Navigating the world of personal finance often involves a keen understanding of how to best utilize financial tools, and credit cards are a cornerstone of modern spending. They offer convenience, rewards, and a means to build credit history. However, the pervasive utility of credit cards isn’t universal. Certain bills and services are intentionally excluded from credit card payment by providers, merchants, or even regulatory bodies. Understanding these limitations is crucial for effective budgeting, avoiding unnecessary fees, and ensuring timely payment of essential obligations. This article delves into the common types of bills you typically cannot pay with a credit card, the reasons behind these restrictions, and what alternatives are available.

Bills That Typically Prohibit Credit Card Payments

While credit card companies aim to facilitate as many transactions as possible, the nature of certain payments and the associated costs often lead to restrictions. These restrictions are not arbitrary; they are rooted in the financial models of both the service providers and the credit card networks.

Government and Tax Payments

One of the most common areas where credit card payments are restricted, or at least come with significant caveats, is with government entities. This includes federal, state, and local taxes, as well as certain court-ordered payments or fees.

Tax Payments

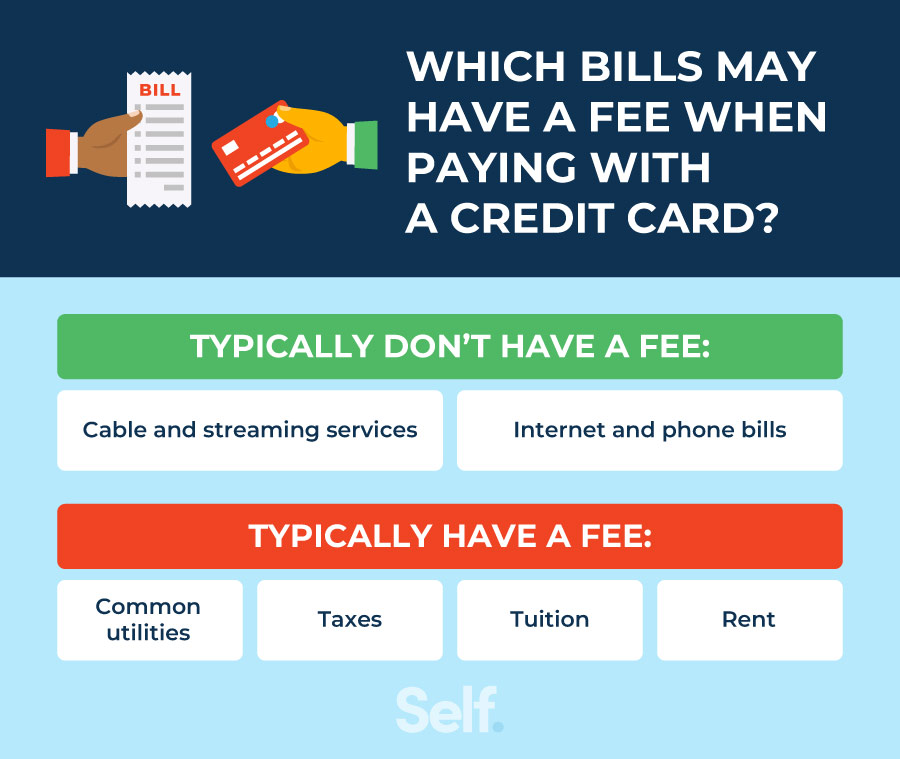

Paying taxes with a credit card can be a tempting proposition, especially for individuals or businesses facing a large tax liability and seeking to leverage rewards or defer payment. However, while the IRS and most state tax authorities do accept credit card payments, they almost invariably pass on a processing fee. This fee, often a percentage of the payment amount, can range from 1.5% to 3% or more. For example, a $10,000 tax bill could incur a $200-$300 processing fee, potentially negating any rewards earned. Furthermore, some jurisdictions may have direct prohibitions against paying certain types of taxes with a credit card without incurring these hefty surcharges. The rationale behind these fees is that credit card companies charge merchants (in this case, the government) transaction fees. To recoup these costs, governments impose these fees on the taxpayer choosing this payment method. In some instances, smaller local tax authorities or specific tax types might not accept credit cards at all, preferring traditional methods like checks or direct bank transfers to avoid the complexity and cost of credit card processing.

Court Fees, Fines, and Bail Bonds

Similarly, many court systems and bail bond agencies limit or prohibit direct credit card payments for certain services. Court fees, legal fines, and administrative charges are often processed through internal systems that may not be equipped to handle credit card transactions, or the profit margins are too thin to absorb the associated processing fees. For bail bonds, while some agencies might accept credit cards for the initial deposit or payment of their fee, the full bond amount often requires cash, cashier’s check, or collateral due to the high risk and complex legal processes involved. The inability to pay the full bond with a credit card is a significant restriction for many individuals in need of immediate release from custody.

Utility Bills and Services with Subscription Models

A vast array of recurring monthly bills, particularly those for essential services, often restrict direct credit card payments to avoid processing fees and to encourage direct debit from bank accounts.

Utility Providers (Electricity, Gas, Water)

Most major utility companies do not allow direct payment of your monthly bills using a credit card. The primary reason for this is the cost of merchant fees. For utility companies operating on relatively slim profit margins, absorbing these fees for millions of customers would significantly impact their bottom line. They prefer direct debit from checking accounts, which incurs minimal to no transaction costs. While some third-party payment processors might offer to pay your utility bill with a credit card for a fee, this is essentially a workaround that adds an extra layer of expense and isn’t a direct offering from the utility provider themselves. This restriction can be frustrating for customers who wish to earn rewards on all their monthly expenses.

Rent and Mortgage Payments

Paying rent with a credit card is often not an option directly through landlords or property management companies. Similar to utility bills, landlords typically want to avoid credit card processing fees, which can be substantial on larger monthly payments. While some online rent payment platforms might allow credit card payments, they invariably charge a convenience fee to the tenant. This fee can be anywhere from 2.5% to over 3.5% of the rent amount, making it an expensive way to pay. For mortgage payments, direct credit card payments are virtually nonexistent. Mortgage servicers are highly regulated, and the infrastructure for accepting credit card payments for principal and interest is either not in place or prohibitively expensive to implement. They primarily rely on automated clearing house (ACH) payments or checks.

Loans and Other Financial Obligations

Paying off existing loans, including student loans, personal loans, and auto loans, directly with a credit card is generally not permitted by the lenders. Lenders are already receiving a return on their capital through interest payments, and they are not set up to absorb credit card processing fees for loan repayments. While balance transfer offers can be used to consolidate debt onto a new credit card, this is a one-time transfer and not a method for ongoing loan payments. Similarly, paying off other financial obligations like money orders or wire transfers directly with a credit card is also usually not possible.

Cash Advance and Gambling Transactions

Certain financial transactions are explicitly excluded or heavily penalized by credit card issuers due to their high risk or lack of consumer protection benefits.

Cash Advances

Taking out a cash advance from your credit card is a form of borrowing, but it’s distinct from a purchase. Credit card companies do not consider a cash advance a bill to be paid. Instead, it’s a direct withdrawal of cash from your credit line. You are essentially borrowing money that you will then repay. This transaction carries a separate, often higher, interest rate that starts accruing immediately from the day of the withdrawal, without any grace period. Furthermore, cash advance fees are typically charged upfront, usually a percentage of the amount advanced or a flat fee, whichever is greater. Therefore, while you are using your credit card’s limit, it’s not a bill payment in the traditional sense, and the process is designed differently to reflect its nature as a high-cost loan.

Gambling and Speculative Transactions

Credit card companies often place restrictions on transactions deemed high-risk or associated with speculative activities. This includes payments to online casinos, sports betting sites, and other forms of gambling. These transactions are often flagged by credit card networks as “cash equivalents” or are subject to specific merchant category codes that may be blocked or heavily scrutinized. The reasons for these restrictions include regulatory concerns, the high likelihood of chargebacks and fraud associated with these industries, and the potential for customers to get into severe financial distress quickly. While some smaller or offshore gambling sites might accept credit cards, major, reputable platforms often have their own payment gateways that might not directly accept credit cards, or they might be subject to interdiction by credit card networks.

Why These Restrictions Exist

The limitations on credit card payments are not arbitrary; they stem from a complex interplay of costs, risks, and business models. Understanding these underlying reasons can help consumers make more informed financial decisions.

Merchant Fees and Profit Margins

The core reason for many restrictions lies in merchant fees. When a business accepts a credit card payment, they pay a percentage of the transaction amount, plus a small fixed fee, to the credit card network and the issuing bank. These fees, often referred to as interchange fees and network fees, are how credit card companies make their money. For businesses operating on thin profit margins, such as utility companies or government agencies that provide essential services, these fees can be a significant operational cost. Absorbing these fees for every transaction would either drastically increase the price of their services for all customers or significantly erode their profits. Therefore, they opt for payment methods that are either free or have lower transaction costs, such as direct bank transfers (ACH) or checks.

Risk and Fraud Concerns

Certain types of transactions carry a higher risk of fraud or chargebacks, making them less attractive for credit card acceptance. Gambling transactions, for instance, are notorious for their association with fraud and chargeback disputes. Credit card companies are wary of facilitating these transactions directly to mitigate their exposure to financial losses. Similarly, large, one-off payments like property taxes or mortgage payments, while less inherently risky, can still be targets for fraudulent activity. By limiting credit card acceptance for these types of bills, financial institutions and service providers are also protecting themselves and their customers from potential fraud.

Regulatory and Legal Frameworks

In some cases, regulatory requirements or legal frameworks dictate how payments can be processed. For instance, specific government payments or court-ordered financial obligations might have established procedures that do not readily accommodate credit card processing. The complexity of integrating credit card payment systems with existing government or legal accounting systems can also be a deterrent. Furthermore, regulations around money laundering and the financial integrity of certain industries can lead to restrictions on payment methods.

Promoting Specific Payment Methods

Often, the restrictions are also a strategic choice to encourage the use of alternative payment methods that are more cost-effective for the provider. Direct debit from a bank account (ACH) is significantly cheaper for businesses than credit card processing. By not accepting credit cards for recurring bills like utilities or rent, providers incentivize customers to set up automatic bank transfers, which streamlines their cash flow and reduces their processing costs. This can lead to more predictable revenue streams and lower administrative burdens.

Alternative Payment Methods and Strategies

While direct credit card payments for certain bills are restricted, various alternative payment methods and strategies can help consumers manage their finances effectively and, in some cases, still leverage the benefits of credit cards indirectly.

Direct Debit and Bank Transfers

For recurring bills from utility companies, rent, mortgages, and loan payments, direct debit from your bank account is the most common and often preferred method. This ensures timely payments, avoids late fees, and is usually free of charge. Many providers offer online portals where you can set up automatic payments from your checking or savings account. Bank transfers, including ACH payments, are also widely accepted and are a secure way to move funds directly between accounts.

Checks and Money Orders

While increasingly less common in daily transactions, checks and money orders remain viable payment options for many bills. Government agencies, some landlords, and certain service providers may still prefer or only accept these traditional methods. Sending a check requires careful record-keeping, and money orders, purchased with cash or a debit card, offer a prepaid alternative for those who don’t want to use a bank account or credit card.

Third-Party Payment Processors

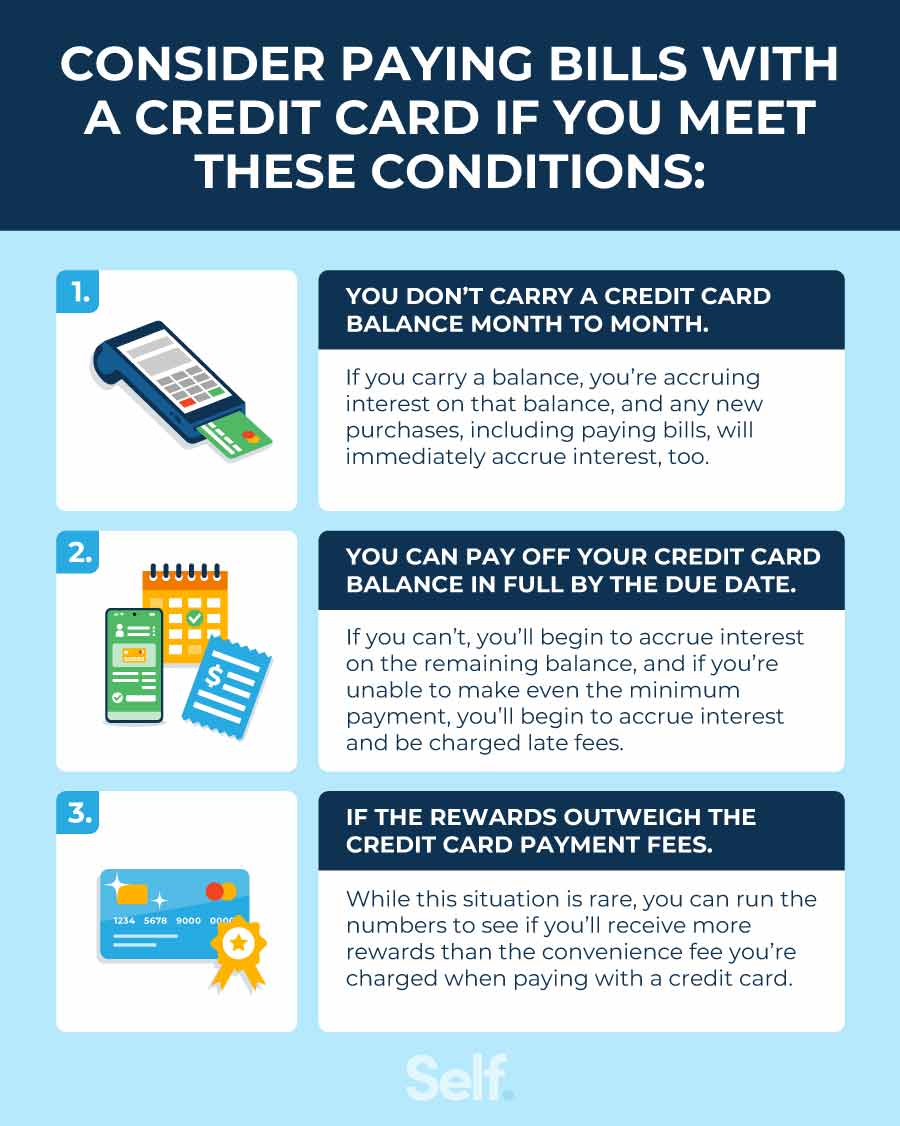

For certain bills that do not accept credit cards directly, third-party payment processors may offer a solution. Platforms like Plastiq, for example, allow you to pay a wide range of bills with a credit card. They then pay your bill on your behalf via check or ACH. However, these services come with a convenience fee, which is typically a percentage of the payment amount. While this fee can sometimes be offset by credit card rewards, it’s essential to calculate whether the rewards earned outweigh the processing fee. This method is best used strategically for bills where the reward yield is high enough or when a specific need arises, such as meeting a credit card spending bonus requirement.

Strategic Use of Credit Cards for Indirect Benefits

Even when direct payment isn’t an option, credit cards can still play a role in managing your finances.

Meeting Spending Thresholds for Bonuses

If you have a new credit card with a generous sign-up bonus that requires a certain spending amount within the first few months, you might strategically use a third-party payment processor to pay some of your non-credit-card-friendly bills. By paying rent, tuition, or other large expenses through a service that accepts credit cards, you can meet your spending requirements to unlock valuable rewards. Remember to factor in the processing fees to ensure the strategy is financially sound.

Managing Cash Flow

For individuals or businesses facing a temporary cash flow crunch, using a credit card through a third-party processor can provide a short-term financial buffer. It allows you to defer payment for a month or so, giving you time to gather the necessary funds. However, this should be a temporary solution, as carrying a balance on a credit card accrues interest, which can quickly become more expensive than the original bill.

Conclusion

While credit cards have revolutionized how we pay for goods and services, their utility is not without boundaries. Understanding which bills cannot be paid directly with a credit card is a fundamental aspect of sound financial management. Government taxes, utility bills, rent, mortgages, and certain financial obligations often fall into this category due to merchant fees, risk, and regulatory considerations. By being aware of these limitations and exploring alternative payment methods like direct debit, bank transfers, or strategically using third-party processors, consumers can ensure their bills are paid on time, avoid unnecessary fees, and continue to make informed financial decisions that align with their overall financial goals. The key lies in knowing the rules of the game and playing them to your advantage.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.