Navigating the world of dental health often feels like a balancing act between physical well-being and financial stability. When a tooth is lost due to decay, injury, or age, the immediate concern is often aesthetic, but the secondary concern is almost always the price tag. A dental bridge is one of the most common and effective solutions for replacing missing teeth, yet the “sticker price” can vary wildly depending on a multitude of factors.

In the realm of personal finance, a dental bridge should be viewed not just as a medical necessity, but as a significant capital expenditure. Understanding the variables that drive these costs—from material selection to insurance nuances—is essential for any consumer looking to maintain their health without compromising their long-term financial goals. This guide provides an in-depth analysis of the costs associated with dental bridges, offering a strategic framework for budgeting, financing, and maximizing the value of your investment.

Understanding the Financial Breakdown of Dental Bridges

The cost of a dental bridge is rarely a flat fee. Instead, it is a composite of several variables including the type of bridge, the materials used, and the complexity of the installation. On average, a consumer can expect to pay anywhere from $1,500 to $5,000 per bridge, though these figures can climb significantly higher if dental implants are involved.

Type of Bridge and Its Impact on Price

The structural design of the bridge is the primary driver of the initial quote.

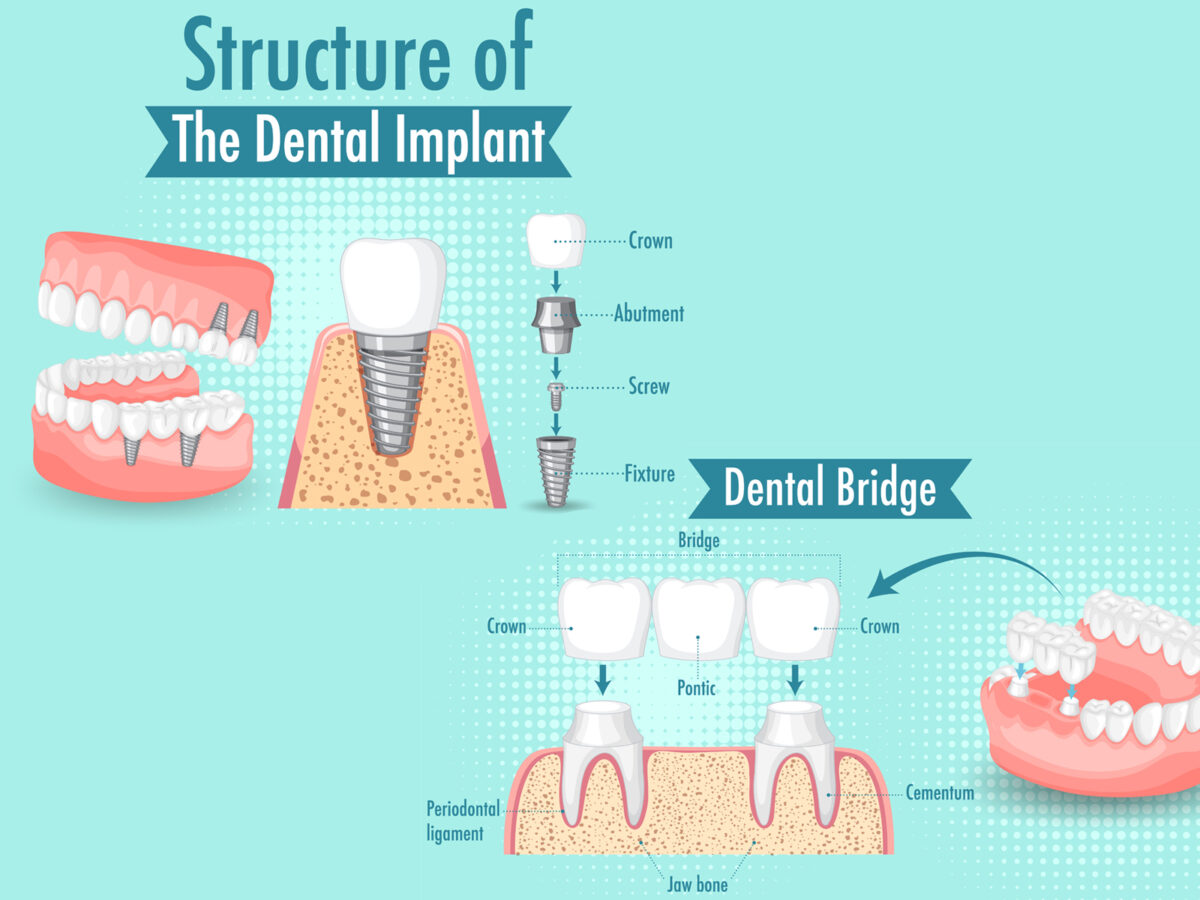

- Traditional Bridges: These are the most common and involve creating crowns for the teeth on either side of the gap. Because they require the alteration of healthy “abutment” teeth, the cost reflects both the bridge fabrication and the labor for reshaping surrounding teeth.

- Cantilever Bridges: Used when there is only one adjacent tooth to support the bridge, these are similar in price to traditional bridges but are less common due to the potential for structural stress on the single supporting tooth.

- Maryland Bridges: Often the most “budget-friendly” option, these use a metal or porcelain framework bonded to the backs of adjacent teeth. Because they don’t require extensive crowning of neighbor teeth, the laboratory and clinical time are reduced, often bringing the cost down to the $1,500–$2,500 range.

- Implant-Supported Bridges: From a financial perspective, this is a high-tier investment. Rather than being supported by teeth, the bridge is supported by dental implants. While the bridge itself might cost $3,000, the surgical placement of implants can push the total project cost upward of $10,000 to $15,000.

Material Costs: Porcelain vs. Metal vs. Zirconia

The “ingredients” of your bridge dictate both its longevity and its price. Base metal alloys are the least expensive but are often avoided for front-of-mouth aesthetics. Porcelain-fused-to-metal (PFM) offers a middle ground, providing strength and a tooth-like appearance. However, the current “gold standard” in both durability and cost is Zirconia or all-ceramic bridges. These materials are bio-compatible and highly resistant to chipping, but they require advanced milling technology, which is reflected in a higher laboratory fee passed on to the patient.

Direct and Indirect Costs Associated with the Procedure

When budgeting for a dental bridge, it is a mistake to look only at the cost of the prosthetic itself. Restorative dentistry involves a series of clinical steps, each of which carries its own line item on a financial statement.

Preparatory Procedures and Diagnostic Fees

Before a bridge can be placed, the “foundation” must be assessed. This involves diagnostic imaging (X-rays or 3D CT scans) which can range from $100 to $500. Furthermore, if the abutment teeth have underlying decay, they may require root canals or core buildups before they are strong enough to support a bridge. A single root canal can add $800 to $1,500 to the total bill. If you are opting for an implant-supported bridge, you may also face costs for bone grafting if your jawbone density is insufficient, adding another $500 to $2,000 to the total expenditure.

Labor and Geographic Variables in Pricing

The “where” and “who” of the procedure are significant financial factors. Dental fees are not standardized; they are influenced by the local cost of living and the overhead of the practice. A prosthodontist—a specialist in tooth replacement—will typically charge 20% to 40% more than a general dentist. While this represents a higher upfront cost, the specialized expertise may offer a better “Return on Investment” (ROI) through a lower likelihood of procedural failure or the need for premature replacement. Geographically, undergoing the procedure in a major metropolitan area like New York City or San Francisco will inevitably cost more than in a rural setting due to higher commercial rents and labor costs for dental assistants and lab technicians.

Insurance, Financing, and Budgeting Strategies

Given the high cost of dental bridges, few patients pay the entire sum out-of-pocket without a strategic financial plan. Leveraging financial tools can transform a daunting lump-sum payment into a manageable monthly expense.

Maximizing Dental Insurance Benefits

Most dental insurance plans categorize bridges as “Major Services.” Typically, this means the insurer will cover approximately 50% of the cost, provided you have met your deductible. However, there is a catch: the “Annual Maximum.” Most dental plans cap their yearly payout between $1,000 and $2,000. If a bridge costs $4,000, and your insurance covers 50%, you might expect to pay $2,000. But if your annual maximum is $1,000, you will actually be responsible for $3,000.

A savvy financial move is “straddling” the treatment across two calendar years. If your dentist prepares the teeth in December and sets the final bridge in January, you may be able to apply two years’ worth of insurance maximums to a single procedure, effectively doubling your coverage.

Flexible Spending Accounts (FSA) and Health Savings Accounts (HSA)

For those with high-deductible health plans, an HSA is a powerful tool for dental work. Contributions to an HSA are tax-deductible, the growth is tax-free, and withdrawals for qualified medical expenses (like dental bridges) are tax-free. Using “pre-tax” dollars can effectively provide a 20% to 30% discount on the procedure, depending on your tax bracket. FSAs offer similar tax advantages but are “use-it-or-lose-it,” making it critical to time your dental bridge surgery with your plan year.

Payment Plans and Third-Party Financing

Many dental offices partner with third-party lenders like CareCredit or LendingClub. These companies offer promotional periods—often 6 to 24 months—with 0% interest. From a cash-flow perspective, this is an excellent way to preserve your liquidity. However, consumers must be cautious: if the balance is not paid in full by the end of the promotional period, deferred interest (often at rates exceeding 25%) may be applied retroactively to the entire original balance.

Long-Term Value vs. Immediate Expense

In personal finance, it is essential to distinguish between “price” (what you pay now) and “cost” (what you pay over the lifetime of the asset). A dental bridge is a functional asset that requires maintenance and eventual replacement.

The Cost of Neglect: Avoiding Secondary Financial Consequences

Choosing not to get a bridge or implant after losing a tooth might seem like a way to save money, but it often leads to “financial leakage” later. When a gap is left empty, adjacent teeth begin to shift. This can lead to malocclusion (misaligned bite), which causes tooth wear, jaw pain (TMJ), and an increased risk of periodontal disease. The cost of correcting a collapsed bite or treating advanced gum disease often far exceeds the initial investment of a dental bridge. In this context, a bridge is a defensive financial play to protect the rest of your dental “portfolio.”

Durability and Replacement Cycles

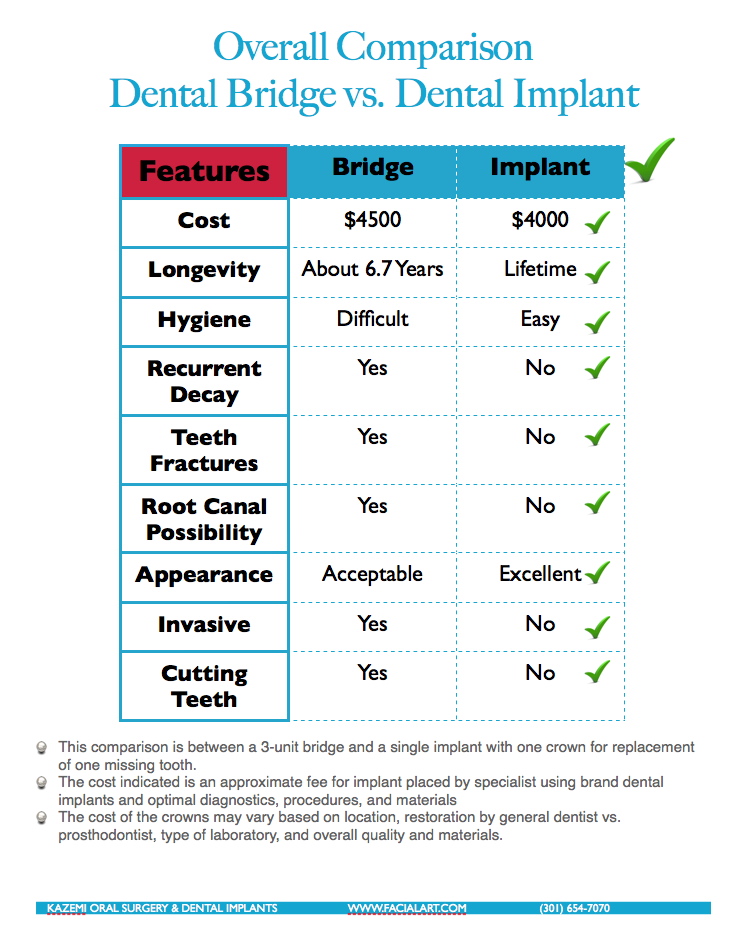

The average lifespan of a dental bridge is 5 to 15 years. When calculating the long-term cost, you must factor in the likelihood of replacement. A $3,000 bridge that lasts 15 years costs $200 per year of utility. A cheaper $2,000 bridge that fails after 5 years costs $400 per year. Furthermore, if a bridge fails, it often compromises the abutment teeth, potentially leading to the need for more expensive implants or larger bridges.

For many, the higher upfront cost of an implant-supported bridge is the more logical financial choice. While a traditional bridge may need to be replaced two or three times over a lifetime, an implant is designed to be a permanent solution. When conducting a 20-year cost analysis, the implant often emerges as the more cost-effective option despite its intimidating initial price.

Conclusion

The cost of a dental bridge is a significant financial consideration that requires more than a simple glance at a price list. By understanding the structural types, material differences, and the various ways to leverage insurance and tax-advantaged accounts, patients can make informed decisions that align with their personal balance sheets.

Ultimately, dental health is an investment in your “human capital.” The ability to eat properly, speak clearly, and present yourself confidently in professional settings has an intangible but real impact on your earning potential and quality of life. By viewing a dental bridge through the lens of personal finance—evaluating ROI, managing cash flow, and mitigating long-term risk—you can navigate this restorative journey with both a healthy smile and a healthy bank account.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.