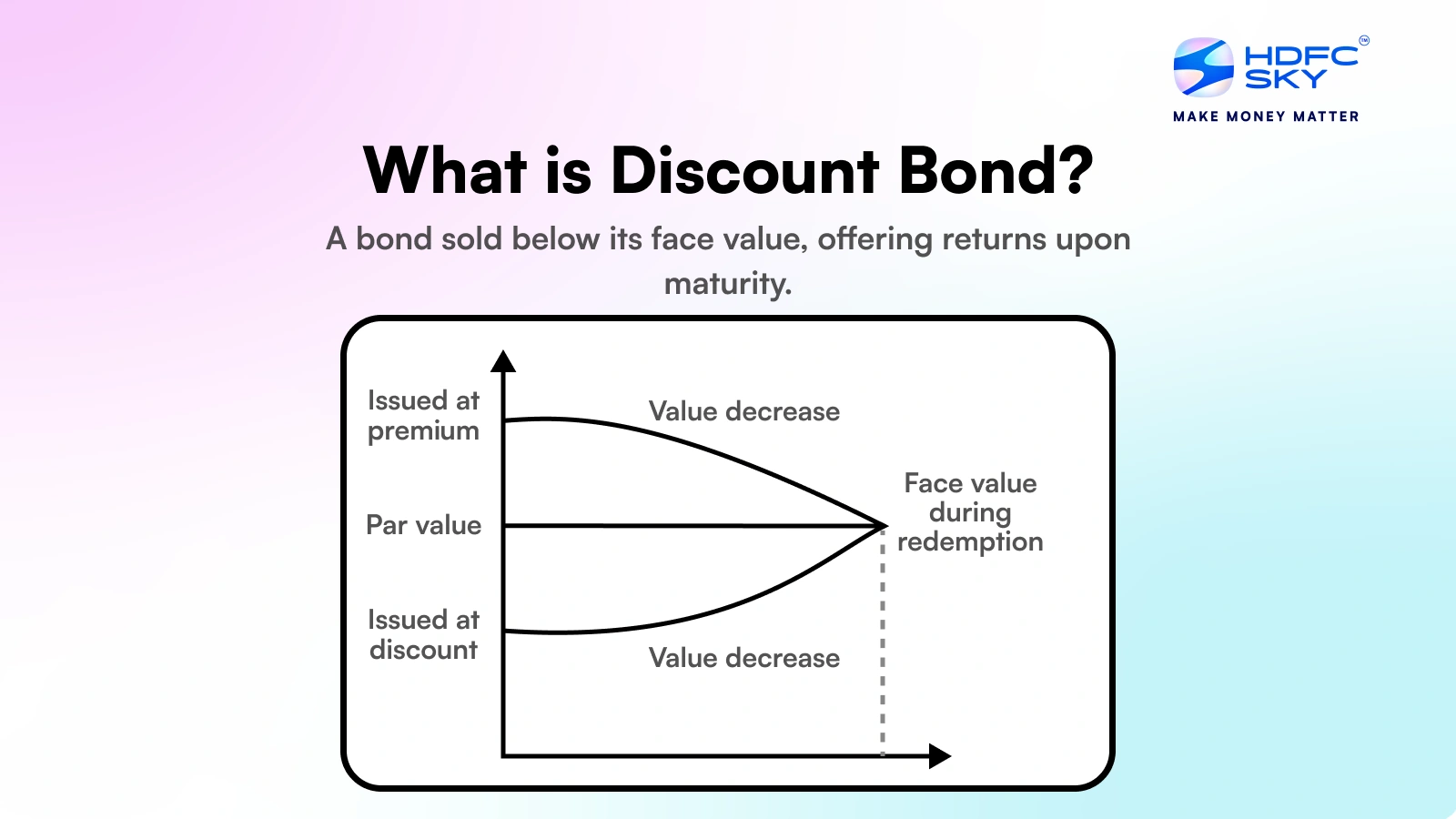

In the world of fixed-income investing, the term “discount bond” often piques the interest of both novice investors and seasoned portfolio managers. While the word “discount” in a retail setting usually implies a bargain or a sale, its meaning in the financial markets is more technical, though no less significant for one’s bottom line. At its core, a discount bond is a debt instrument that is issued or currently trading for less than its par (face) value.

Understanding the mechanics of discount bonds is essential for anyone looking to navigate the bond market, manage interest rate risk, or build a diversified investment portfolio. This article explores the nature of discount bonds, why they exist, how to calculate their value, and the strategic role they play in modern personal and business finance.

The Mechanics and Characteristics of Discount Bonds

To understand a discount bond, one must first understand the anatomy of a standard bond. A bond is essentially a loan made by an investor to a borrower (typically a corporation or government). The borrower promises to pay back the “par value” (usually $1,000) at a specific date in the future (the maturity date) and usually pays periodic interest, known as the coupon.

Par Value vs. Market Price

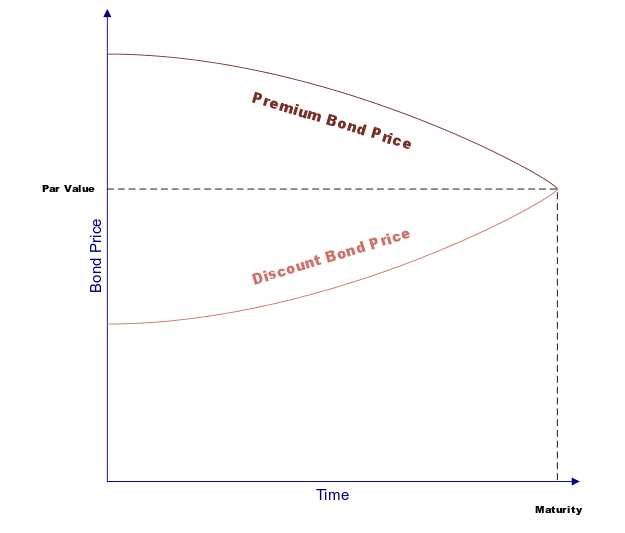

The par value is the amount the bondholder will receive when the bond matures. However, once a bond is issued, it begins trading on the secondary market, where its price fluctuates based on economic conditions. If the market price falls below $1,000, the bond is said to be trading at a discount. For example, if you purchase a bond for $950 that has a face value of $1,000, you have purchased a discount bond.

Zero-Coupon Bonds: The Purest Form

The most common type of discount bond is the “zero-coupon bond.” As the name suggests, these bonds do not make regular interest payments. Instead, they are issued at a deep discount to their face value. The investor’s return is the difference between the purchase price and the par value received at maturity. U.S. Treasury Bills (T-Bills) are a classic example of zero-coupon discount bonds; they are sold at a discount and mature at face value, providing a predictable return for the holder.

Secondary Market Discounts

Not all discount bonds start that way. Many bonds are issued “at par” (at full face value) but later drop in price on the secondary market. This happens because the bond’s fixed coupon rate becomes less attractive compared to newer bonds being issued at higher current market rates. To remain competitive and find a buyer, the older bond’s price must drop until its total yield aligns with current market expectations.

Why Do Bonds Trade at a Discount?

There are several economic and fundamental reasons why a bond’s price might dip below its face value. Understanding these drivers is crucial for assessing whether a discount bond represents a “value buy” or a “value trap.”

The Inverse Relationship with Interest Rates

The primary driver of bond prices is the movement of interest rates. There is an inverse relationship between the two: when market interest rates rise, bond prices fall. Imagine you own a bond paying a 3% interest rate. If the Federal Reserve raises rates and new bonds are issued at 5%, no investor will want to buy your 3% bond at full price. To sell it, you must lower the price (create a discount) so that the buyer’s total return (the 3% interest plus the capital gain from the discount) equals the 5% they could get elsewhere.

Credit Rating Downgrades

A bond’s price also reflects the perceived risk of the issuer. If a corporation’s financial health deteriorates, credit rating agencies (like Moody’s or S&P) may downgrade the company’s debt. A lower credit rating implies a higher risk of default. To compensate investors for taking on this increased risk, the market price of the bond will drop, causing it to trade at a discount. In this scenario, the discount reflects a “risk premium.”

Liquidity and Market Sentiment

Sometimes, bonds trade at a discount due to a lack of liquidity. If there are many sellers and few buyers for a particular niche bond, the price may be driven down below its intrinsic value. Additionally, broader market sentiment—such as a flight to cash during a financial crisis—can lead to a sell-off in corporate bonds, pushing prices into discount territory across the board, regardless of the individual issuers’ health.

Calculating Returns: Yield to Maturity and Tax Implications

For a “Money” focused investor, the nominal price of a bond is less important than its “yield.” When buying a discount bond, the math of your return becomes slightly more complex than simply looking at the coupon rate.

Current Yield vs. Yield to Maturity (YTM)

The “Current Yield” is a simple calculation: the annual coupon payment divided by the bond’s current price. However, this does not tell the whole story for a discount bond. The more accurate measure is the Yield to Maturity (YTM). YTM accounts for the annual interest payments plus the capital gain you realize when the bond matures at par. If you buy a bond at $900 and it matures at $1,000 in five years, that $100 gain is a significant part of your total return, and YTM captures that “internal rate of return.”

The Capital Gains Element

The primary appeal of a discount bond is the built-in capital appreciation. Because you know the bond will (ideally) pay back its full face value at maturity, the “pull to par” provides a predictable growth component. For investors who do not need immediate cash flow from high coupon payments, the capital gain from a discount bond can be an effective way to grow wealth over a fixed horizon.

Taxation and the OID Rule

Taxation is a critical consideration for any financial tool. In many jurisdictions, the “Original Issue Discount” (OID) on a bond is treated as interest income rather than a capital gain. This means you may be required to pay taxes on a portion of the discount each year you hold the bond, even though you haven’t actually received the cash yet. This is often referred to as “phantom income.” However, for bonds bought at a discount on the secondary market (market discount), the rules may differ, sometimes allowing the gain to be taxed only upon sale or maturity. Always consult a tax professional when dealing with deep discount instruments.

Strategic Advantages and Risks for Investors

Investing in discount bonds is a strategic choice that offers specific advantages, but it also carries unique risks that must be managed.

Lower Capital Outlay

One of the most practical benefits of discount bonds is the lower entry price. For individual investors or small businesses, buying bonds at a discount allows for the acquisition of a larger face value of debt for less upfront cash. This can be particularly useful for “laddering” a portfolio, where an investor buys bonds with different maturity dates to ensure a steady stream of capital returning at intervals.

Increased Sensitivity to Interest Rates (Duration)

Investors should be aware that discount bonds, especially zero-coupon bonds, have higher “duration.” Duration is a measure of a bond’s sensitivity to interest rate changes. Because a large portion of the return on a discount bond is back-loaded (received at maturity), its price will swing more violently when interest rates move compared to a bond that pays high frequent coupons. This makes discount bonds excellent tools for speculating on falling interest rates, but risky during periods of rising rates.

Reinvestment Risk Mitigation

A significant advantage of zero-coupon discount bonds is the elimination of reinvestment risk. When you receive regular coupon payments from a standard bond, you have to find a place to reinvest that money. If interest rates have fallen, you’ll be reinvesting at a lower rate. With a zero-coupon discount bond, your “interest” is effectively locked in at the purchase price, compounding automatically until maturity.

Real-World Applications in Personal and Corporate Finance

Discount bonds are not just theoretical constructs; they are used daily by governments, corporations, and individuals to achieve specific financial goals.

U.S. Treasury Bills and Savings Bonds

The U.S. government is one of the largest issuers of discount debt. T-Bills are short-term instruments (maturing in one year or less) that do not pay interest but are sold at a discount. They are considered among the safest investments in the world. Similarly, Series EE Savings Bonds were historically sold at half their face value, acting as a long-term discount instrument for individual savers.

Corporate “Deep Discount” and Distressed Debt

In the corporate world, companies may issue deep discount bonds to lower their immediate cash flow burden, as they won’t have to make large interest payments during the life of the bond. On the other hand, “distressed debt” investors look for bonds of companies in financial trouble. These bonds might trade at 40 or 50 cents on the dollar. If the company successfully restructures or recovers, the investor stands to make a massive profit as the bond’s price moves back toward par.

Municipal Bonds and Tax-Exempt Growth

Many municipal bonds (issued by cities or states) are offered at a discount. For high-net-worth investors, these can be doubly attractive. Not only do they offer the capital appreciation of a discount bond, but the interest (and sometimes the discount itself) may be exempt from federal and state taxes. This makes them a powerful tool for tax-efficient wealth preservation.

Conclusion

A discount bond is more than just a “cheap” security; it is a sophisticated financial instrument that reflects the complex interplay between time, risk, and interest rates. Whether you are an individual investor looking for a predictable way to fund a future liability like college tuition, or a business manager seeking to understand the cost of debt, the discount bond is a fundamental concept in the “Money” niche. By understanding how to calculate yields, manage duration risk, and navigate tax implications, you can leverage discount bonds to build a more resilient and profitable financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.