In the hierarchy of global commodities, few materials hold as much weight—literally and metaphorically—as iron ore. While gold captures the headlines of “safe-haven” assets and lithium dominates conversations regarding the green energy transition, iron ore remains the foundational bedrock of the global economy. It is the primary raw material used to produce steel, which in turn fuels infrastructure, urbanization, and industrial manufacturing. For the savvy investor or the finance professional, understanding “what is the ore for iron” is not merely a geological inquiry; it is a fundamental deep dive into a trillion-dollar market that dictates the pulse of global trade.

To understand the financial implications of this commodity, one must look past the red dust and into the balance sheets of multinational mining conglomerates and the sovereign wealth funds of emerging economies. This article explores iron ore through the lens of investment, market dynamics, and the economic forces that transform raw minerals into financial wealth.

Understanding Iron Ore: The Bedrock of Global Trade

To participate in the commodity markets, an investor must first understand the quality and composition of the asset. In the financial world, not all iron ore is created equal. The “ore for iron” typically refers to rocks and minerals from which metallic iron can be economically extracted. From a business perspective, the focus is on the concentration of iron and the level of impurities, as these factors determine the profit margins of extraction and smelting.

From Earth to Industry: Defining the Asset

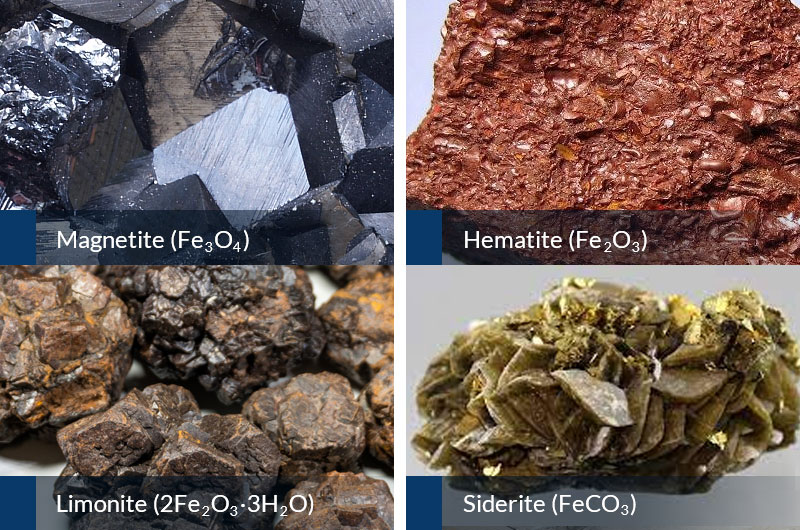

Iron ore is essentially a mineral substance which, when heated in the presence of a reducing agent such as coke, yields metallic iron (Fe). The most common ores are hematite ($Fe2O3$) and magnetite ($Fe3O4$). For a mining project to be bankable, the ore must typically contain a high percentage of iron—usually above 50% for direct shipping ores. Lower-grade deposits require extensive “beneficiation,” a process that increases the iron content but also adds significant capital expenditure (CAPEX) and operational expenditure (OPEX) to the project.

Hematite vs. Magnetite: Value Discrepancies in the Market

In the commodity exchange, the distinction between hematite and magnetite is crucial. Hematite is often referred to as “Direct Shipping Ore” (DSO) because it can be mined and sent straight to a blast furnace with minimal processing. This makes hematite-rich regions, like the Pilbara in Western Australia, high-margin goldmines for companies like Rio Tinto and BHP.

Magnetite, while generally lower in raw iron content (around 25-30%), is highly magnetic, allowing for easier separation from impurities. Once processed into a concentrate, magnetite often reaches a higher purity (65%+ Fe) than standard hematite. In today’s market, high-grade magnetite pellets often command a premium price because they require less coal to smelt, aligning with the growing financial trend of ESG (Environmental, Social, and Governance) investing.

The Economics of Extraction and Supply Chain Dominance

The iron ore market is characterized by a high degree of consolidation. Unlike the fragmented gold mining industry, the global supply of iron ore is largely controlled by a handful of “supermajors.” This oligopolistic structure has a profound impact on price discovery and investment returns.

The Major Players: Rio Tinto, Vale, and BHP

Three companies dominate the global landscape: Rio Tinto (Australia/UK), Vale (Brazil), and BHP (Australia). These entities function as the “central banks” of the iron ore world. When Vale experiences a production disruption—such as the Brumadinho dam disaster in 2019—the global price of iron ore can spike by 30% or more overnight. For an investor, these companies offer a way to gain exposure to the commodity while benefiting from sophisticated management and robust dividend yields. Their ability to maintain low cash costs—sometimes as low as $15 to $20 per tonne—while selling at market prices that fluctuate between $80 and $150 per tonne, results in massive free cash flow.

Geopolitical Factors and the “Big Three” Influence

The geography of iron ore creates a fascinating geopolitical tension. Australia and Brazil account for the vast majority of seaborne exports. This creates a dependency for industrial nations, particularly China, which produces more than half of the world’s steel but lacks high-grade domestic ore. Consequently, the iron ore market is often used as a tool for economic diplomacy. Changes in trade tariffs, freight rates (tracked by the Baltic Dry Index), and port inventories in Tianjin or Qingdao are leading indicators of broader macroeconomic shifts.

Market Volatility and the Primary Price Drivers

For those looking to generate income from the commodity sector, understanding price volatility is essential. Iron ore is a cyclical asset, and its price is a “canary in the coal mine” for global economic health.

The China Connection: Infrastructure and Real Estate

You cannot talk about the money in iron ore without talking about China. For the past two decades, China’s massive urbanization and infrastructure stimulus have been the primary drivers of demand. When the Chinese government eases credit for property developers or announces a new high-speed rail network, the demand for steel—and thus iron ore—surges. Conversely, when the Chinese real estate market faces a liquidity crisis (as seen with the Evergrande collapse), the price of iron ore tends to retreat. Investors must keep a close eye on the Chinese Politburo’s economic policies as much as they do on the mining companies’ quarterly reports.

Decarbonization and the Premium on High-Grade Ore

A new financial driver has emerged in recent years: the “Green Premium.” The steel industry is responsible for approximately 7-9% of global CO2 emissions. To meet net-zero targets, steelmakers are shifting toward Electric Arc Furnaces (EAF) and Hydrogen-based Direct Reduced Iron (DRI) technologies. These technologies require much higher-grade iron ore (typically 67% Fe or higher). This shift is creating a bifurcated market where high-grade “green” ore sells at a significant premium over standard 62% Fe benchmarks. This transition represents a major investment opportunity in companies that own high-grade assets or innovative beneficiation technologies.

Investment Strategies for the Commodity Sector

How does an individual or institutional investor capitalize on the “ore for iron”? There are several avenues, each with its own risk-reward profile.

Direct Stocks vs. ETFs: Managing Risk

The most common way to invest is through the equity of mining companies. Stocks like Rio Tinto (RIO) or Fortescue (FMG) offer direct exposure to the iron ore price but also carry “company risk,” such as management failures or labor strikes. For those seeking broader exposure, Exchange-Traded Funds (ETFs) such as the iShares MSCI Global Metals & Mining Producers ETF (PICK) provide a diversified basket of companies involved in the extraction of iron and other industrial metals. This mitigates the risk of a single mine failure while still capturing the upside of a commodity bull market.

Futures Contracts: A Tool for Institutional Investors

For more sophisticated investors, the Singapore Exchange (SGX) and the Dalian Commodity Exchange (DCE) offer iron ore futures. These financial instruments allow traders to speculate on the future price of the ore or hedge against price drops. Because futures are highly leveraged, they offer the potential for significant gains, but they also require a deep understanding of market mechanics and margin requirements. For most retail investors, sticking to equities or ETFs is a more prudent path to long-term wealth accumulation.

The Future of Iron Ore: Green Steel and Financial Evolution

As we look toward the middle of the 21st century, the narrative surrounding iron ore is shifting from simple extraction to sustainable value creation. The financial world is increasingly viewing iron ore through the lens of the “Circular Economy.”

The Shift Toward Sustainable Mineral Finance

Institutions are now prioritizing “Green Steel” initiatives. This involves using renewable energy to power the mining process and utilizing green hydrogen for smelting. From a money perspective, this means that capital is being reallocated toward projects that can prove a lower carbon footprint. Governments are also introducing “Carbon Border Adjustment Mechanisms” (CBAM), which act as a tax on high-carbon steel imports. This will further widen the price gap between low-quality and high-quality iron ore, rewarding investors who positioned themselves in high-grade assets early.

Long-term Outlook: Is Iron Ore a Safe Haven?

While iron ore will always be subject to the booms and busts of the construction cycle, its necessity is indisputable. There is no modern civilization without steel. As India and Southeast Asia begin their own massive urbanization phases—mirroring China’s growth in the early 2000s—the long-term demand for iron ore appears robust.

In conclusion, “the ore for iron” is much more than a geological curiosity. It is a sophisticated financial instrument, a geopolitical lever, and a foundational asset for any diversified portfolio. By understanding the grades of ore, the dominance of the supermajors, and the shifting tides of global demand and decarbonization, investors can navigate the complexities of this essential market to build long-term, “ironclad” financial security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.