When discussing personal finance, most people focus on the accumulation phase—investing, saving, and growing a portfolio. However, the preservation and eventual transfer of that wealth are equally critical components of a comprehensive financial strategy. At the heart of this transition lies a pivotal figure: the executor. While often viewed through a legal lens, the role of an executor is, at its core, one of intensive financial management and fiduciary stewardship.

An executor is the person or entity designated in a will to manage a deceased person’s estate. In the realm of money management, they act as the temporary CEO of a person’s lifetime financial output. Their responsibility is to ensure that every asset is accounted for, every debt is settled, and every remaining cent is distributed according to the deceased’s wishes. It is a role that requires a high degree of financial literacy, organizational prowess, and an unwavering commitment to ethical conduct.

The Fiduciary Foundation: Managing Wealth with Integrity

The most important concept to understand regarding the role of an executor is “fiduciary duty.” In the world of finance, a fiduciary is legally obligated to act in the best interest of another party. For an executor, this means putting the interests of the estate and its beneficiaries above their own.

Legal Accountability and Financial Liability

An executor does not just handle money; they are legally responsible for it. If an executor mismanages estate funds—for example, by making speculative investments with the estate’s cash or failing to pay taxes on time—they can be held personally liable for the losses. This financial risk underscores why the role is so significant. They must maintain a “paper trail” that would survive a rigorous audit, documenting every transaction, fee, and distribution made during their tenure.

Immediate Financial Safeguarding

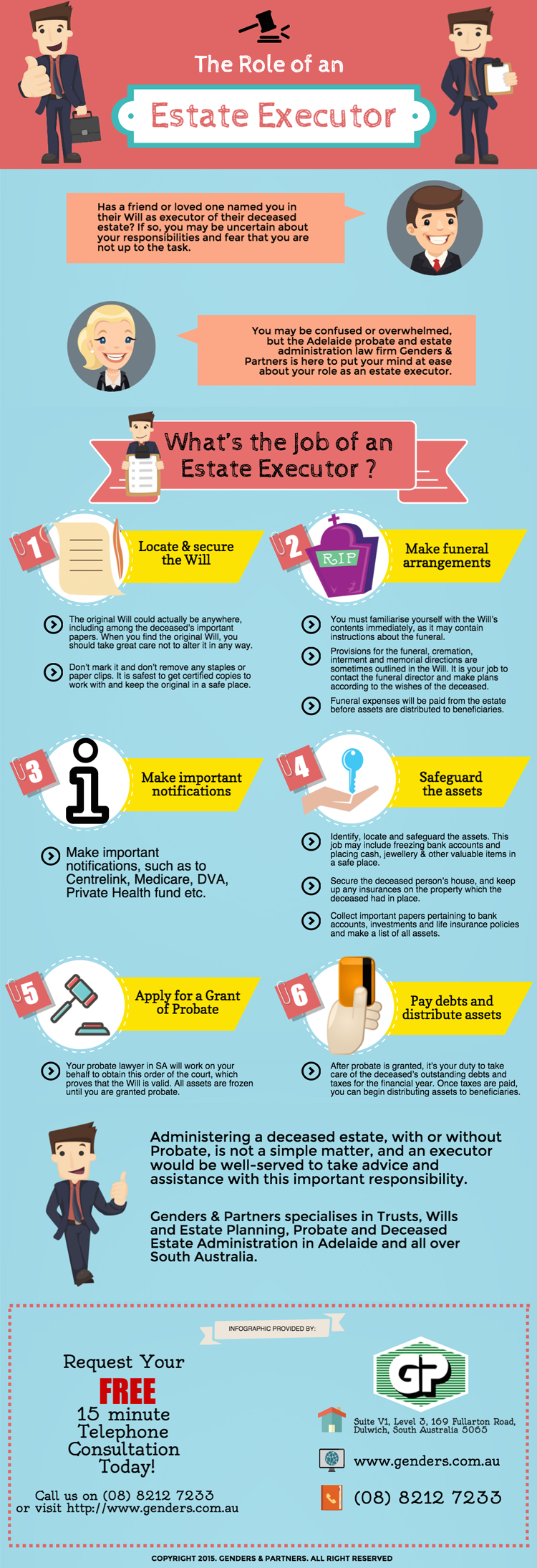

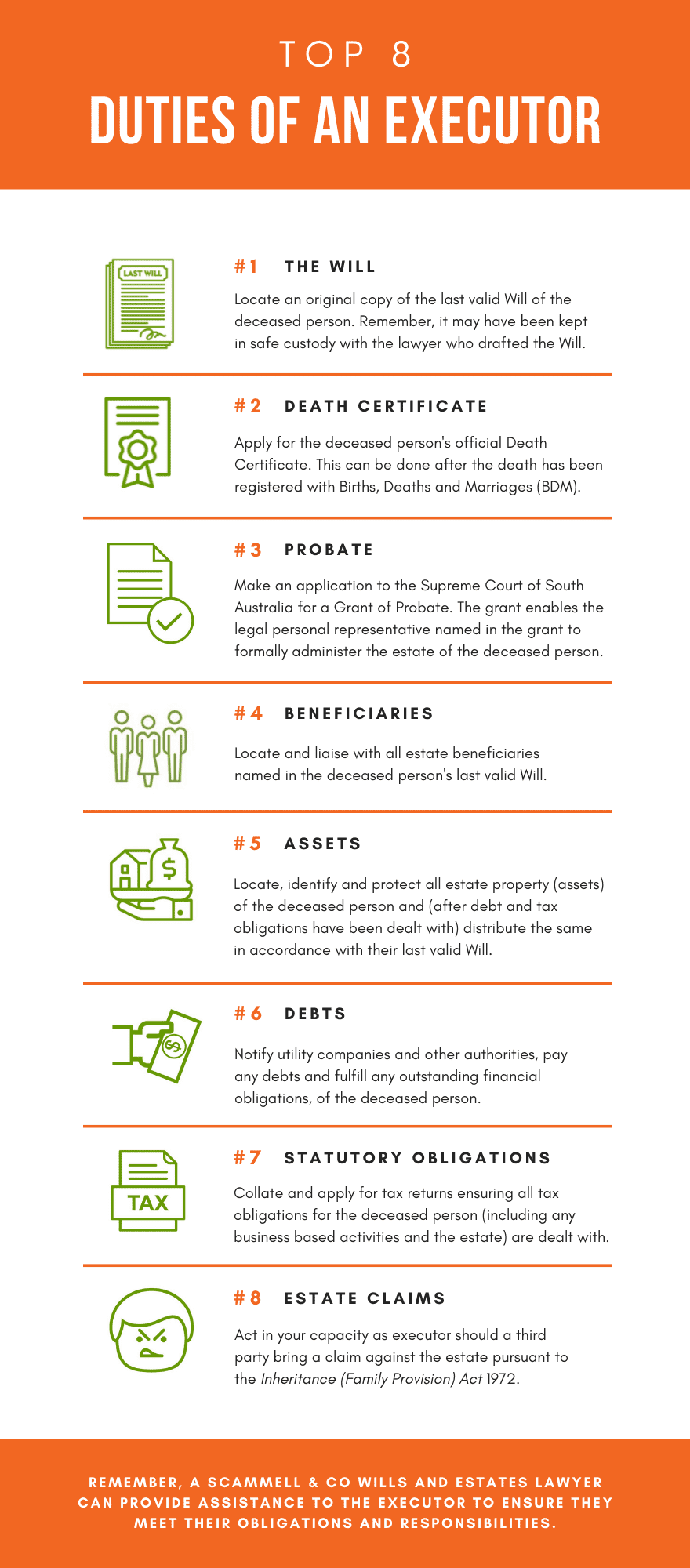

Upon the death of the estate owner, the executor’s first financial task is one of preservation. This involves “marshalling the assets.” They must secure physical property, such as real estate and vehicles, but more importantly, they must secure liquid assets. This often involves notifying banks and brokerage firms to freeze accounts or transition them into estate accounts. By preventing unauthorized access or “leakage” of funds, the executor ensures that the financial legacy remains intact for the eventual heirs.

The Financial Roadmap: Inventory, Valuation, and Debt Settlement

The middle phase of an executor’s journey is the most labor-intensive from a financial perspective. It requires a meticulous deep dive into the deceased’s financial history to create a comprehensive balance sheet.

Identifying and Valuing Assets

An executor must locate every bank account, investment portfolio, retirement fund, and insurance policy. In today’s digital age, this also includes identifying “invisible” assets like cryptocurrency wallets, digital storefronts, and online payment accounts. Once identified, these assets must be valued. For complex estates, the executor must hire professional appraisers for real estate, art, or specialized collections. This valuation is not just for the beneficiaries; it is a critical requirement for calculating potential estate taxes.

Navigating the Creditor Hierarchy

Before a single dollar can be distributed to a beneficiary, the executor must settle the estate’s liabilities. This is where the financial complexity peaks. The executor is responsible for notifying creditors and determining the validity of claims against the estate. They must follow a specific legal hierarchy for payment—typically starting with funeral expenses and administrative costs, followed by taxes and then general debts. If an executor distributes money to heirs before paying valid creditors, they may find themselves in a position where they have to claw back those funds or pay the creditors out of their own pocket.

Tax Strategy and Compliance

Perhaps the most daunting financial task is managing the tax obligations. The executor is responsible for filing the deceased’s final income tax return, as well as an income tax return for the estate itself if it earns income during the probate process. Furthermore, if the estate exceeds certain thresholds, the executor must file federal and state estate tax returns. Navigating these requirements requires a sophisticated understanding of tax law or the foresight to hire an expert CPA to ensure the estate doesn’t lose money to unnecessary penalties or overpayment.

Business Continuity and Investment Oversight

The role of an executor becomes significantly more complex when the deceased was a business owner or a sophisticated investor. In these cases, the executor acts as a bridge, ensuring that financial value does not evaporate during the transition.

Managing Business Interests and Partnerships

If the deceased owned a business or held a stake in a partnership, the executor must step in to oversee those interests. This might involve voting on shares, managing payroll in the short term, or executing a buy-sell agreement. The goal is to maintain the “going concern” value of the business. Without active management by an executor, a thriving business can quickly lose value, devastating the financial return for the beneficiaries.

Investment Management During Probate

Probate—the legal process of settling an estate—can take anywhere from six months to several years. During this time, the executor is responsible for the estate’s investment portfolio. They must decide whether to liquidate stocks to move into safer cash equivalents or maintain an existing investment strategy. This requires a balanced approach; they must avoid unnecessary risks while also ensuring that the estate’s purchasing power isn’t eroded by inflation. The executor must act as a prudent investor, often relying on the “Prudent Investor Rule,” which mandates that they manage the assets as a cautious person would manage their own.

The Distribution Process and Final Accounting

The culmination of the executor’s work is the distribution of the remaining wealth. This is the stage where the financial planning of the deceased finally comes to fruition.

Asset Liquidation vs. In-Kind Distribution

The executor must determine the most efficient way to transfer wealth. In some cases, the will specifies that certain assets (like a family home) be distributed “in-kind” to a specific person. In other cases, the executor may need to liquidate assets—selling real estate, stocks, or jewelry—to create a pool of cash that can be divided among several beneficiaries according to percentage allocations. This process requires a keen eye for market timing and transaction costs to ensure the estate receives the maximum possible value.

Final Reporting and Closing the Estate

Before the executor can be relieved of their duties, they must provide a “final accounting” to the court and the beneficiaries. This document is a comprehensive summary of every penny that entered and left the estate under their watch. It lists the initial inventory, any income earned, debts paid, and the proposed final distribution. Only once the beneficiaries and the court approve this accounting can the executor distribute the funds and officially close the estate. This transparency is the final safeguard in the financial management process.

Choosing the Right Executor: Financial Competence vs. Personal Connection

Given the heavy financial and administrative burden, the selection of an executor is one of the most important personal finance decisions an individual can make. It is a choice between emotional trust and technical capability.

Professional vs. Lay Executors

Many people choose a spouse or an adult child to serve as their executor. While this person likely has the best intentions, they may lack the financial acumen required to handle complex tax filings or investment management. This is why many high-net-worth individuals opt for a professional executor—such as a trust company or a bank’s wealth management department. While these entities charge a fee for their services, their expertise can often save the estate more money in avoided taxes and penalties than the cost of their commission.

The Cost of Execution

In the world of money, nothing is free, and the role of an executor is no exception. Executors are generally entitled to compensation for their time and effort, usually calculated as a percentage of the estate’s value or an hourly rate. These fees are a legitimate expense of the estate. When planning an estate, it is vital to account for these costs, as they will reduce the total amount available for heirs. Understanding this fee structure helps in selecting an executor who provides the best value for their level of expertise.

Conclusion: The Ultimate Financial Service

The role of an executor is a demanding, high-stakes position that sits at the intersection of law and finance. It is far more than a ceremonial title; it is a functional job that requires the skills of an accountant, a project manager, and a fiduciary agent. By ensuring that assets are protected, debts are settled, and taxes are paid, the executor performs the final act of financial service for the deceased, securing their legacy and providing for the financial future of the next generation. Whether you are currently drafting a will or have been asked to serve as an executor, understanding these financial mechanics is essential to ensuring that the transition of wealth is handled with the precision and integrity it deserves.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.