The onset of the COVID-19 pandemic in early 2020 triggered unprecedented societal and economic shifts. As the virus spread rapidly, governments at all levels grappled with how to best protect public health while simultaneously mitigating the fallout. Among the most drastic measures implemented were widespread shutdowns, affecting businesses, schools, and public gatherings. The question of which state was the first to initiate such a shutdown is not merely a matter of historical curiosity; it has profound implications for understanding the economic ripple effects, the initial financial responses, and the long-term fiscal strategies that emerged from this global crisis. This article delves into the financial implications of the initial COVID-19 shutdowns, exploring the economic rationale, the immediate financial impacts, and the subsequent policy interventions in the state that first took decisive action.

The Economic Calculus of an Unforeseen Crisis

The decision to implement a state-wide shutdown was, and remains, a complex equation balancing public health imperatives with severe economic consequences. In the nascent stages of the pandemic, scientific understanding of the virus was still evolving, and the projected trajectory of its spread instilled a sense of urgency. This urgency, however, was directly at odds with the fundamental principles of a market-driven economy. Businesses, from small local shops to large corporations, rely on the free flow of commerce, consumer spending, and operational continuity. Imposing a halt to these activities, even for a limited period, represented a significant disruption with immediate and cascading financial repercussions.

Pre-Pandemic Economic Vulnerabilities and Their Amplification

Before COVID-19, the United States, like many developed nations, had a complex economic landscape characterized by varying levels of business resilience, consumer debt, and industry-specific dependencies. Sectors heavily reliant on in-person interaction, such as hospitality, retail, and entertainment, were inherently more vulnerable to the prospect of widespread public confinement. The financial structures supporting these industries, including supply chains, employment models, and capital investment, were ill-equipped to absorb an abrupt cessation of activity. The anticipation of a shutdown, therefore, illuminated pre-existing economic fragilities, transforming them into immediate financial threats.

The Rationale Behind the Shutdown: A Financial Risk Assessment

From a financial perspective, the decision to shut down was a calculated, albeit incredibly difficult, risk assessment. The potential economic costs of a widespread outbreak, including healthcare expenditures, loss of productivity due to illness, and potential long-term economic stagnation from a severely compromised workforce, were weighed against the immediate and certain economic devastation of a shutdown. The prevailing economic theory in such extreme situations often leans towards a proactive, albeit painful, intervention to prevent a far more catastrophic and prolonged economic collapse. The initial shutdown can be viewed as a financial triage, an attempt to contain a runaway expenditure (uncontrolled pandemic spread and its associated costs) by incurring a controlled, albeit substantial, immediate cost (economic shutdown).

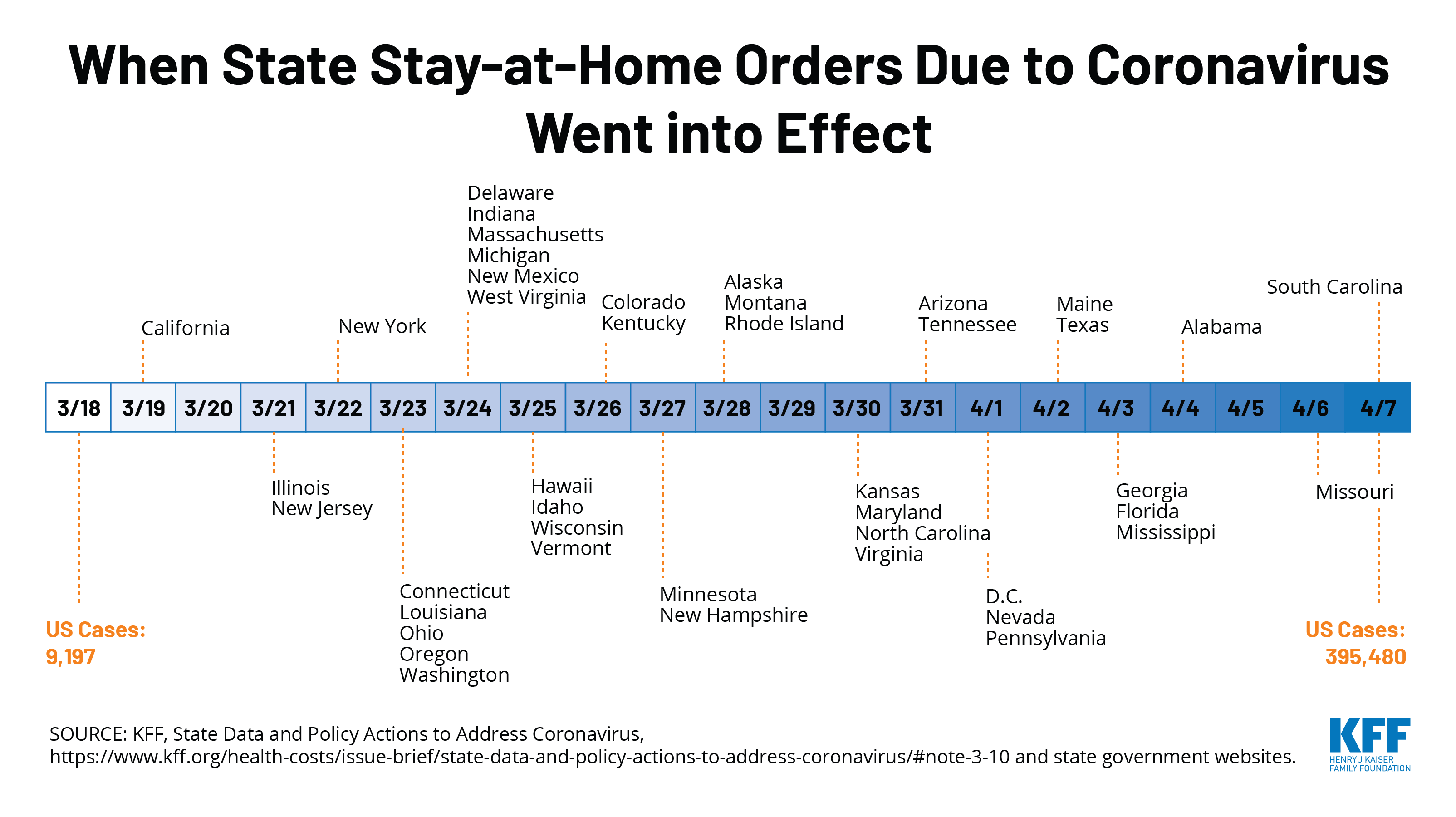

California: The First Domino to Fall and its Financial Ramifications

While the exact timeline of phased restrictions and their official designations can be debated, the state of California is widely recognized as the first to implement sweeping, stay-at-home orders across its entire population in response to the burgeoning COVID-19 crisis. Governor Gavin Newsom’s executive order on March 19, 2020, marked a pivotal moment, initiating a cascade of economic disruptions that would reverberate across the nation and the globe. The financial implications of this decision were immediate and profound, impacting individuals, businesses, and the state’s fiscal outlook.

Immediate Economic Shockwaves: Business Closures and Employment Losses

The directive for California residents to stay home and for non-essential businesses to close their doors sent immediate shockwaves through the state’s economy. The hospitality sector, a significant contributor to California’s GDP, was among the hardest hit. Restaurants, hotels, and entertainment venues faced an abrupt halt in revenue. This led to widespread business closures, with many small and medium-sized enterprises (SMEs) lacking the financial reserves to weather an extended period of zero income. The unemployment rate in California, like elsewhere, surged dramatically as businesses were forced to lay off workers. The financial strain on individuals was immense, with many facing immediate income loss and uncertainty about their financial future. The state’s robust tech sector, while more amenable to remote work, also experienced disruptions in supply chains and reduced investment as economic uncertainty permeated the market.

The State’s Financial Response: Emergency Funding and Fiscal Strain

The California state government, faced with an unprecedented economic crisis, was compelled to implement a swift and substantial financial response. This included allocating emergency funding for healthcare services, supporting overwhelmed hospitals, and establishing programs to assist individuals and businesses impacted by the shutdowns. The state’s unemployment insurance system, designed for more typical economic downturns, was quickly strained to its limits by the surge in claims. The financial burden on the state government was significant, requiring the reallocation of existing funds and the exploration of new borrowing mechanisms. The initial shutdown, therefore, not only triggered private sector financial distress but also placed considerable strain on public finances, necessitating proactive fiscal management and long-term financial planning.

Navigating the Financial Fallout: Policy Interventions and Economic Recovery Strategies

The initial shutdown in California, and subsequent similar actions by other states, necessitated a comprehensive and multi-faceted approach to financial recovery. This involved a combination of federal and state-level interventions aimed at stabilizing the economy, providing relief to those most affected, and laying the groundwork for a return to normalcy. The financial tools employed were varied, reflecting the complex and evolving nature of the crisis.

Stimulus Packages and Business Support Mechanisms

At the federal level, the U.S. government enacted several massive stimulus packages designed to inject liquidity into the economy and provide direct relief. These included programs like the Paycheck Protection Program (PPP), which offered forgivable loans to small businesses to help them retain employees, and expanded unemployment benefits for individuals who lost their jobs. California also implemented its own state-specific relief programs, targeting industries and populations that were disproportionately affected. The financial success of these interventions was a subject of ongoing debate, with some arguing they were crucial in preventing a complete economic collapse, while others pointed to issues of equitable distribution and potential inflationary effects. The underlying financial principle was to bridge the economic gap created by the shutdown, preventing a complete unraveling of the financial fabric.

The Long-Term Fiscal Health of the State: Debt, Deficits, and Diversification

The financial impact of the pandemic and the necessary relief measures extended far beyond the immediate crisis. California, like many states, faced increased debt burdens and potential future deficits as tax revenues declined due to economic slowdowns. This necessitated a re-evaluation of long-term fiscal health, including strategies for debt management, budget balancing, and economic diversification. The pandemic highlighted the vulnerability of economies heavily reliant on specific sectors, prompting discussions about building greater resilience through investment in new industries and innovative technologies. The financial lessons learned from the initial shutdown and the subsequent recovery period continue to shape fiscal policy and economic development strategies within the state.

Lessons Learned: Financial Preparedness for Future Shocks

The experience of California’s initial COVID-19 shutdown offered invaluable lessons in financial preparedness for future economic shocks. The rapid and severe disruption underscored the importance of robust financial safety nets, adaptable business models, and agile government fiscal policies. The pandemic exposed vulnerabilities in supply chains, the precarious financial situations of many workers, and the limitations of existing economic frameworks in responding to unprecedented global crises.

Building Financial Resilience: Individual and Corporate Strategies

On an individual level, the pandemic emphasized the critical need for emergency savings and diversified income streams. Many households that had built up personal financial cushions were better equipped to weather periods of unemployment or reduced income. For corporations, the crisis spurred a re-evaluation of supply chain diversification, remote work capabilities, and the importance of strong cash reserves. Businesses that had invested in digital transformation and flexible operational models were more adept at adapting to the new economic landscape. The financial principle here is proactive risk mitigation and building inherent resilience.

Government Financial Preparedness: Fiscal Reserves and Adaptive Policy Frameworks

For state governments, the pandemic highlighted the need for substantial fiscal reserves and the development of adaptive policy frameworks that can be quickly deployed during emergencies. The ability to rapidly disburse funds, manage unemployment claims efficiently, and support critical industries requires pre-existing infrastructure and well-defined protocols. Furthermore, the long-term financial health of states is intrinsically linked to their ability to foster economic environments that are both dynamic and resilient to external shocks. The initial shutdown served as a stark reminder that economic prosperity is not a given but requires continuous investment in infrastructure, innovation, and robust financial planning at all levels of governance. The financial architecture of a state must be designed not just for growth, but for survival and recovery.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.