In the modern financial landscape, maintaining a clear view of one’s cash flow is essential for long-term stability. However, even the most meticulous budgeters can occasionally find themselves in a precarious position where an unexpected bill or a timing mismatch between a deposit and a withdrawal leads to a negative balance. This scenario triggers what is known as an overdraft. While a bank paying a transaction on your behalf when you lack the funds might seem like a convenience, it comes at a significant cost. Overdraft charges represent one of the most substantial revenue streams for traditional financial institutions and, conversely, one of the most common pitfalls for consumers. Understanding the mechanics of these charges is the first step toward achieving total control over your personal finances.

The Mechanics of Overdrafts and How They Occur

At its core, an overdraft occurs when a transaction—whether it be a check, an ATM withdrawal, a debit card purchase, or an electronic transfer—exceeds the available balance in a checking account. Rather than simply declining the transaction, the bank chooses to cover the deficit, effectively issuing a short-term, high-interest loan to the account holder.

What is an Overdraft?

An overdraft is a financial state where your account balance drops below zero. In the eyes of a bank, providing an overdraft service is a discretionary act. Unless you have a specific agreement in place, the bank is not legally obligated to cover your overage. When they do, they are providing a service that prevents a payment from “bouncing,” which could otherwise lead to late fees from vendors or damage to your reputation with creditors. However, this “service” is rarely free.

How Transactions are Processed

One of the most complex aspects of overdrafts is the order in which transactions are processed. Banks do not always process transactions in the chronological order they occur. Many institutions use automated systems that batch transactions at the end of the business day. Historically, some banks processed the largest transactions first. While this ensures that major payments like rent or mortgages are cleared, it also quickly depletes the account balance, potentially triggering multiple overdraft fees for smaller subsequent purchases like a coffee or a grocery item. Understanding your bank’s specific processing order is vital to predicting when a fee might be assessed.

Available Balance vs. Current Balance

A common source of confusion is the difference between your “current balance” and your “available balance.” The current balance represents the total amount of money in the account, including deposits that have not yet cleared. The available balance is the amount you can actually spend right now. Overdraft charges are typically triggered based on the available balance. If you deposit a check on Friday, the bank may place a “hold” on those funds, meaning they aren’t part of your available balance until Monday. Spending against those pending funds can lead to an overdraft.

The Different Types of Overdraft and Related Fees

Not all “insufficient fund” situations are treated equally. Depending on the bank’s policies and the nature of the transaction, you may be hit with different types of penalties. These fees can stack quickly, turning a $5 deficit into a $100 liability in a single afternoon.

Standard Overdraft Fees

The most common charge is the standard overdraft fee. This is a flat fee applied to each transaction the bank chooses to cover while your account is in the negative. In the United States, this fee typically ranges between $30 and $35 per item. Because these are per-item charges, a series of small transactions can lead to a cascade of fees that far exceed the original amount overdrawn.

Non-Sufficient Funds (NSF) Fees

A Non-Sufficient Funds (NSF) fee occurs when the bank decides not to cover the transaction. In this case, the transaction is returned or declined, and the bank charges you a fee for the “returned item.” The danger here is twofold: not only do you owe the bank an NSF fee, but the merchant you attempted to pay may also charge you a “returned check fee” or a late payment penalty. This makes NSF scenarios particularly damaging to your monthly budget.

Continuous Overdraft and Extended Fees

If your account remains in a negative balance for several consecutive days, many banks apply a “continuous overdraft fee” or an “extended overdrawn balance fee.” This is essentially a daily penalty for failing to bring the account back to a positive standing. These charges emphasize the importance of resolving a negative balance immediately, as the cost of the overdraft increases the longer the debt remains unpaid.

The Impact of Overdrafts on Your Financial Health

While an occasional $35 fee might seem like a minor annoyance, the cumulative effect of overdraft charges can have a devastating impact on your broader financial strategy and your ability to access credit.

The True Cost of “Small” Loans

When viewed as a percentage, overdraft fees are among the most expensive forms of credit available. If you overdraw your account by $20 and are charged a $35 fee, and you pay that back when your paycheck arrives five days later, the effective annual percentage rate (APR) is in the thousands. Relying on overdrafts as a safety net is significantly more expensive than using a credit card or a personal line of credit.

Credit Score and ChexSystems

While standard overdrafts on a checking account usually do not report to the three major credit bureaus (Equifax, Experian, and TransUnion), they can still ruin your “banking credit.” Most financial institutions use a service called ChexSystems to track how consumers manage their bank accounts. If an account is closed with a negative balance due to unpaid overdraft fees, it is reported to ChexSystems. This can make it nearly impossible to open a new bank account at any major institution for up to five years, forcing individuals into the “unbanked” or “underbanked” population who rely on expensive check-cashing services.

Impact on Financial Psychology

Frequent overdrafting often points to a breakdown in financial planning or an underlying issue with “liquidity management.” It creates a cycle of debt where a significant portion of a person’s next paycheck is immediately diverted to paying off previous fees and negative balances, leaving them with even less money for the current month’s expenses. Breaking this cycle is essential for building an emergency fund and investing for the future.

Strategies to Avoid Overdraft Charges

The most effective way to manage overdraft charges is to prevent them entirely. Through a combination of modern banking tools and disciplined habits, consumers can insulate themselves from these predatory fees.

Leveraging Real-Time Alerts

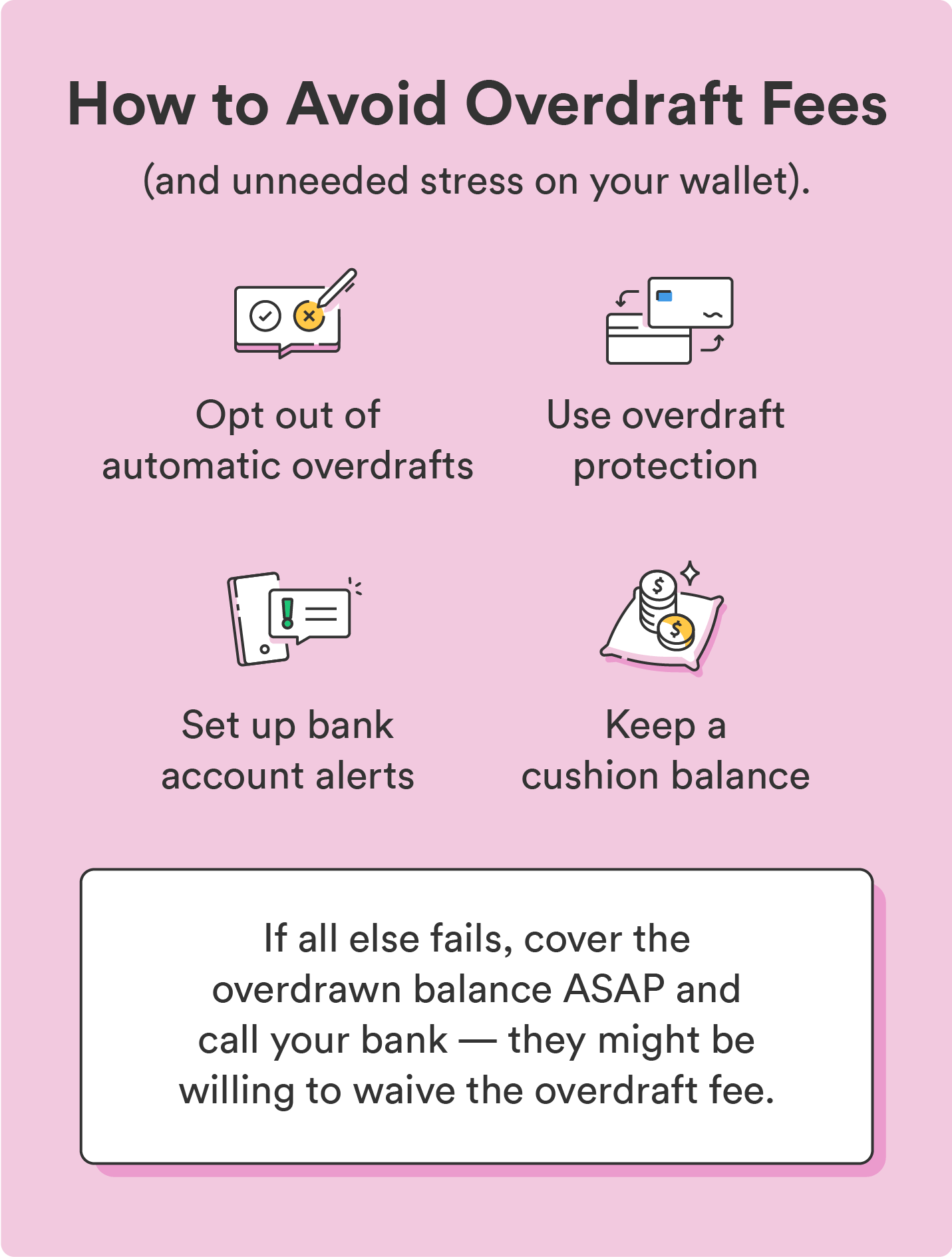

Most modern banking apps allow users to set up customizable notifications. The most important of these is the “Low Balance Alert.” By setting a threshold—for example, $100—you can receive a text or push notification the moment your balance dips below that amount. This provides a crucial window of time to transfer funds from a savings account or to curtail spending until the next deposit.

Overdraft Protection Transfers

Many banks offer an “Overdraft Protection” service that links your checking account to a savings account, money market account, or credit card. If you overdraw your checking account, the bank automatically transfers funds from the linked account to cover the shortfall. While some banks charge a small fee for this transfer (often around $10-$12), it is significantly cheaper than a $35 overdraft fee. More importantly, it ensures your transactions are cleared without moving your balance into the negative.

The Power of “Opting Out”

Under federal regulations (such as Regulation E in the U.S.), banks are prohibited from charging overdraft fees on one-time debit card and ATM transactions unless the customer has specifically “opted in” to the service. If you opt out, your card will simply be declined at the point of sale if you have insufficient funds. While being declined at a cash register may be embarrassing, it is a free event that protects you from incurring high-cost debt.

Navigating Bank Regulations and Consumer Rights

The landscape of banking fees is constantly evolving, driven by both consumer advocacy and government regulation. Knowing your rights can help you recover funds if you believe a fee was assessed unfairly.

Recent Regulatory Shifts

In recent years, there has been a significant push by regulators to limit the “junk fees” associated with banking. Some of the most consumer-friendly changes include “de minimis” thresholds, where banks agree not to charge a fee if the account is overdrawn by less than a small amount (e.g., $5 or $10). Additionally, some institutions have completely eliminated overdraft fees in an attempt to compete with “neobanks” and fintech startups that prioritize fee-free structures.

Negotiating Fee Waivers

If you are a long-standing customer with a generally good history, you have more leverage than you might think. If you are hit with an overdraft fee due to an honest mistake or a technical delay, call your bank’s customer service department. Politely explain the situation and ask for a “one-time courtesy waiver.” Banks often have the authority to reverse these fees to maintain customer loyalty, especially if it is your first offense in a 12-month period.

Choosing the Right Financial Institution

Ultimately, the best defense against overdraft charges is choosing a bank whose fee structure aligns with your financial goals. Many online-only banks and credit unions offer accounts with no overdraft fees or “no-fee” overdraft buffers. When shopping for a new bank account, the fee schedule should be just as important as the interest rate. By aligning yourself with an institution that prioritizes transparency over penalty-based revenue, you can ensure that more of your hard-earned money stays in your pocket, fueling your personal wealth rather than the bank’s bottom line.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.