In the world of finance, the difference between a comfortable retirement and generational wealth often boils down to a single mathematical distinction: the difference between arithmetic and geometric sequences. While these terms are frequently relegated to the back of high school algebra textbooks, they are the silent engines behind every bank account, investment portfolio, and debt cycle in the global economy.

Understanding how these sequences function is not merely an academic exercise; it is a fundamental requirement for anyone looking to optimize their personal finance strategy. Whether you are calculating the interest on a car loan or projecting the growth of a 401(k), you are interacting with these two distinct patterns of progression. By mastering the nuances of how money moves—either by addition or by multiplication—you can shift your financial trajectory from stagnant to stratospheric.

Understanding the Core Logic: Difference vs. Ratio

To master your money, you must first understand the DNA of growth. At their most basic level, arithmetic and geometric sequences represent the two primary ways that a numerical value evolves over time.

The Arithmetic Framework: Steady and Predictable

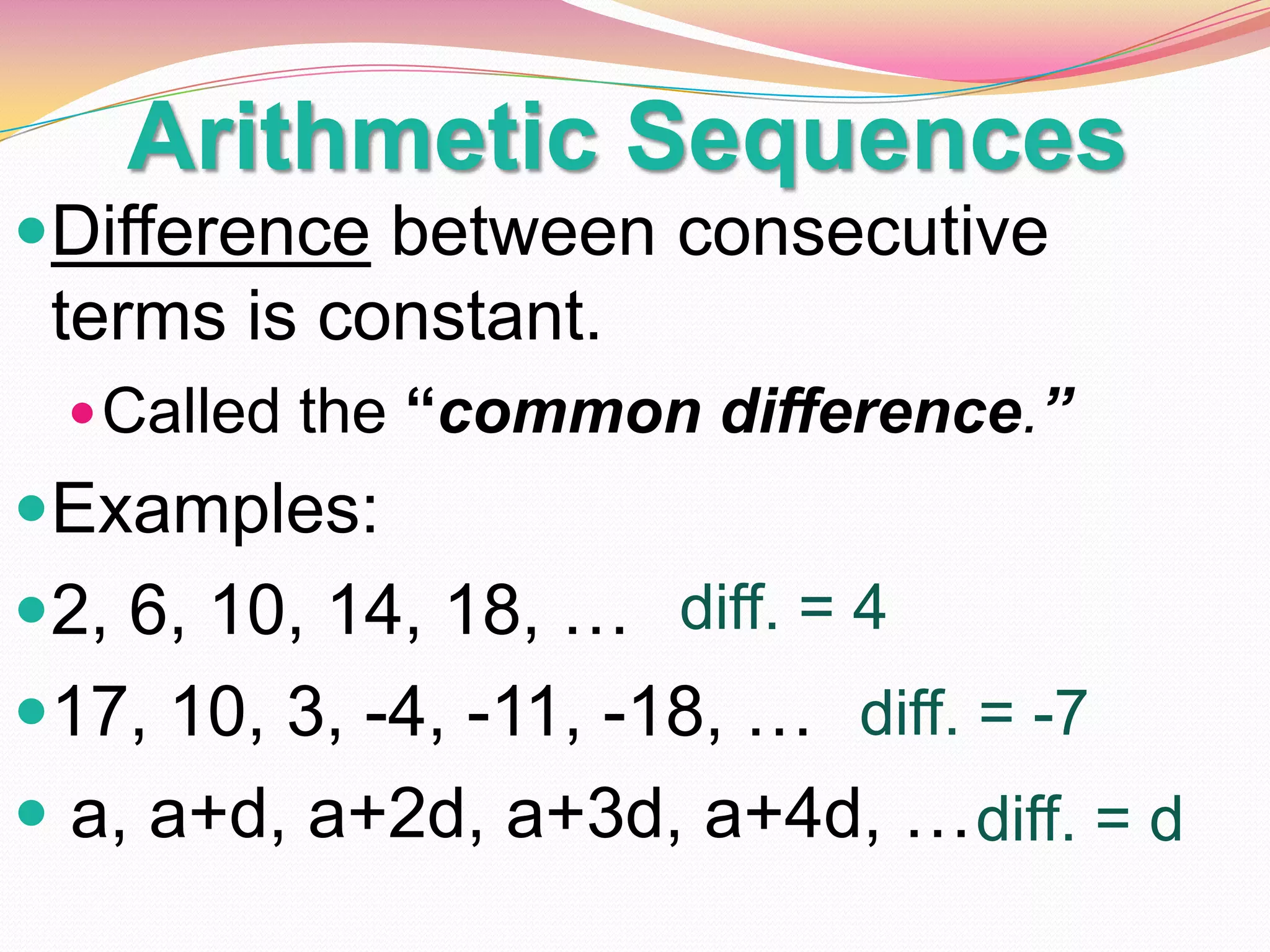

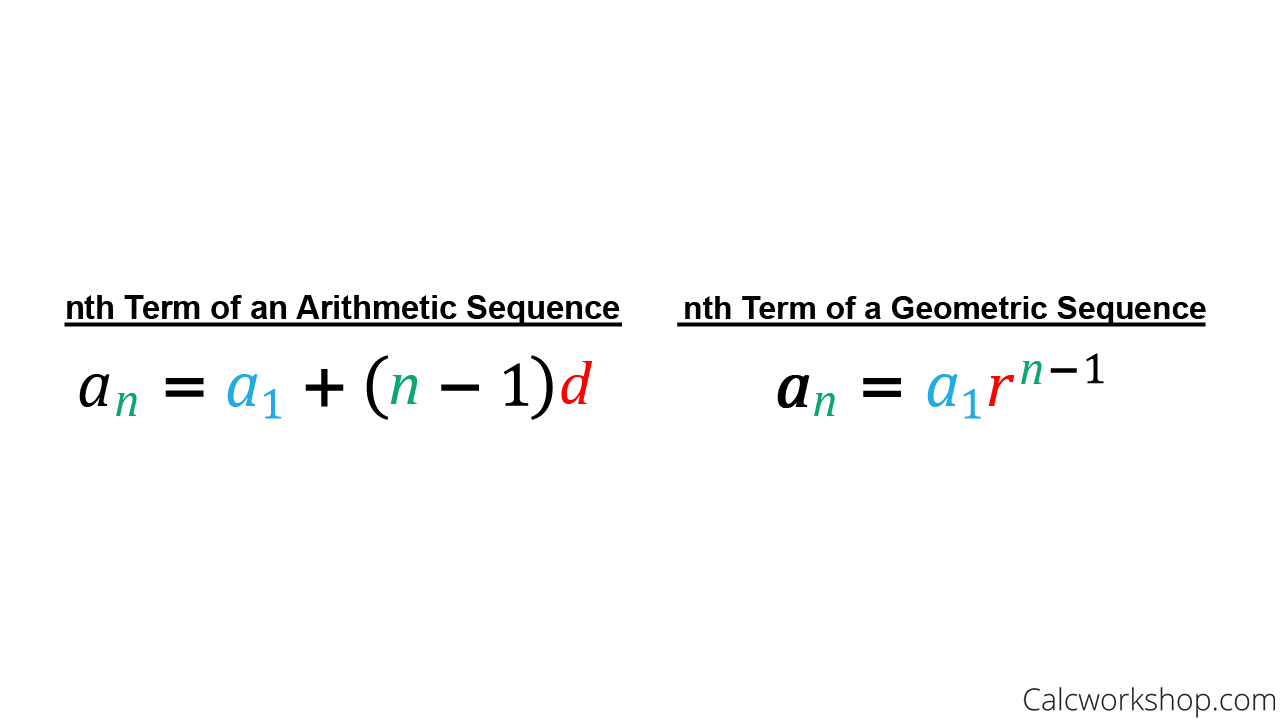

An arithmetic sequence is a sequence of numbers in which the difference between consecutive terms is constant. In mathematical terms, this is known as the “common difference” ($d$). If you start with $100 and add $10 every month, your balance follows an arithmetic progression: $110, $120, $130, and so on.

In the niche of personal finance, arithmetic growth is linear. It is predictable, steady, and easy to visualize. It represents the “hustle”—the direct correlation between time worked and money earned. If you earn a fixed hourly wage, your daily income is an arithmetic sequence. While this provides a necessary foundation for stability, linear growth is inherently limited by the finite nature of time.

The Geometric Framework: The Multiplier Effect

Conversely, a geometric sequence is a sequence of numbers where each term after the first is found by multiplying the previous one by a fixed, non-zero number called the “common ratio” ($r$). If you start with $100 and it grows by 10% each year, you are not adding a flat $10. Instead, you are multiplying the previous year’s total by 1.10. Your sequence becomes $110, $121, $133.10, and so forth.

The power of the geometric sequence lies in its acceleration. Unlike the flat line of an arithmetic sequence, a geometric sequence creates a curve that steepens over time. In finance, this is the mechanism behind compounding. It is the shift from working for money to having your money work for you.

Arithmetic Sequences in Personal Finance: The Foundation of Stability

While geometric growth gets the most headlines in the investing world, arithmetic sequences are the bedrock of financial discipline and short-term planning. Most people’s financial lives begin with arithmetic logic.

Fixed Savings Plans and Budgeting

The most common application of an arithmetic sequence in money management is the recurring deposit. When a financial advisor suggests “paying yourself first” by automating a $500 monthly transfer into a high-yield savings account, they are setting up an arithmetic progression.

This type of growth is essential for emergency funds and short-term goals, such as saving for a wedding or a down payment on a home. Because the growth is linear, it is highly resistant to market volatility. You know exactly how much you will have in twelve months because the “common difference” is your monthly contribution. For liquidity and short-term security, the predictability of arithmetic sequences is an asset, not a limitation.

Simple Interest and Debt Principal Reduction

Arithmetic sequences also play a critical role in debt management, specifically regarding simple interest and principal-only payments. Some short-term loans or personal IOUs operate on simple interest, where the interest is calculated only on the original principal.

More importantly, when you make “extra payments” toward the principal of a mortgage or student loan, you are effectively trying to force a geometric debt (compound interest) into an arithmetic decline. By applying a fixed “common difference” to your debt balance every month above the required interest, you systematically reduce the timeline of the loan. Understanding this linear reduction helps borrowers visualize the “light at the end of the tunnel” in a way that complex compounding formulas often obscure.

The Power of Geometric Sequences: Exponential Wealth Creation

If arithmetic sequences provide the foundation, geometric sequences provide the skyscraper. To achieve true financial independence, one must transition from relying on additive growth to harnessing multiplicative growth.

Compound Interest: The Eighth Wonder of the World

Albert Einstein famously referred to compound interest as the eighth wonder of the world, stating, “He who understands it, earns it; he who doesn’t, pays it.” Compound interest is the real-world application of a geometric sequence.

In a geometric sequence, the “common ratio” ($r$) is $(1 + text{interest rate})$. Because each new term is calculated based on the previous term (which already includes previous growth), the sequence experiences “growth on growth.” In the early stages, the difference between arithmetic and geometric growth seems negligible. However, over decades, the gap becomes a chasm. A $10,000 investment growing arithmetically at $1,000 a year results in $40,000 after 30 years. That same $10,000 growing geometrically at 10% annually results in approximately $174,494. The geometric sequence doesn’t just perform better; it operates in an entirely different dimension of wealth.

Reinvestment and Asset Appreciation

Geometric sequences are also found in dividend reinvestment plans (DRIPs) and business scaling. When a company reinvests its profits to buy more inventory or build more locations, it is attempting to achieve a geometric growth rate.

For the individual investor, the common ratio is often determined by the rate of return of the asset class. Historically, the stock market has provided a geometric return of roughly 7-10% annually. By reinvesting dividends, you ensure that your “common ratio” remains high, allowing the geometric sequence to work its magic. This is why time is the most valuable asset in investing; the most dramatic gains in a geometric sequence occur in the later stages of the progression.

Strategic Decision-Making: Choosing the Right Growth Model

Successful financial planning requires knowing when to think arithmetically and when to think geometrically. Misapplying these concepts can lead to the “Linear Trap,” where an individual works harder and harder without ever gaining momentum.

Avoiding the Linear Trap

The “Linear Trap” occurs when a person’s income is purely arithmetic (trading hours for dollars) while their expenses or debts are geometric (credit card interest or inflation). If your salary increases by a flat $2,000 a year (arithmetic) but the cost of living increases by 3% (geometric), you are effectively losing purchasing power over time.

To escape this trap, one must convert arithmetic income into geometric assets. This is the essence of investing. By taking the “common difference” from your paycheck and placing it into a vehicle with a “common ratio” (like an index fund or real estate), you bridge the gap between working for a living and owning your time.

Mitigating Geometric Risks: Inflation and Market Volatility

It is important to recognize that geometric sequences can work against you just as easily as they can work for you. Inflation is a geometric sequence that erodes the value of the dollar. A 3% inflation rate is a common ratio of 0.97 applied to your purchasing power every year. Over 20 years, this geometric decay can cut the value of “stagnant” cash in half.

Furthermore, while geometric sequences in the stock market are powerful, they are not always smooth. Market volatility can temporarily turn a positive common ratio into a negative one. This is why diversification and asset allocation are vital. A savvy investor uses arithmetic stability (bonds, cash reserves) to protect their geometric engines (stocks, private equity) during market downturns.

Conclusion: The Path to Financial Literacy

The distinction between arithmetic and geometric sequences is the boundary between the middle class and the wealthy. Arithmetic sequences—characterized by addition and linear progression—are excellent for budgeting, saving for short-term goals, and maintaining a disciplined lifestyle. They represent the “slow and steady” approach that keeps the lights on.

However, to build significant wealth and outpace the geometric erosion of inflation, one must embrace the geometric sequence. By focusing on the common ratio—the return on investment, the compounding of interest, and the scaling of business assets—you unlock the potential for exponential growth.

Financial literacy is, at its core, the ability to read these patterns in your own bank statements. When you stop looking at your money as a pile to be added to and start seeing it as a seed to be multiplied, you have mastered the most important mathematical lesson in the world of finance. Whether you are at the beginning of your career or nearing retirement, the choice remains the same: will you live your life by the plus sign, or by the multiplication sign?

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.