The intersection of geopolitical stability and financial markets is perhaps nowhere more visible than in the moments following a national tragedy. On November 22, 1963, at 12:30 p.m. CST, the world changed forever as President John F. Kennedy was assassinated in Dallas, Texas. While the human and political toll was immeasurable, the financial world faced its own immediate crisis. For investors, the event serves as one of the most significant case studies in market psychology, liquidity management, and the inherent resilience of the American economy.

To understand what happened to the stock market after Kennedy’s death, one must look beyond the initial panic and analyze the structural recovery that followed. This event provides timeless lessons for modern personal finance and institutional investing, demonstrating how markets react to “Black Swan” events and how fundamental economic strength often outweighs short-term volatility.

The Immediate Shock: Thirty Minutes of Financial Chaos

The news of the shooting reached the floor of the New York Stock Exchange (NYSE) shortly before 2:00 p.m. EST. In an era long before high-frequency trading and instant digital alerts, the speed with which the market reacted was still staggering. As rumors solidified into reports of the President’s death, a wave of panic-selling hit the floor, threatening to collapse the entire financial apparatus of the United States.

The Decision to Close the Markets

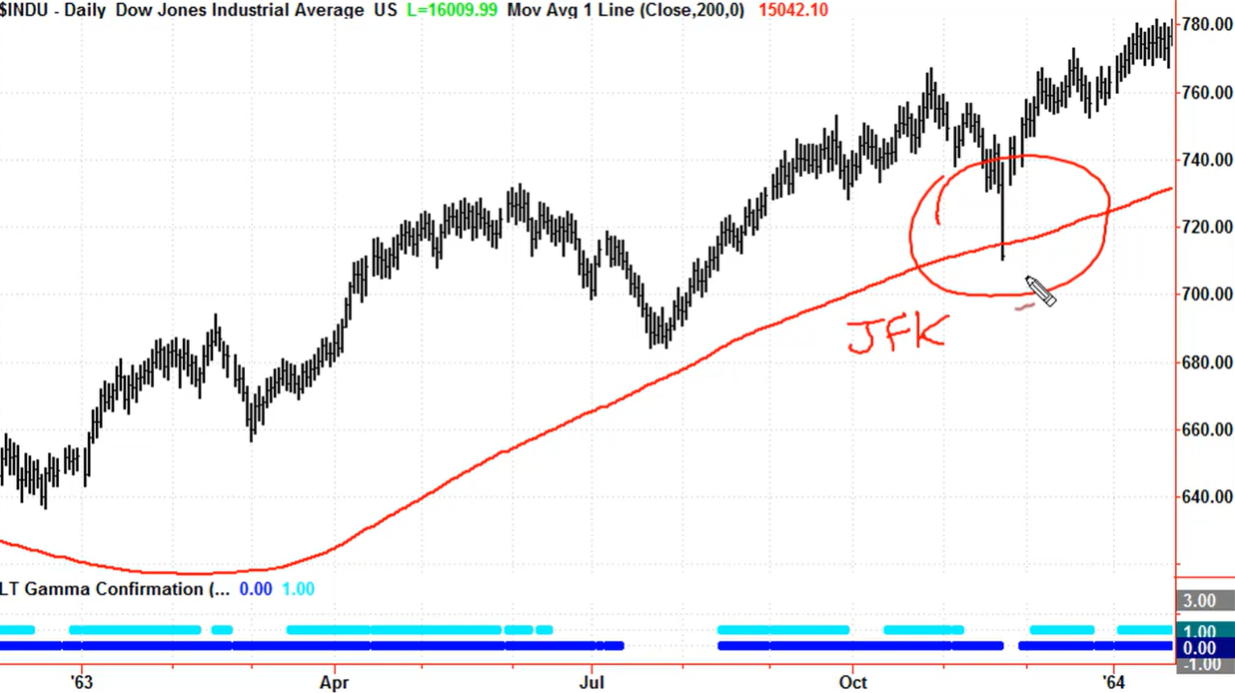

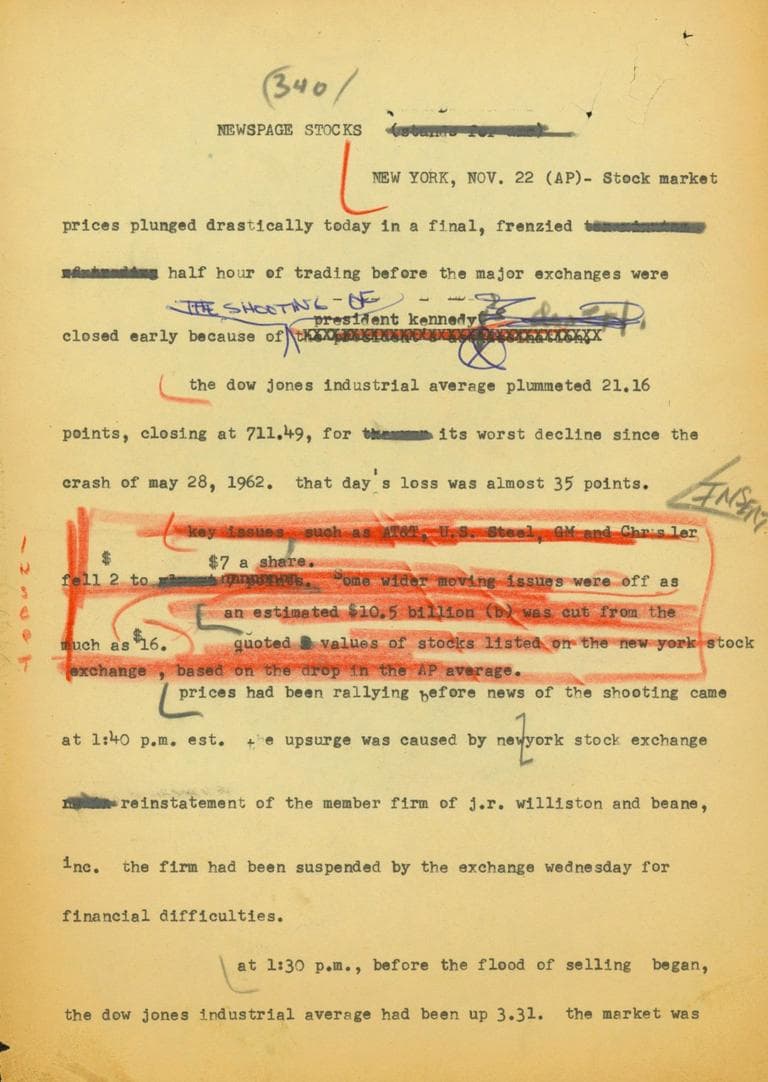

As the Dow Jones Industrial Average (DJIA) began a vertical descent, the governors of the NYSE faced a critical decision. In less than 30 minutes, the Dow had plunged roughly 21.16 points—a nearly 2.9% drop, which was a massive move for the early 1960s. Recognizing that the selling was driven by blind panic rather than economic data, the NYSE board took the extraordinary step of closing the exchange at 2:07 p.m. EST, roughly 83 minutes before the scheduled close.

This move was essential for maintaining order. By halting trade, the exchange allowed investors time to process the transition of power and prevented a “feedback loop” of selling that could have wiped out billions in market capitalization overnight. It remains a landmark example of how market circuit breakers—both formal and informal—protect the integrity of the financial system.

Market Volatility and the “Tape” Lag

One of the unique aspects of the 1963 crash was the technical limitation of the time. The “ticker tape,” which provided price updates to brokers across the country, could not keep up with the volume of sell orders. At one point, the tape was running 20 minutes behind the actual trades happening on the floor. This information gap exacerbated the fear; investors were selling stocks without knowing their current price, effectively “flying blind” into a financial storm. For modern investors, this highlights the value of the instant liquidity and transparency we enjoy today, which helps mitigate the kind of information-vacuum panic seen in 1963.

The Pre-Assassination Context: The “Kennedy Slide” and Economic Tensions

To fully grasp the market’s reaction to the assassination, we must look at the preceding years. Kennedy’s relationship with Wall Street had been historically fraught, a factor that influenced how investors viewed the sudden change in leadership.

The 1962 Flash Crash and the Steel Conflict

In 1962, the market experienced what was known as the “Kennedy Slide.” The Dow dropped 27% during the first half of the year, driven in part by a public and bitter confrontation between the President and the leaders of the steel industry. Kennedy’s intervention in steel pricing was viewed by many in the financial community as an overreach of executive power, leading to a period of deep mistrust between the White House and the “Money” interests of New York.

Consequently, entering late 1963, the market was already sensitive to Kennedy’s policies. However, the economy itself was fundamentally strong. Corporate earnings were rising, and the post-WWII economic boom was still in effect. This dichotomy—a strong economy paired with political uncertainty—set the stage for the market’s eventual and rapid recovery after the assassination.

Investment Sentiment Before Dallas

In the weeks leading up to November 1963, the market had actually been performing well, nearing record highs. The suddenness of the assassination did not just represent a loss of a leader; it represented a potential threat to the “New Frontier” economic policies Kennedy had championed, including proposed tax cuts that were expected to stimulate further growth. The initial crash was not a vote of no confidence in the American economy, but rather a reaction to the sudden vacuum of power and the uncertainty of what Vice President Lyndon B. Johnson’s administration would hold.

The Great Rebound: Monday’s Recovery and the Johnson Transition

The NYSE remained closed on Saturday and Monday (November 25), the latter being a national day of mourning. When the markets finally reopened on Tuesday, November 26, the financial community witnessed one of the most dramatic reversals in history.

The Reopening Surge

Expectations for Tuesday’s opening were mixed, with many fearing a continuation of the Friday sell-off. Instead, the market opened with a massive “buy” bias. The Dow Jones Industrial Average surged 32.03 points—a 4.5% increase—completely erasing the losses from the day of the assassination and then some. At the time, it was the largest single-day point gain in the history of the NYSE.

This recovery was fueled by several factors:

- Institutional Stability: The Federal Reserve and major New York banks stepped in to ensure there was plenty of liquidity in the system.

- The Smooth Transition of Power: Lyndon B. Johnson’s swift swearing-in aboard Air Force One and his subsequent address to the nation reassured the public that the government remained functional.

- Bargain Hunting: Sophisticated investors recognized that the Friday drop was an emotional reaction, not a fundamental one. Large-scale “value” buying began the moment the opening bell rang.

Lyndon B. Johnson’s “Business-Friendly” Stance

As the market processed the transition, investors began to realize that LBJ might actually be more favorable to the business community than JFK had been. Johnson was a master of legislative maneuvering and was seen as more likely to pass the tax cuts Kennedy had proposed. This “pro-growth” sentiment provided the tailwinds necessary for a sustained bull market throughout much of 1964. The “Money” niche often speaks of “policy certainty,” and LBJ provided that in the wake of the tragedy.

Lessons for Modern Personal Finance and Investing

The events following the JFK assassination offer profound insights for today’s investors, particularly those navigating the high-speed, often volatile modern landscape of digital finance and global instability.

The Danger of Panic-Selling

The most obvious lesson from 1963 is the high cost of emotional investing. Those who sold their holdings in the frantic thirty minutes on Friday afternoon locked in losses that were entirely reversed just one trading day later. In personal finance, this reinforces the “stay the course” philosophy. Market shocks are often temporary, and the fundamental value of a diversified portfolio is rarely changed by a single political event, however tragic.

Understanding “Black Swan” Resilience

Nassim Taleb’s concept of the “Black Swan”—an unpredictable event with extreme consequences—perfectly describes the Kennedy assassination. While such events cause short-term trauma, history shows that the U.S. stock market has an incredible capacity for “anti-fragility.” Whether it was the assassination of JFK, the attacks on 9/11, or the 2008 financial crisis, the market has historically rebounded because it is built on the underlying productivity of corporations and the labor force, not just the stability of a single individual.

The Role of Market Closures and Regulation

The 1963 closure of the NYSE was a manual precursor to the automated “circuit breakers” we use today. For the modern investor, understanding these mechanisms is crucial. They are not designed to stop the market from moving, but to stop it from moving irrationally. In an era of AI-driven trading and social media-fueled bank runs, the lesson of 1963 is that “time” is the greatest enemy of panic. Giving the market time to digest news is often the best way to preserve capital.

Conclusion: The Endurance of the Financial System

The assassination of John F. Kennedy remains one of the darkest chapters in American history. Yet, from the perspective of financial markets, it serves as a testament to the durability of the American economic experiment. The stock market’s rapid descent and even faster recovery in November 1963 highlight a fundamental truth about investing: while politics can influence the “mood” of the market, the long-term trajectory of wealth is driven by economic fundamentals and the continuity of institutions.

For the modern investor, the events of 1963 are a reminder that the best strategy in the face of uncertainty is often no strategy at all. By maintaining a disciplined approach to personal finance and resisting the urge to react to the “tape,” individuals can protect their assets from the temporary shocks of history. The market eventually looks past the tragedy to the reality of the balance sheet, proving that even in the face of national grief, the wheels of commerce and the growth of capital remain remarkably persistent.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.