In the modern landscape of personal finance, the debit card serves as the primary bridge between your hard-earned savings and the global marketplace. While we use these plastic or metal rectangles daily, few of us stop to consider the complex logic embedded within the long string of digits embossed on the front or printed on the back. This number is far more than a random sequence; it is a sophisticated financial identifier that facilitates trillions of dollars in transactions annually.

Understanding what your debit card number is, how it is structured, and the role it plays in your financial security is essential for anyone looking to navigate the digital economy safely. This guide provides an in-depth exploration of the debit card number from a personal finance perspective, detailing its anatomy, its function in the payment ecosystem, and how to protect it as part of a robust financial strategy.

The Anatomy of a Debit Card Number: Decoding the Digits

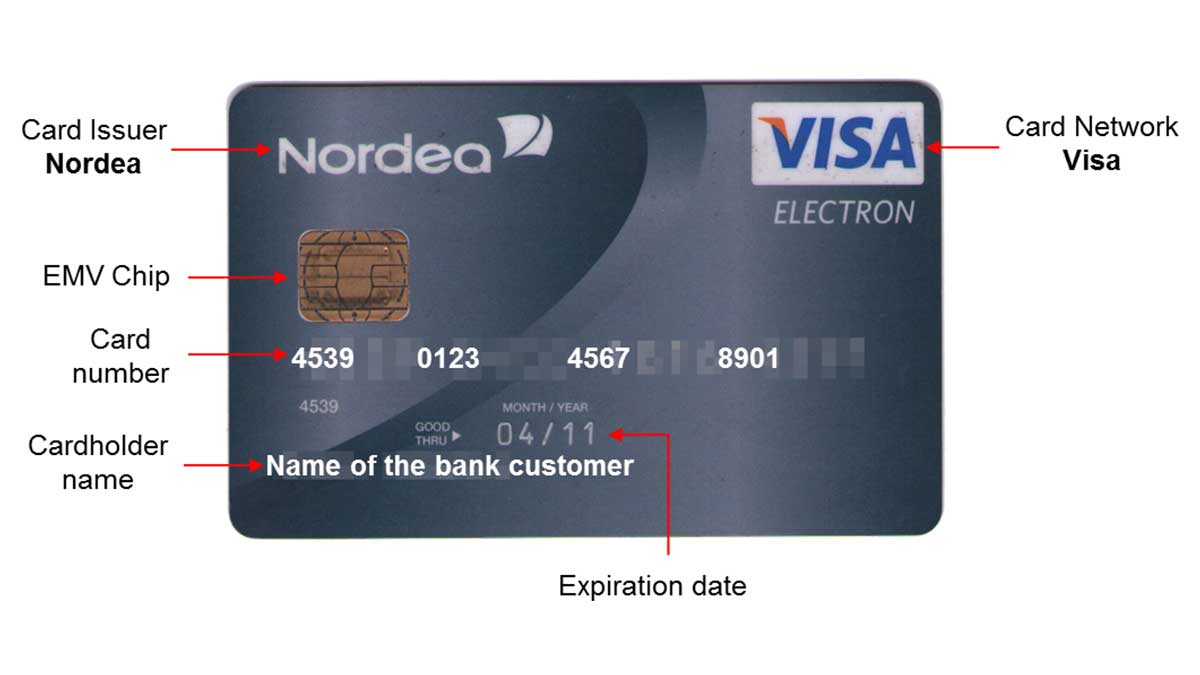

To the untrained eye, a debit card number—usually 16 digits long—looks like a random string of numbers. However, these digits follow a strict international standard (ISO/IEC 7812) that allows financial institutions worldwide to communicate instantly. Each segment of the number tells a specific story about where the card originated and the network it belongs to.

The Major Industry Identifier (MII)

The very first digit of your debit card number is known as the Major Industry Identifier (MII). This digit identifies the category of the entity that issued the card. In the world of personal finance, you will most commonly see:

- 4: Visa (Banking and Financial)

- 5: Mastercard (Banking and Financial)

- 3: American Express or Entertainment/Travel cards

- 6: Discover or Merchandising/Banking

Knowing your MII helps you understand which global network processes your transactions, which can affect where your card is accepted internationally and what kind of consumer protections you might have.

The Issuer Identification Number (IIN)

The first six to eight digits (including the MII) make up the Issuer Identification Number (IIN), formerly known as the Bank Identification Number (BIN). This sequence is a crucial piece of financial data that identifies the specific bank or credit union that issued the card. For example, a specific sequence will tell a merchant’s payment processor that the card belongs to Chase, Barclays, or a local credit union. This allows the electronic payment system to route the transaction request to the correct institution for fund verification.

The Account Identifier and the Check Digit

Following the IIN is a series of digits—usually up to the 15th digit—that represents your individual primary account number (PAN). It is important to note that this is not your actual bank account number. Instead, it is a unique identifier linked to your bank account within the issuer’s internal system. This provides a layer of security, ensuring that even if a merchant has your card number, they do not have your direct bank account details.

The final digit of the sequence is known as the “Check Digit.” This number is calculated using the Luhn Algorithm, a mathematical formula used to validate the card number. When you enter your card number into an online store, the system immediately runs this algorithm. If the result doesn’t match the check digit, the system knows the number was entered incorrectly or is fraudulent, preventing a failed transaction before it even reaches the bank.

Why the Card Number is Central to Personal Finance

In the realm of money management, the debit card number is the primary tool for liquidity. Unlike a credit card, which represents a line of credit, the debit card number is a direct tap into your liquid assets. This fundamental difference makes the management of your card number a high-stakes component of your personal financial health.

Facilitating Seamless Online Transactions

The primary function of the debit card number today is to enable Card-Not-Present (CNP) transactions. In an era where e-commerce is the norm, the card number acts as your digital signature. By providing this number along with your expiration date and CVV, you are authorizing the immediate transfer of funds from your checking account to a merchant. For many, this is the backbone of their budgeting system, allowing for real-time tracking of expenses as they appear on banking apps.

Integration with Digital Wallets and Financial Apps

Modern financial tools have evolved to make the physical card number less visible, yet more integrated. Services like Apple Pay, Google Wallet, and PayPal require you to input your debit card number once to “tokenize” it. From a financial perspective, this is a revolutionary step in security. Instead of sharing your actual 16-digit number with every coffee shop or online retailer, these apps use a “token”—a proxy number that represents your card. This keeps your actual financial key hidden while allowing the convenience of tap-to-pay and one-click checkouts.

Recurring Payments and Subscription Management

For many households, the debit card number is the engine behind automated financial lives. From utility bills to streaming services, recurring payments are tied to this number. While this is convenient for ensuring bills are paid on time, it also requires diligent financial oversight. If your card number changes—due to expiration or theft—all these automated links break, which can lead to service interruptions or late fees. Managing these “linked” accounts is a vital part of modern personal finance maintenance.

Protecting Your Financial Identity: Security Best Practices

Because the debit card number is a direct link to your cash, it is a primary target for bad actors. Protecting this number is synonymous with protecting your bank balance. Understanding the secondary security features associated with your card number is the first step in a defensive financial strategy.

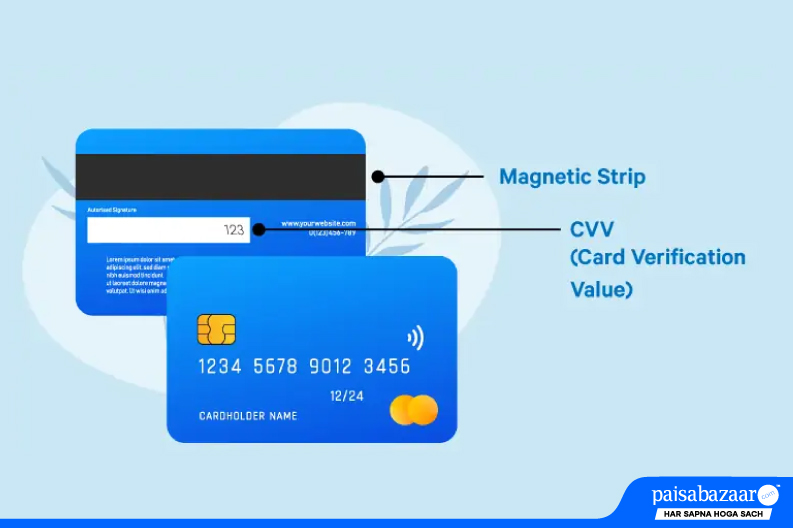

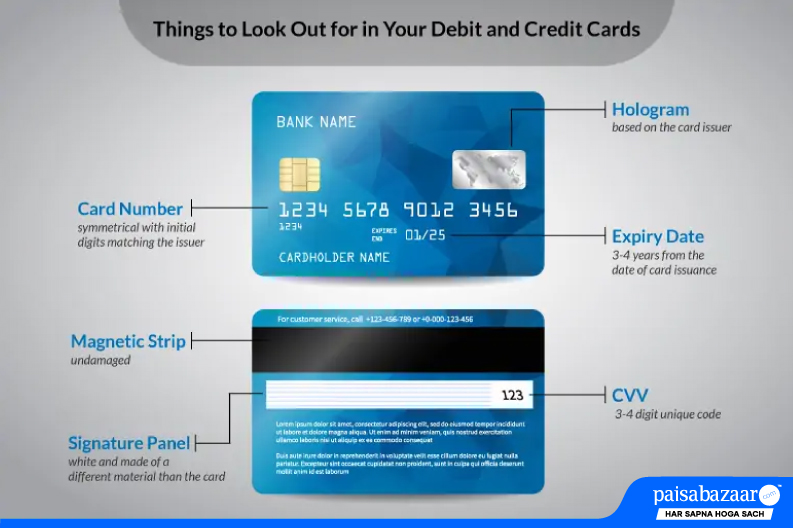

Understanding CVV and Expiration Dates

The card number rarely acts alone. It is almost always accompanied by an Expiration Date and a CVV (Card Verification Value). The CVV is a three- or four-digit security code that is not stored in the magnetic stripe or the chip. Its purpose is to verify that the person making the transaction actually has the physical card in their possession. In terms of financial safety, you should never share your CVV over unencrypted channels, and you should be wary of any “customer service” representative asking for it via phone or email.

Avoiding Phishing and Skimming Scams

Financial literacy includes being aware of how card numbers are stolen. “Skimming” occurs when a small device is placed over a legitimate card reader (like at a gas pump) to capture the card number and its data. “Phishing” involves fraudulent emails or texts designed to trick you into entering your card number on a fake website. To protect your money:

- Use Chip Technology: Whenever possible, dip the chip or use “tap” instead of swiping. The chip creates a unique transaction code that cannot be reused, making the physical card number less vulnerable.

- Monitor Accounts Regularly: Use your banking app to set up “transaction alerts.” If your card number is used without your permission, you will know instantly, allowing you to freeze the card and limit financial damage.

Modern Financial Tools and the Evolution of Card Numbers

As we move toward a more digital-centric financial world, the concept of the static 16-digit card number is changing. Financial institutions are introducing new tools to give consumers more control over their money and how it is accessed.

Virtual Card Numbers for Enhanced Security

One of the most powerful tools in modern personal finance is the “Virtual Card Number.” Some banks and third-party financial services allow you to generate a temporary card number for one-time use or for a specific merchant. For instance, you could generate a virtual number specifically for a new online store you don’t entirely trust. If that store’s database is later hacked, the card number they have is useless because it was set to expire or was locked to that specific merchant. This is an advanced way to wall off your primary bank account from the risks of the internet.

The Transition to Tokenization in Modern Banking

As mentioned earlier, tokenization is the process of replacing the sensitive card number with a non-sensitive equivalent. This is becoming the standard for the “Internet of Things” (IoT). Whether it’s your smartwatch, your car, or your refrigerator making a purchase, these devices don’t store your actual card number. They store a digital token. From a financial management perspective, this reduces the “attack surface” of your bank account. If your phone is stolen, you can de-authorize the token without having to cancel your physical debit card and change the card number on all your other accounts.

The Future: Cardless Banking

We are beginning to see the rise of “cardless” transactions where the 16-digit number becomes entirely secondary. Biometric verification (fingerprints and facial recognition) and QR code payments are gaining traction. In these scenarios, the “card number” exists only in the background of the bank’s ledger, while the consumer interacts with their money through secure, encrypted digital identities. This transition represents the next frontier in financial security, moving us away from a world where a stolen string of numbers can lead to a drained bank account.

Conclusion: Empowering Your Financial Journey

The debit card number is more than just a sequence of digits; it is a vital piece of financial infrastructure. It represents your identity in the global market and serves as the gateway to your personal wealth. By understanding the anatomy of these numbers, recognizing their role in your daily transactions, and implementing high-level security protocols, you can take full control of your financial life.

In a world where digital threats are constant, being informed is your best defense. Treat your debit card number with the same respect you would treat the cash in your wallet. Use the tools provided by modern fintech—such as virtual numbers and tokenization—to add layers of protection to your account. Ultimately, the more you understand the mechanics of how your money moves, the better equipped you will be to grow and protect your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.