The allure of a seemingly great deal on a used car can be incredibly tempting, especially when the price tag appears significantly lower than comparable vehicles. However, beneath that attractive sticker price might lie a crucial designation that could impact your finances significantly: a rebuilt title. Understanding what a rebuilt title signifies is paramount for any savvy car buyer looking to make a sound financial decision. This isn’t just about a cosmetic repair; it’s about the vehicle’s history, its potential risks, and, most importantly, its long-term financial value.

The Genesis of a Rebuilt Title: Understanding Salvage and Restoration

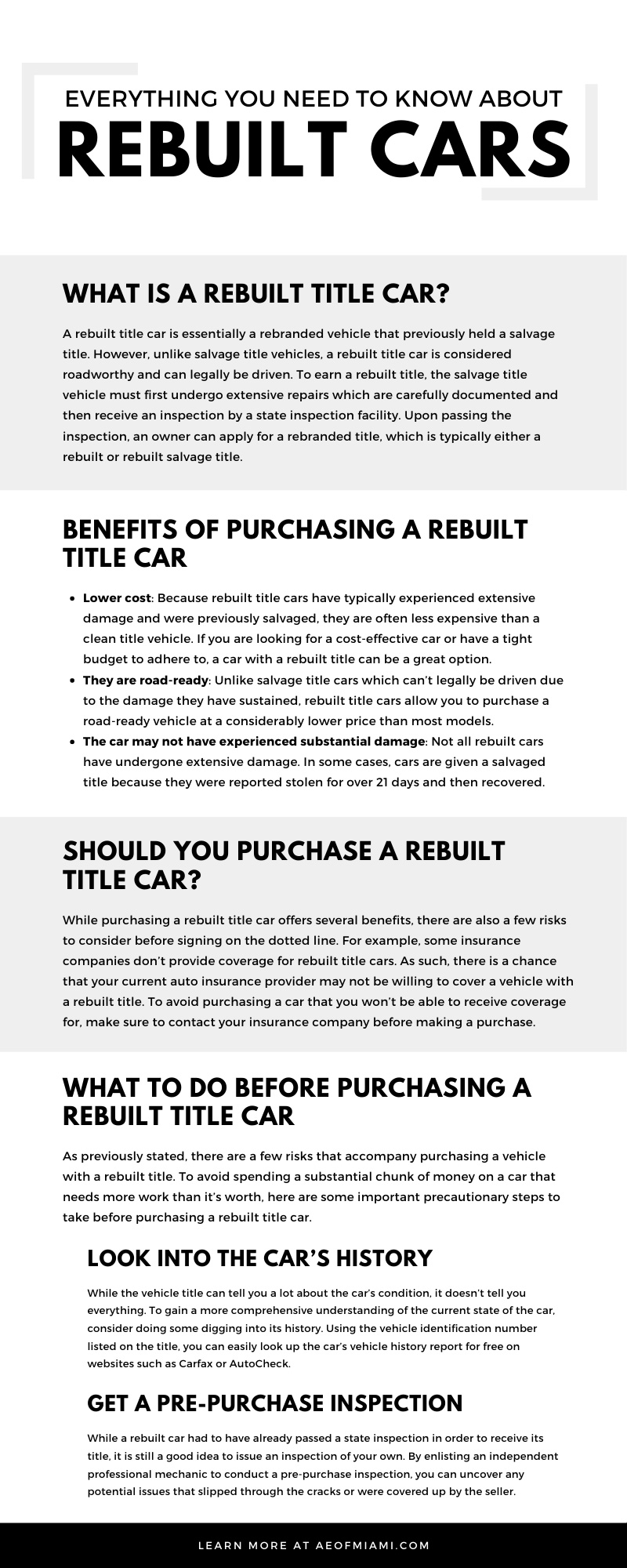

A rebuilt title isn’t a spontaneously generated status. It’s a consequence of a car being declared a total loss by an insurance company, typically due to significant damage, and then subsequently repaired to a roadworthy condition. This designation is a critical piece of financial information, signaling that the car has a history of substantial damage.

Defining “Total Loss” and the Insurance Payout

When a vehicle is involved in an accident, theft, or other event resulting in damage, an insurance adjuster assesses the cost of repairs against the car’s actual cash value (ACV). If the estimated repair costs exceed a certain percentage of the ACV, which varies by state but often falls between 70% and 90%, the insurance company declares the vehicle a “total loss.” At this point, the insurance company pays the owner the ACV of the vehicle and takes possession of the damaged car. This payout is a financial transaction that directly impacts the owner’s ability to replace their vehicle, and it’s the foundational event that sets the stage for a rebuilt title. For the insurer, it’s often more financially prudent to recoup some of their losses by selling the damaged vehicle as salvage rather than incurring the full cost of repairs.

From Salvage to Rebuilt: The Restoration Process and Inspection

Once a vehicle is declared a total loss and its title is branded as “salvage,” it cannot be legally driven on public roads. The salvage title signifies that the car is damaged and its structural integrity or safety may be compromised. However, this isn’t necessarily the end of the road for the vehicle. Entrepreneurs and repair shops can purchase these salvage vehicles, undertaking the necessary repairs to bring them back to a drivable and safe condition.

The crucial transition from a salvage title to a rebuilt title occurs after these extensive repairs are completed. Most states mandate a rigorous inspection process for vehicles with salvage titles. This inspection is conducted by a state-authorized agency and is designed to verify that all repairs have been completed safely and meet specific safety standards. This might involve checking the frame, suspension, braking system, electrical components, and other critical safety features. Once the vehicle passes this inspection, its title is officially changed from “salvage” to “rebuilt.” This designation signifies that while the car has a history of significant damage, it has been deemed roadworthy by the relevant authorities. However, it’s important to understand that this is a designation of functional repair, not a pristine restoration. The underlying structural integrity may still be a concern, and this is a primary factor impacting its financial value.

The Financial Ramifications of a Rebuilt Title

The most significant implications of a rebuilt title are financial, impacting everything from resale value to insurance premiums and loan eligibility. A car with a rebuilt title is inherently less valuable than a comparable vehicle with a clean title, and understanding these differences is crucial for making informed financial decisions.

Depreciated Resale Value: A Lingering Shadow

The most immediate and substantial financial consequence of a rebuilt title is the significant depreciation in resale value. Even if a car has been impeccably repaired and looks and drives like new, the stigma of its past damage often deters potential buyers and lowers its market worth. This depreciation can be substantial, often ranging from 20% to 50% or more compared to a similar vehicle with a clean title. This is a critical consideration for anyone planning to sell the vehicle in the future. When you purchase a car with a rebuilt title, you are essentially accepting this pre-determined loss in value. For those looking to flip cars or consider them as short-term investments, a rebuilt title is almost always a financially unsound choice. The market actively penalizes this type of history, and it’s a difficult hurdle to overcome when seeking to recoup your initial investment or make a profit.

Insurance Premiums: Higher Costs for Higher Risk

Insurance companies view vehicles with rebuilt titles as higher risks. This is due to the potential for underlying structural damage that may not be apparent during a standard inspection, leading to a greater likelihood of future mechanical issues or compromised safety in the event of another accident. Consequently, obtaining comprehensive and collision coverage for a car with a rebuilt title can be more challenging and significantly more expensive. Some insurers may refuse to offer full coverage altogether, opting for liability-only policies. Even when coverage is available, expect your premiums to be higher than for a comparable vehicle with a clean title. This added cost can accumulate over the life of the vehicle, further diminishing the initial savings that might have attracted you to the car in the first place. It’s a direct reflection of the perceived increased financial risk associated with these vehicles.

Loan and Financing Challenges: Accessing Capital

Securing financing for a car with a rebuilt title can also be a considerable hurdle. Many traditional lenders, including banks and credit unions, are hesitant to offer loans for vehicles with this designation. Their concern stems from the depreciated value and the perceived increased risk of default. If a lender does agree to finance a rebuilt title vehicle, they may require a larger down payment, offer less favorable interest rates, or have shorter loan terms. This can make the overall cost of ownership higher and the process of acquiring the vehicle more difficult. For buyers who rely on financing, this can be a deal-breaker, limiting their options and potentially pushing them towards vehicles they might not have initially considered. The financial institutions are assessing the long-term collateral value, and a rebuilt title significantly diminishes that perceived value.

Purchasing a Rebuilt Title Car: Due Diligence is Key

If you are considering purchasing a car with a rebuilt title, understanding the risks and performing thorough due diligence is not just recommended; it’s absolutely essential. The potential cost savings can be attractive, but they must be weighed against the inherent risks and long-term financial implications.

The Importance of a Pre-Purchase Inspection

Before even considering a purchase, always insist on a pre-purchase inspection (PPI) by an independent, trusted mechanic. This is especially critical for vehicles with rebuilt titles. Your mechanic should be experienced in inspecting vehicles with a history of damage and understand what to look for, such as frame alignment issues, substandard repair work, or hidden damage. This inspection can reveal potential problems that the state inspection might have missed or that have developed since the vehicle was deemed roadworthy. The cost of a PPI is a small investment compared to the potential cost of major repairs down the line. It’s a crucial step in assessing the true condition of the vehicle and understanding the potential future financial burden. This inspection is not about finding a few minor cosmetic flaws; it’s about identifying potentially dangerous or costly structural and mechanical issues.

Understanding the Vehicle’s History: Beyond the Title

While the rebuilt title itself is a significant indicator, it’s crucial to delve deeper into the vehicle’s history. Request any available repair records from the current owner or the shop that performed the restoration. If possible, obtain a vehicle history report from services like Carfax or AutoCheck. These reports can provide valuable information about the original damage, the extent of repairs, and any subsequent issues. Don’t solely rely on the information provided by the seller; conduct your own research to corroborate their claims and uncover any discrepancies. Understanding the specifics of the damage – was it a minor fender-bender or a severe collision? – can provide a clearer picture of the risks involved. This historical context is a vital component of your financial assessment.

Assessing the True Cost of Ownership: Beyond the Purchase Price

When evaluating a rebuilt title car, look beyond the sticker price and consider the total cost of ownership. Factor in potentially higher insurance premiums, the likelihood of more frequent and costly repairs, and the significantly lower resale value. Mentally (or even practically) adjust the purchase price by subtracting a realistic estimate of these future costs. This will give you a more accurate picture of whether the initial savings are truly worth the long-term financial commitment. For many buyers, the immediate savings on the purchase price are quickly eroded by these subsequent financial burdens, making the car a less financially sound decision than initially perceived. It’s a reminder that the cheapest option upfront isn’t always the most economical in the long run.

Rebuilt Title Vehicles: A Niche Market for Savvy Buyers

While generally not recommended for the average car buyer focused on long-term value and minimal risk, vehicles with rebuilt titles can represent a niche opportunity for specific buyers with the right knowledge and risk tolerance. The key lies in understanding the trade-offs and approaching the purchase with a highly informed perspective.

The Potential for Value: For the DIY Enthusiast or Restorer

For individuals with mechanical expertise, access to affordable repair parts, or a passion for automotive restoration, a rebuilt title vehicle can present an opportunity. If you can perform repairs yourself or have a trusted network of mechanics who can work at a reduced cost, the initial savings on the purchase price can be amplified. The goal for these buyers is often to invest further in the vehicle, bringing it up to a higher standard of repair and potentially mitigating some of the inherent depreciation. However, even in these scenarios, the underlying structural history remains a factor. The financial upside is contingent on the buyer’s ability to control repair costs and their willingness to accept the limitations on future resale value.

When a Clean Title Isn’t a Priority: Practical Considerations

In certain situations, a buyer might prioritize functionality and affordability over pristine history and maximum resale value. For example, a person who needs a reliable vehicle for a specific, limited purpose, such as a work vehicle for a small business that will be heavily utilized and eventually replaced, might consider a rebuilt title car. If the buyer intends to keep the vehicle for an extended period and doesn’t anticipate selling it, the depreciation factor becomes less of a concern. However, even in these cases, the risk of unexpected repairs remains. The financial decision hinges on the buyer’s specific needs, their risk appetite, and their realistic expectations about the vehicle’s lifespan and future performance. The financial prudence here is about matching the asset’s limitations to the buyer’s unique requirements.

Avoiding the Pitfalls: A Cautionary Note for All Buyers

Ultimately, for the vast majority of consumers, the financial risks associated with a rebuilt title vehicle outweigh the potential savings. The complexities of hidden damage, the increased insurance costs, the difficulty in financing, and the significant depreciation make them a less attractive proposition for most. Before making any decision, thoroughly weigh the financial implications. If you are not an experienced mechanic or restorer, and your primary goal is to acquire a reliable vehicle with good long-term value, it is generally advisable to steer clear of cars with rebuilt titles. Prioritizing a clean title, even if it means a higher initial purchase price, often proves to be the more financially sound and less stressful decision in the long run. The perceived bargain of a rebuilt title car can quickly turn into a financial burden if not approached with extreme caution and a deep understanding of its implications.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.