In the realm of personal finance, insurance is often viewed as a necessary evil—a recurring line item in the monthly budget that offers no immediate gratification. However, seasoned financial planners and savvy investors recognize insurance for what it truly is: the foundation of a robust financial plan. Determining “how much is insurance” is not merely about finding a single dollar amount; it is about understanding the variables that dictate premiums and the financial impact of the coverage you choose.

Insurance is essentially the “price of risk.” By paying a premium, you are transferring the financial burden of a catastrophic event—be it a medical emergency, a car accident, or the loss of a home—to an entity with deeper pockets. To navigate the complexities of insurance costs, one must delve into the factors that influence pricing across different sectors of the financial world.

Factors Influencing Your Insurance Premiums

The cost of insurance is rarely a flat fee. It is a highly personalized figure calculated through a process known as underwriting. Actuaries use vast amounts of data to predict the likelihood that a policyholder will file a claim. The higher the perceived risk, the higher the premium.

Risk Assessment and Demographic Data

For personal finance management, it is crucial to understand that your personal profile is the primary driver of cost. In life and health insurance, age and health history are the dominant factors. A 25-year-old non-smoker will pay significantly less for life insurance than a 50-year-old with a history of hypertension. In the world of auto insurance, your driving record and geographic location take center stage. Living in a high-crime area or an urban center with frequent traffic accidents will invariably drive up your rates.

Coverage Limits and Deductibles

The “how much” of insurance is also a reflection of how much risk you are willing to retain. This is balanced through coverage limits and deductibles. A deductible is the out-of-pocket amount you pay before the insurance company steps in. From a financial strategy standpoint, opting for a higher deductible can lower your monthly premium significantly. However, this requires a well-funded emergency savings account to ensure you can cover that deductible if a disaster occurs. Conversely, higher coverage limits—the maximum amount an insurer will pay—increase the premium because they increase the insurer’s potential liability.

Breaking Down the Costs of Essential Insurance Types

To answer how much insurance costs in a practical sense, we must categorize the expenses into the most common pillars of personal and business finance. Each category has its own pricing ecosystem.

Health Insurance: Premiums, Out-of-Pocket Maximums, and Deductibles

Health insurance is often the most expensive component of a household budget. In the United States, for instance, the average monthly premium for an individual can range from $400 to over $700, depending on the “metal level” (Bronze, Silver, Gold, or Platinum) of the plan.

- Bronze Plans: Typically have lower premiums but very high deductibles, making them suitable for healthy individuals who want protection against catastrophic illness.

- Gold/Platinum Plans: Feature high premiums but lower out-of-pocket costs, ideal for those who require frequent medical care.

When calculating the cost of health insurance, one must look beyond the premium and consider the “total cost of care,” which includes co-pays and the out-of-pocket maximum—the most you will have to pay for covered services in a plan year.

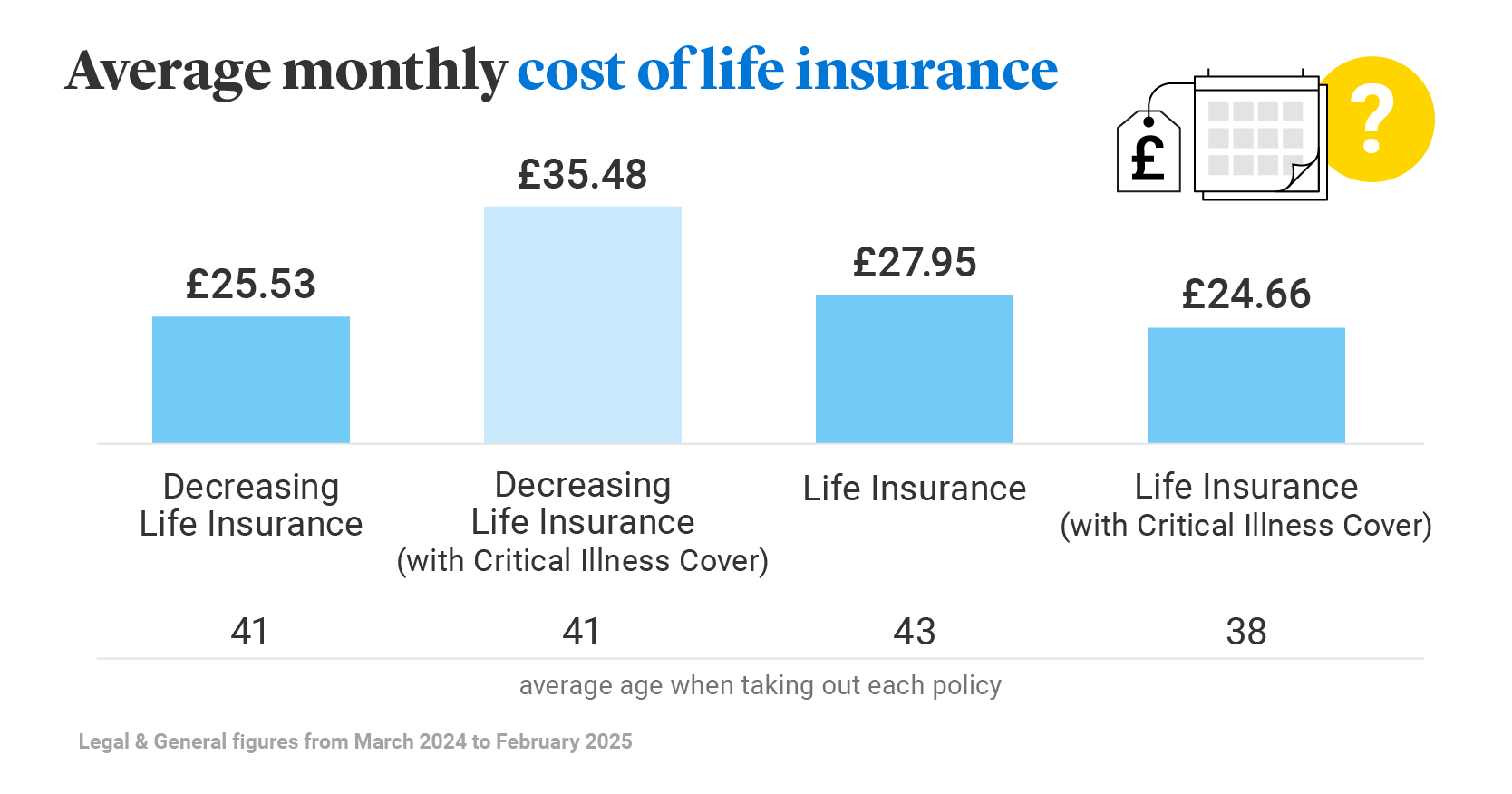

Life Insurance: Term vs. Whole Life Costs

Life insurance costs vary wildly based on the type of policy.

- Term Life Insurance: This is the most cost-effective way to protect your family’s financial future. For a healthy 30-year-old, a $500,000 policy for a 20-year term might cost as little as $20 to $30 per month. It provides a death benefit only.

- Whole Life/Permanent Insurance: These policies include a “cash value” component that acts as an investment vehicle. Because of this, premiums are often five to ten times higher than term life. While some use these for advanced estate planning, the high cost can be a deterrent for those focused on maximizing their liquid investment capital elsewhere.

Auto and Homeowners Insurance: Protecting Your Assets

Property and casualty insurance costs are dictated by the value of the assets being insured.

- Homeowners Insurance: The average cost is often tied to the replacement value of the home, not the market value. On average, homeowners might pay between $1,200 and $4,000 annually. Factors like proximity to a fire station, the age of the roof, and the local climate (flood or wildfire zones) play a massive role in the final quote.

- Auto Insurance: Costs are influenced by the make and model of the vehicle and the driver’s history. A standard policy for a moderate sedan might average $1,500 to $2,500 per year. In the context of business finance, commercial auto insurance will be higher due to increased liability risks.

Strategies to Lower Your Insurance Costs Without Sacrificing Coverage

Understanding the cost is the first step; the second is optimizing it. In personal finance, “cheap” insurance is often expensive in the long run if it doesn’t provide adequate protection. However, there are strategic ways to reduce premiums.

Bundling and Loyalty Discounts

Most insurance providers offer “multi-line” discounts. By placing your homeowners, auto, and umbrella liability policies with the same carrier, you can often save 10% to 25% across the board. This is a simple yet effective way to streamline your financial management and reduce outgoing cash flow.

Improving Your Credit Score and Financial Profile

In many jurisdictions, insurance companies use credit-based insurance scores to determine premiums. Statistically, individuals with higher credit scores are less likely to file claims. By managing your debt, paying bills on time, and maintaining a low credit utilization ratio, you aren’t just improving your ability to get a loan—you are actively lowering your insurance costs.

Regular Policy Audits and Comparison Shopping

The insurance market is highly competitive. Rates fluctuate based on a company’s current “appetite” for certain types of risk. A financial best practice is to audit your insurance policies every two years. Getting quotes from at least three different carriers ensures that you are not paying a “loyalty penalty” (where long-term customers are charged more than new customers).

The True Cost of Being Underinsured

When people ask “how much is insurance,” they are often looking for the lowest price. However, the most expensive insurance is the policy that doesn’t pay out when you need it, or the “missing” policy that leaves you exposed.

Calculating Potential Out-of-Pocket Catastrophes

Consider the financial impact of a total loss. If you opt for the bare minimum of state-required auto liability insurance (e.g., $25,000 for property damage) and you cause an accident involving a luxury electric vehicle, you could be personally liable for the remaining $60,000 or more. This could lead to wage garnishment or the forced liquidation of your investment accounts. In this light, paying an extra $20 a month for higher liability limits is a high-return investment in risk mitigation.

Insurance as a Wealth Preservation Tool

For high-net-worth individuals, insurance isn’t just about replacing a car or a roof; it’s about protecting an estate. Umbrella insurance is a prime example. For a relatively low cost (often $300–$500 a year for $1 million in coverage), an umbrella policy sits on top of your existing home and auto policies to provide an extra layer of liability protection. This ensures that a single lawsuit does not derail decades of wealth accumulation.

Conclusion: Balancing the Budget and the Safety Net

The question “how much is insurance” ultimately leads to a deeper discussion about financial values and risk tolerance. While the average American household may spend several thousand dollars a year on various premiums, this expenditure should be viewed as a vital safeguard for your net worth.

To manage your insurance costs effectively, focus on the variables you can control: maintain a clean driving record, improve your credit score, choose deductibles that align with your emergency fund, and shop around regularly. By integrating insurance planning into your broader financial strategy, you transform an abstract expense into a powerful tool for financial security and long-term peace of mind. Insurance is not just a cost of living; it is the price of ensuring that your financial journey remains on track, regardless of the obstacles that may arise.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.