Invoice discounting is a crucial financial tool for businesses, particularly small and medium-sized enterprises (SMEs), that need to accelerate their cash flow by unlocking the value tied up in their outstanding invoices. It’s a form of invoice finance that allows businesses to receive a significant portion of the invoice value upfront, rather than waiting for their customers to pay according to their agreed credit terms, which can often be 30, 60, or even 90 days. This immediate injection of capital can be transformative, enabling businesses to manage operational expenses, invest in growth, and navigate periods of fluctuating income.

The core principle behind invoice discounting is relatively straightforward. When a business issues an invoice to a customer for goods or services rendered, instead of waiting for the customer to pay, the business can “sell” that invoice, or a selection of them, to a third-party finance provider, known as a discounter. The discounter then advances a percentage of the invoice’s face value to the business, typically between 80% and 95%. Once the customer pays the invoice in full, the discounter collects the payment directly. The business then receives the remaining balance of the invoice, minus the discounter’s fees and interest.

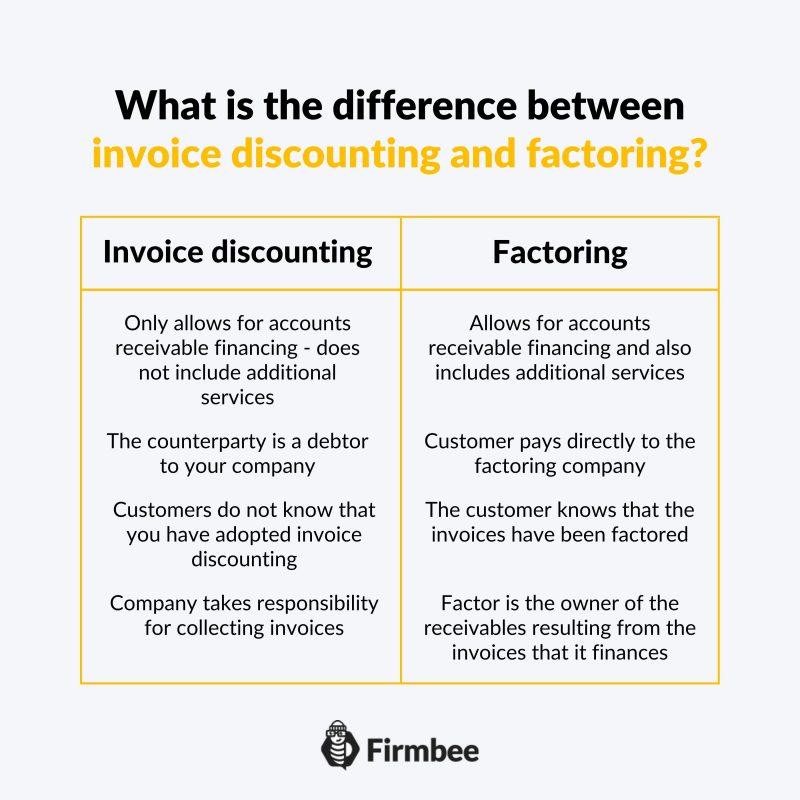

Crucially, in invoice discounting, the business typically remains responsible for managing its sales ledger and collecting payments from its customers. This is a key differentiator from factoring, another common form of invoice finance where the finance provider takes over the sales ledger management and credit control. This means that the customer is generally unaware that invoice discounting is being used, as the transaction and communication remain between the business and its client. This discreet nature makes invoice discounting particularly appealing to businesses that want to maintain direct relationships with their customers and control their credit control processes.

Understanding the Mechanics of Invoice Discounting

Invoice discounting operates on a foundation of trust and a clear understanding of the financial transaction. It’s not a loan in the traditional sense; rather, it’s the leveraging of an existing asset – the outstanding invoice – to generate immediate liquidity. The process is designed to be efficient and relatively simple for the business, although it requires a clear understanding of the agreement with the finance provider.

The Role of the Invoice as Collateral

At its heart, an invoice represents a debt owed to the business. This debt is a valuable asset that can be converted into cash. When a business chooses to use invoice discounting, these invoices are essentially pledged as security for the funds advanced by the discounter. The discounter assesses the creditworthiness of the business’s customers and the quality of the invoices themselves. Robust businesses with reliable customers and clear invoicing procedures will find it easier to secure invoice discounting facilities. The invoices act as collateral, reducing the risk for the finance provider. If the customer were to default on payment, the discounter might have recourse to the business, though this depends on the specific terms of the agreement. However, the primary security is the outstanding debt itself.

The Advance and the Reserve

The process begins with the business issuing an invoice to its customer. Upon verification and agreement, the discounter will advance a percentage of the invoice value. This is known as the “advance rate,” and it’s typically between 80% and 95%. For example, if a business has a £10,000 invoice due in 60 days and secures invoice discounting with an 85% advance rate, they would receive £8,500 immediately.

The remaining 15%, which is £1,500 in this example, is held by the discounter in a “reserve” or “retention account.” This reserve serves as a buffer for the discounter. Once the customer pays the invoice in full to the discounter, the discounter will deduct their fees and interest charges. The net amount remaining in the reserve is then released to the business. This release is known as the “repayment” or “balance payment.”

Fees and Charges: The Cost of Liquidity

Like any financial service, invoice discounting comes with costs. These fees are what the discounter charges for providing the facility and for taking on the associated risks. Understanding these costs is crucial for accurately assessing the profitability of using invoice discounting. The primary charges include:

- Discount Fee: This is an interest charge calculated on the amount of funds advanced for the duration it is outstanding. It is typically calculated on a daily basis and is often expressed as a percentage per annum. The rate can vary depending on the economic climate, the discounter’s risk assessment, and the overall facility size.

- Service Fee or Management Fee: This is a fee charged for the administration and management of the invoice discounting facility. It can be a fixed monthly fee, a percentage of the total invoice value processed, or a combination of both. This fee covers the discounter’s operational costs, including system maintenance and administrative staff.

- Late Payment Fees: If customers pay invoices late, the discounter may charge additional fees to the business. These can be calculated based on the period of delay and the amount outstanding.

- Setup Fees: Some discounters may charge an initial setup fee to establish the invoice discounting facility. This is typically a one-off charge.

The total cost of invoice discounting will depend on the volume of invoices discounted, the advance rate, the duration for which funds are outstanding, and the specific fee structure of the finance provider. Businesses need to carefully compare offers from different discounters to ensure they are getting the most competitive rates.

Benefits of Invoice Discounting for Business Growth

The primary appeal of invoice discounting lies in its ability to address a common pain point for growing businesses: working capital limitations. By providing swift access to funds, it empowers businesses to operate more smoothly, seize opportunities, and achieve their strategic objectives.

Improved Cash Flow Management

The most immediate and significant benefit of invoice discounting is the dramatic improvement in cash flow. Instead of waiting for customers to pay, businesses can access up to 95% of their invoice value within days of issuing the invoice. This predictable and reliable inflow of cash allows businesses to:

- Meet Operational Expenses: Pay suppliers on time, cover payroll, rent, utilities, and other essential operating costs without the stress of uncertain incoming payments.

- Manage Seasonal Fluctuations: Businesses with seasonal sales cycles can use invoice discounting to bridge gaps during leaner periods, ensuring consistent operational capacity.

- Avoid Overdrafts and Expensive Debt: By accessing funds tied up in invoices, businesses can reduce their reliance on costly overdraft facilities or short-term loans that often come with high interest rates.

Accelerated Growth and Investment Opportunities

With improved cash flow comes the ability to invest in growth. Invoice discounting provides the financial agility needed to:

- Fulfill Larger Orders: Businesses can confidently accept larger orders from new or existing clients, even if their current cash reserves are stretched. The ability to fund the supply chain and operational costs associated with these orders becomes manageable.

- Invest in New Projects: Expansion plans, product development, marketing campaigns, or entering new markets often require upfront capital. Invoice discounting can provide the necessary funds without diluting ownership or taking on significant long-term debt.

- Take Advantage of Supplier Discounts: Many suppliers offer discounts for early payment. With the cash injection from invoice discounting, businesses can leverage these discounts, reducing their cost of goods and improving their profit margins.

- Strengthen Bargaining Power: Having readily available cash can give businesses more leverage in negotiations with both suppliers and customers.

Maintaining Customer Relationships and Control

A key advantage of invoice discounting over factoring is the discreet nature of the service. The business retains control over its sales ledger and customer communications.

- Confidentiality: Customers typically remain unaware that invoice discounting is being used. This preserves the business’s professional image and avoids any perception of financial distress. The business continues to manage its credit control and collection processes, ensuring a seamless experience for its clients.

- Brand Integrity: By handling collections directly, businesses can maintain their brand’s reputation and customer service standards. This is particularly important for businesses that pride themselves on strong client relationships.

- Flexibility: The business retains full autonomy over its invoicing and credit policies, allowing it to adapt its practices as needed without external interference.

Who Can Benefit from Invoice Discounting?

Invoice discounting is a versatile financial solution that can be tailored to the needs of a wide range of businesses. While it’s particularly beneficial for SMEs, larger enterprises can also leverage its advantages. The primary determinant for eligibility is the existence of a robust sales ledger with creditworthy customers.

Small and Medium-Sized Enterprises (SMEs)

SMEs are often the primary users of invoice discounting. They frequently experience cash flow challenges due to longer payment terms from larger clients, rapid growth, or seasonal demand. Invoice discounting provides them with a vital lifeline, enabling them to:

- Expand and Compete: SMEs can compete more effectively with larger corporations by having the financial muscle to take on bigger projects and invest in necessary resources.

- Survive Economic Downturns: A steady cash flow allows SMEs to weather economic storms, pay their staff and suppliers, and maintain operations when demand may be uncertain.

- Access Working Capital Without Diluting Ownership: Unlike equity financing, invoice discounting doesn’t involve selling shares, thus allowing founders and existing shareholders to retain full ownership of their business.

Growing Businesses

Businesses experiencing rapid growth often find themselves outstripping their available working capital. As sales increase, so does the volume of invoices, but the cash collected doesn’t always keep pace with the demand for immediate operational expenditure. Invoice discounting is ideal for such businesses as it scales with their sales. The more invoices they generate, the more funding they can access, creating a virtuous cycle of growth.

Businesses with Long Payment Cycles

Industries where customers typically have extended payment terms, such as construction, manufacturing, or government contracting, can significantly benefit. The extended waiting periods for payment can severely hamper cash flow. Invoice discounting bridges this gap, ensuring that the business has the funds to continue operations while awaiting payment.

Businesses Seeking Confidentiality

As previously mentioned, the discreet nature of invoice discounting makes it suitable for businesses that prioritize maintaining direct control over their customer relationships and credit control. This includes businesses in sectors where customer trust and direct interaction are paramount, such as professional services, consulting, and niche manufacturing.

Considerations and Potential Drawbacks

While invoice discounting offers substantial advantages, it’s essential for businesses to be aware of potential drawbacks and carefully consider the implications before adopting the service. A thorough understanding of the agreement and its implications will help mitigate any negative consequences.

Recourse vs. Non-Recourse

A crucial distinction in invoice discounting agreements is whether they are “with recourse” or “without recourse.”

- Invoice Discounting with Recourse: This is the most common type. If the customer fails to pay the invoice, the business is typically liable to repay the advanced funds to the discounter. This means the ultimate risk of non-payment still lies with the business. The discounter’s risk is reduced, and therefore the fees are often lower.

- Invoice Discounting Without Recourse: In this scenario, the discounter assumes the risk of bad debt. If the customer defaults due to insolvency or a dispute that isn’t the fault of the business, the discounter bears the loss. This type of facility is usually more expensive due to the increased risk for the finance provider and may require stricter eligibility criteria, often involving credit insurance.

Businesses must understand which type of recourse they have signed up for, as it significantly impacts their financial exposure.

Cost of the Facility

While invoice discounting can be cheaper than overdrafts or other forms of short-term debt, the fees can still accumulate, especially if invoices are outstanding for extended periods or if the facility is used frequently. Businesses need to conduct a thorough cost-benefit analysis. They should compare the cost of invoice discounting against the potential gains from improved cash flow, such as taking advantage of supplier discounts or avoiding missed growth opportunities. The overall cost should be factored into pricing strategies to ensure profitability.

Eligibility and Due Diligence

Not all businesses are eligible for invoice discounting. Discounters will typically assess the business’s financial health, its history, and the creditworthiness of its customers. They will want to see a track record of issuing invoices to sound businesses. The process usually involves a degree of due diligence, which can take some time. Businesses with a history of late payments, disputes with customers, or a concentration of invoices with a single, unproven customer may find it challenging to secure a facility.

Administrative Burden

Although the business retains control over its sales ledger, invoice discounting still requires some administrative effort. This includes accurate record-keeping, timely submission of invoices to the discounter, and keeping them informed about any payment issues or customer disputes. While usually less burdensome than factoring, it’s an additional process that needs to be integrated into the business’s operations.

In conclusion, invoice discounting is a powerful financial tool that offers a practical solution to cash flow challenges for businesses of all sizes. By unlocking the value of outstanding invoices, it provides immediate liquidity, fuels growth, and enhances operational resilience. However, like any financial instrument, it requires careful consideration of its mechanics, costs, and potential drawbacks. A thorough understanding and a clear agreement with a reputable finance provider will ensure that invoice discounting serves as a strategic asset, driving the business towards its financial and operational goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.