The question “what are Islam people called” is one that touches on the fundamental identity of over 1.8 billion people worldwide. To answer it simply: followers of Islam are called Muslims. However, in the realms of global finance, investment, and market strategy, this label represents one of the fastest-growing and most influential economic demographics on the planet. For investors, entrepreneurs, and financial analysts, understanding who Muslims are—and the specific ethical frameworks that govern their financial lives—is no longer optional; it is a prerequisite for tapping into a multi-trillion-dollar global market.

The Economic Power of the Muslim Identity

The term “Muslim” refers to an individual who submits to the will of God (Allah) as outlined in the Quran. Beyond the religious definition, this identity carries significant weight in the world of Money. As the global Muslim population continues to grow—projected to reach nearly 3 billion by 2050—their collective purchasing power and investment preferences are reshaping international trade.

The Demographic Dividend

The Muslim demographic is remarkably young compared to Western counterparts. With a median age significantly lower than the global average, this “next-gen” Muslim consumer base is tech-savvy, brand-conscious, and increasingly affluent. For those looking at long-term wealth creation and market entry, the youth of this demographic suggests a decades-long runway for growth in consumer goods, digital services, and real estate.

Identifying the “Halal” Consumer

In a financial context, the Muslim identity is inextricably linked to the concept of Halal (permissible). While many associate Halal strictly with dietary laws, in the niche of personal finance and business, it refers to a comprehensive ethical framework. To engage with the “Muslim market” effectively, businesses must move beyond the label and understand the values of transparency, equity, and social responsibility that drive Muslim spending habits.

Islamic Finance: A System Built on Ethics and Equity

For those called Muslims, money is not merely a tool for accumulation but a means of achieving social and spiritual balance. This has given rise to Islamic Finance, a system of banking and investment that operates without the use of interest (Riba), which is strictly prohibited under Sharia (Islamic law).

The Prohibition of Riba and the Rise of Profit-Sharing

The most distinct feature of the financial world inhabited by Muslims is the avoidance of usury. In conventional banking, money is treated as a commodity that earns interest. In Islamic finance, money is a medium of exchange. To generate a return, the capital must be deployed into productive economic activity. This leads to “Profit and Loss Sharing” (PLS) models such as Mudarabah (partnership where one provides capital and the other expertise) and Musharakah (joint venture). This creates a more resilient financial system where the bank and the client share the risks and rewards of an enterprise.

Sukuk: The Islamic Alternative to Bonds

Institutional investors have long searched for stable, long-term assets. In the Islamic world, conventional bonds are not an option because they represent a debt with interest. Instead, the market utilizes Sukuk. Unlike a bond, which is a debt obligation, a Sukuk represents partial ownership in an underlying tangible asset, such as infrastructure or real estate. This “asset-backed” nature of Sukuk has gained traction even among non-Muslim investors looking for more secure, transparent investment vehicles during times of global market volatility.

The Multi-Trillion Dollar Halal Economy

When we discuss the financial landscape of Muslims, we must look at the “Halal Economy.” This sector encompasses everything from food and pharmaceuticals to modest fashion and “halal travel.” Current estimates value the global Islamic economy at over $2 trillion, with steady annual growth that outpaces many conventional sectors.

The Modest Fashion Revolution

One of the most visible financial shifts driven by the Muslim identity is the rise of modest fashion. Global brands like Nike, Dolce & Gabbana, and Uniqlo have launched specific lines to cater to Muslim women who seek stylish yet culturally appropriate clothing. This is not just a cultural trend; it is a massive revenue stream. The modest fashion industry is projected to reach several hundred billion dollars in the coming years, presenting a lucrative opportunity for retail investors and venture capitalists.

Halal Food and Pharmaceutical Integrity

The requirement for Halal products extends deep into the supply chain. For a product to be certified Halal, it must be free from prohibited substances (like pork or alcohol) and produced under ethical conditions. This has created a massive global industry for certification, logistics, and specialized manufacturing. Investors are increasingly looking at “Halal-Tech” companies that use blockchain to track the provenance of food, ensuring that it meets the strict standards required by Muslim consumers from farm to table.

Wealth Management and Ethical Investing for Muslims

For the modern Muslim investor, the goal is often “Halal Wealth Management.” This involves ensuring that one’s portfolio does not include companies involved in gambling, alcohol, tobacco, or conventional high-interest banking.

Sharia-Compliant Stock Screening

The process of identifying which stocks are “permissible” for Muslims has become a specialized field within finance. Quantitative filters are used to ensure that a company’s debt-to-equity ratio is low and that its primary income does not come from Haraam (forbidden) activities. Fintech apps like Zoya or Sarwa have democratized this process, allowing individual Muslim investors to trade stocks with the confidence that their money is aligned with their values. This surge in retail investing among Muslims is a key driver of liquidity in many emerging markets.

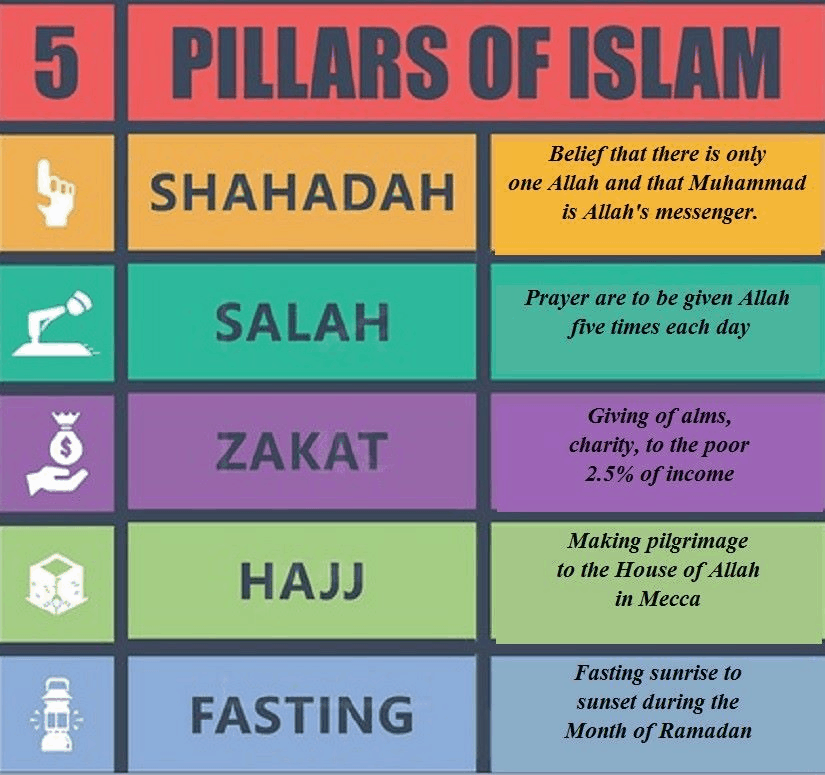

The Role of Zakat and Philanthropic Finance

A unique aspect of Muslim personal finance is Zakat, the mandatory giving of a portion of one’s accumulated wealth (usually 2.5%) to the poor. While often viewed as a religious duty, Zakat is a powerful economic tool for wealth redistribution and poverty alleviation. In recent years, “Zakat-Tech” platforms have emerged, allowing for more efficient collection and distribution of these funds. This social finance aspect makes the Muslim demographic a pioneer in what the modern West calls “Impact Investing” or “ESG” (Environmental, Social, and Governance) criteria.

Digital Transformation in the Muslim Financial Space

As the global economy moves toward digitalization, the Muslim market is at the forefront of the Fintech revolution. The intersection of Islamic values and modern technology is creating new ways for Muslims to manage their money.

Islamic Fintech and Neobanking

Traditional banks often struggle to meet the specific needs of Muslim clients. This gap has been filled by a new wave of Islamic Neobanks—digital-first institutions that offer interest-free accounts, Sharia-compliant home financing, and ethical investment tools. These platforms leverage AI and big data to provide personalized financial advice that respects religious boundaries, making them highly attractive to the younger, tech-savvy Muslim demographic.

Cryptocurrency and Sharia Compliance

One of the most debated topics in the world of money is the status of cryptocurrency. Within the Muslim community, scholars and financial experts are working to determine how digital assets fit into Islamic law. Some view crypto as a form of “digital gold” that avoids the pitfalls of fiat currency and interest-based systems. As more Sharia-compliant crypto exchanges and “Halal coins” emerge, we can expect a significant influx of Muslim capital into the decentralized finance (DeFi) space.

Conclusion: Why the Muslim Demographic Matters for Future Wealth

Answering “what are Islam people called” is the first step in recognizing a global community that is as diverse as it is economically significant. Muslims are not just a religious group; they are a driving force in the modern economy, characterized by a commitment to ethical finance, a preference for asset-backed investments, and a rapidly growing consumer market.

For the financial professional or the savvy investor, the “Muslim niche” represents stability in an era of debt-heavy economies. By focusing on tangible assets, profit-sharing, and social responsibility, the financial systems built by and for Muslims offer a blueprint for a more equitable global economy. Whether it is through the $2 trillion Halal market or the burgeoning Islamic Fintech sector, the economic influence of Muslims is set to be one of the defining stories of 21st-century finance. Understanding this demographic is no longer just about terminology—it is about recognizing the future of global money.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.