The allure of a new credit card often comes with tempting offers, and among the most prominent is the “Introductory APR.” This seemingly straightforward term can significantly impact your financial well-being, especially when embarking on a journey to manage debt or finance a large purchase. Understanding the nuances of introductory APR is crucial for making informed decisions and avoiding potential financial pitfalls. This article will delve into the definition of introductory APR, explore its various forms, outline the benefits and drawbacks, and provide practical advice on how to leverage it effectively while mitigating risks.

Understanding the Fundamentals of Introductory APR

At its core, an introductory Annual Percentage Rate (APR) is a special, often low, interest rate offered by credit card issuers for a limited period at the beginning of a new account. This promotional rate is typically applied to purchases, balance transfers, or both. The primary goal of an introductory APR is to attract new customers by making it more appealing to open and use a credit card. It’s a marketing tool designed to incentivize spending and debt consolidation, offering a temporary reprieve from standard interest charges.

The Mechanics of APR

APR represents the annual cost of borrowing money, expressed as a percentage. It encompasses not only the interest rate but also certain fees associated with the credit. For introductory APRs, this rate is significantly lower than the standard APR that will apply once the introductory period concludes. The “annual” aspect of APR means that if you were to carry a balance for an entire year at that rate, that’s the percentage you would pay in interest. However, introductory APRs are time-sensitive, meaning the clock is ticking from the moment your account is opened.

Key Components of an Introductory APR Offer

When you encounter an introductory APR offer, it’s essential to dissect its components to fully grasp its implications. These often include:

- The Promotional Rate: This is the advertised low interest rate, which can be as low as 0%. It’s the main attraction of the offer.

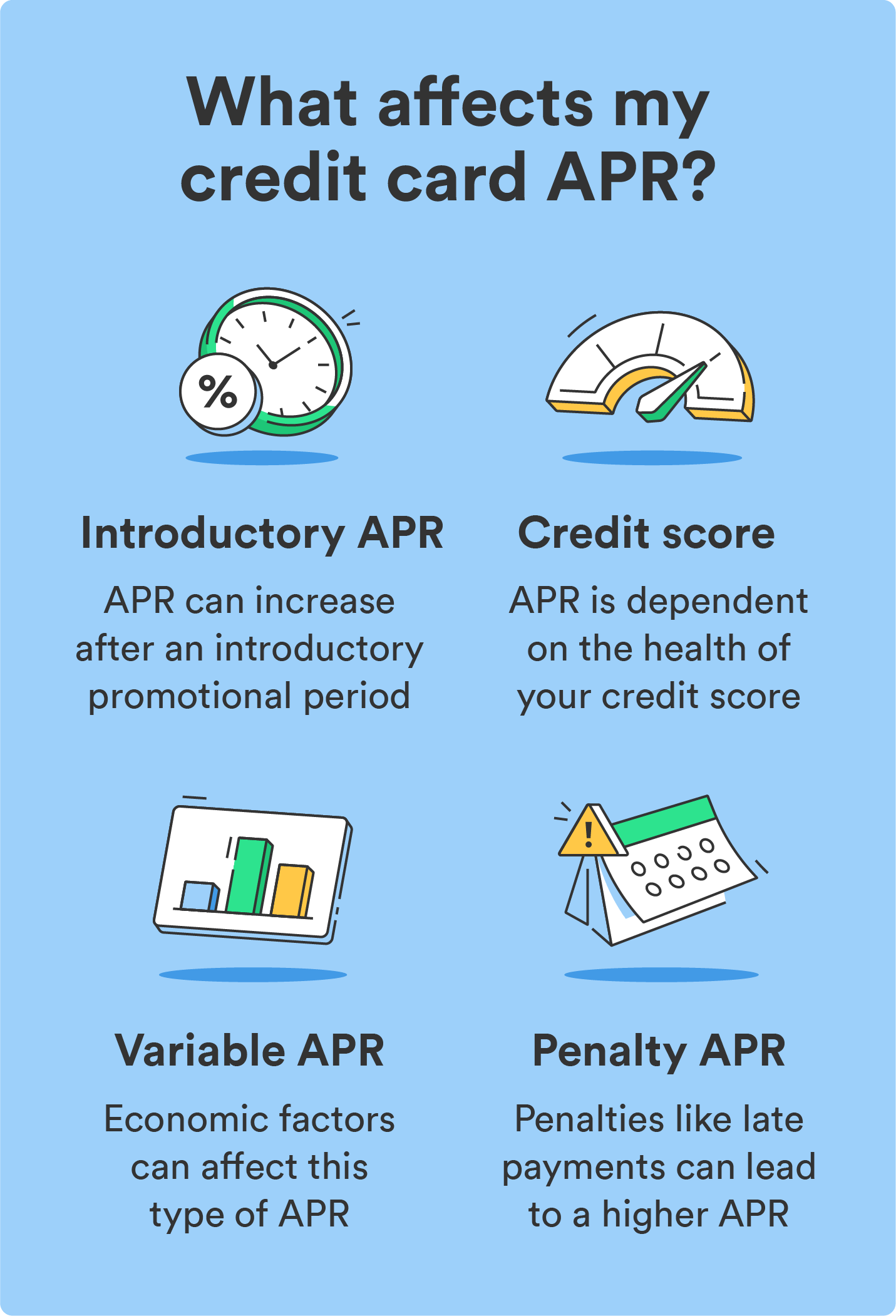

- The Introductory Period: This is the duration for which the promotional rate is valid. Introductory periods can vary widely, from a few months to 18 months or even longer.

- The Standard APR: This is the regular interest rate that will apply to your balance after the introductory period ends. It’s crucial to know this rate, as it will determine your ongoing borrowing costs. The standard APR is often much higher than the introductory rate.

- The Type of Transactions Covered: Introductory APRs can apply to different types of transactions. You might see offers for:

- Introductory Purchase APR: This applies to new purchases made with the card during the promotional period.

- Introductory Balance Transfer APR: This applies to balances transferred from other credit cards to the new card during the promotional period.

- Introductory Cash Advance APR: Less common for introductory offers and often starts at a high rate with no grace period. It’s generally advisable to avoid cash advances.

- The Grace Period: This is the period between the end of a billing cycle and the payment due date. If you pay your statement balance in full by the due date each month, you typically won’t be charged interest on new purchases. This grace period usually applies to the standard APR but might be waived for certain introductory offers, particularly on balance transfers.

Distinguishing Between 0% APR and Low Introductory APR

While often used interchangeably, a 0% introductory APR is a specific type of introductory APR that charges no interest whatsoever for a set period. This is the most attractive offer, as it allows you to finance purchases or pay down debt entirely without incurring interest charges during the promotional window. A “low” introductory APR, on the other hand, might be a rate significantly below the standard APR but still above 0%, such as 3.99% or 7.99%.

Strategic Applications of Introductory APR

The appeal of introductory APRs lies in their potential to save consumers significant money on interest. When used strategically, these offers can be powerful financial tools.

Financing Large Purchases

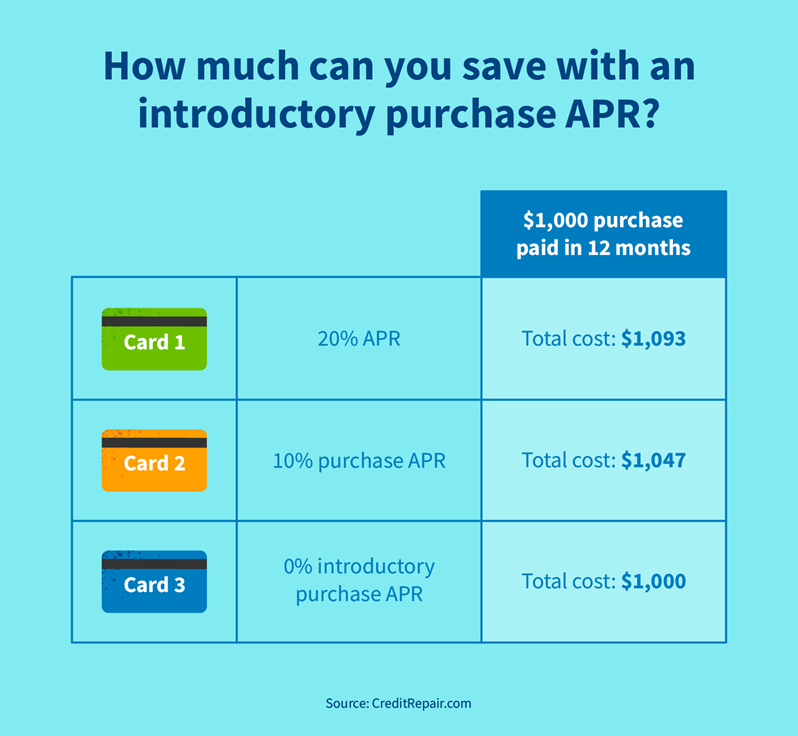

One of the most common and beneficial uses of an introductory APR is for financing large purchases. If you need to buy a major appliance, furniture, or even a vehicle (though auto loans have different structures), a card with a 0% introductory purchase APR can provide a period to pay off the cost without accumulating interest.

- Example Scenario: Imagine you need to purchase a new refrigerator for $1,500. By using a credit card with a 0% introductory purchase APR for 12 months, you can pay off the $1,500 over that year in 12 equal installments of $125 each, without paying a single cent in interest. If you had used a card with a standard APR of 18%, you would have paid a substantial amount in interest over that period.

Debt Consolidation and Management

Introductory balance transfer APRs are particularly valuable for consolidating high-interest debt from multiple credit cards into a single payment. This can simplify your financial life and, more importantly, allow you to aggressively pay down your principal balance without the constant burden of accumulating interest.

- The Balance Transfer Process: To take advantage of a balance transfer offer, you’ll typically apply for a new credit card with an introductory 0% balance transfer APR. You then initiate a balance transfer from your existing card(s) to the new card. It’s crucial to note that balance transfers often come with a fee, usually 3-5% of the transferred amount. This fee should be factored into your cost-benefit analysis.

- Maximizing Debt Repayment: The goal with a balance transfer is to pay off the transferred balance before the introductory period ends and the standard APR kicks in. Create a strict repayment plan and stick to it. Any balance remaining after the promotional period will start accruing interest at the standard APR, which could be quite high.

Credit Building

For individuals looking to establish or rebuild their credit history, responsibly using a credit card with an introductory APR can be a stepping stone. By making small purchases and paying them off in full and on time during the introductory period, you demonstrate responsible credit management to credit bureaus, which can positively impact your credit score.

Potential Pitfalls and How to Avoid Them

While introductory APRs offer significant benefits, they are not without their risks. A lack of understanding or discipline can lead to increased debt and higher costs than anticipated.

The Danger of the Standard APR Cliff

The most significant risk is failing to pay off your balance before the introductory period expires. Once the promotional rate ends, your remaining balance will be subject to the card’s standard APR, which can be considerably higher. This is often referred to as falling off the “APR cliff.”

- Consequences of Ignoring the Deadline: If you carry a balance after the introductory period, the interest charges can quickly snowball, negating any savings you initially achieved. For example, if you transferred $5,000 with a 0% intro APR for 12 months and still owe $3,000 when the 18% standard APR begins, you could end up paying hundreds of dollars in interest in the following months.

- Mitigation Strategy: Create a detailed repayment plan from the outset. Divide the total amount you intend to pay off by the number of months in the introductory period to determine your minimum monthly payment to clear the balance. Make sure this payment is achievable and set up automatic payments to avoid missing deadlines.

Balance Transfer Fees

As mentioned, balance transfers often come with a fee. While a 0% APR can save you a lot on interest, the balance transfer fee can add to the overall cost.

- Calculating the True Cost: Always factor in the balance transfer fee when comparing offers. For example, a 3% fee on a $10,000 balance transfer is $300. If the 0% APR period is 12 months, and you pay off the balance within that time, your effective interest rate for that period is 3% (spread over 12 months). If your current cards have interest rates significantly higher than 3%, it’s still a good deal. However, if the fees are high and the introductory period is short, it might not be as beneficial.

- Avoiding Unnecessary Fees: Some cards occasionally offer waived balance transfer fees as part of a promotion, which can further enhance the value of the offer.

Minimum Payments Trap

It’s tempting to make only the minimum payment, especially when dealing with a low or 0% introductory APR. However, making only minimum payments on a balance transfer with a 0% APR will mean you likely won’t pay off the entire balance before the standard APR takes effect. On a standard APR, minimum payments are notoriously insufficient for paying down debt quickly, and a large portion goes towards interest.

- Understanding Minimum Payment Calculations: Credit card companies calculate minimum payments as a small percentage of the outstanding balance (often 1-3%) or a fixed small amount, whichever is greater. This is designed to keep you in debt longer.

- Prioritizing Principal Payment: Always aim to pay significantly more than the minimum, especially during an introductory period, to ensure the principal is reduced.

Misusing the Card

A 0% introductory APR can be an invitation to overspend. If you treat the introductory period as free money and continue to rack up new purchases on the card, you could find yourself in a worse financial situation than before.

- Separating Introductory Offers: It’s often wise to use a 0% introductory APR card solely for the intended purpose (e.g., debt consolidation or a specific large purchase) and avoid using it for new everyday spending unless you are confident you can pay the entire statement balance in full each month.

- Keeping Track of Balances: Maintain clear records of your balances and payment deadlines for all your credit accounts.

Making the Most of Your Introductory APR Offer

To successfully leverage introductory APRs and reap their financial benefits, a disciplined and strategic approach is essential.

Research and Comparison Shopping

Not all introductory APR offers are created equal. Take the time to research and compare different credit card offers based on your specific financial needs and goals.

- Key Comparison Points:

- Introductory APR Rate: 0% is ideal, but low rates can still be beneficial.

- Introductory Period Length: Longer is generally better for repayment flexibility.

- Type of APR: Purchase APR, balance transfer APR, or both.

- Balance Transfer Fees: Compare percentages and any potential flat fees.

- Standard APR: Know what you’ll pay after the promotion ends.

- Credit Limit: Ensure the credit limit is sufficient for your needs.

- Other Card Benefits: Rewards programs, annual fees, etc.

Develop a Realistic Repayment Plan

Before you even apply for a card with an introductory APR, create a clear and actionable repayment plan.

- Calculate Your Monthly Payments: Determine how much you can realistically afford to pay each month towards the debt or purchase. Divide the total amount by the number of months in the introductory period to see if it’s achievable.

- Set Milestones: Break down your repayment goal into smaller, manageable milestones. This can help you stay motivated and track your progress.

Automate Your Payments

To ensure you never miss a payment and take full advantage of the introductory period, automate your payments.

- Automatic Minimum Payments: Set up automatic minimum payments as a safety net to avoid late fees and potential drops in your credit score.

- Automatic Larger Payments: If possible, set up automatic payments for the amount you’ve determined you need to pay each month to clear the balance within the introductory period. This requires careful monitoring of your bank account to ensure sufficient funds.

Monitor Your Credit Usage and Progress

Regularly check your credit card statements and your overall credit utilization.

- Stay Informed: Keep track of how much you owe, the remaining introductory period, and your progress towards paying down the balance.

- Avoid Overutilization: Even with a 0% APR, high credit utilization can negatively impact your credit score. Aim to keep your utilization below 30% of your available credit.

In conclusion, introductory APRs, particularly 0% offers, can be powerful tools for saving money on interest, financing large purchases, and managing debt. However, their effectiveness hinges on responsible usage and a clear understanding of the terms and conditions. By conducting thorough research, developing a robust repayment plan, and maintaining financial discipline, consumers can harness the advantages of introductory APRs to achieve their financial goals without falling into costly debt traps.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.