Navigating the landscape of retirement savings can feel like deciphering a complex financial code. Among the most common employer-sponsored plans, the 401(k) and 403(b) stand out as foundational pillars for building a secure financial future. While both serve the crucial purpose of helping individuals save and invest for retirement with significant tax advantages, they cater to different sectors of the workforce and come with their own unique nuances. Understanding these distinctions is not just academic; it’s essential for making informed decisions about your financial well-being, especially as you consider career paths or evaluate employee benefits.

For many, the terms 401(k) and 403(b) are often used interchangeably, leading to confusion about eligibility, investment options, and overall structure. This comprehensive guide aims to demystify these powerful retirement vehicles, providing clarity on their core characteristics, key differences, and critical similarities. We’ll delve into who offers them, how they work, and what factors you should consider when planning your retirement strategy. Furthermore, we’ll explore how modern technology can enhance your planning and how understanding these options contributes to your personal financial brand.

Understanding the Fundamentals: 401(k) vs. 403(b)

At their core, both the 401(k) and 403(b) are defined contribution plans, meaning you and/or your employer contribute money into an individual account, and the value of your retirement savings at withdrawal depends on the total contributions and the investment performance over time. Both offer substantial tax benefits, typically allowing your contributions to grow tax-deferred until retirement, or tax-free in the case of Roth options. However, their origins and the types of organizations that sponsor them are where their paths diverge.

The Private Sector’s Pillar: What is a 401(k)?

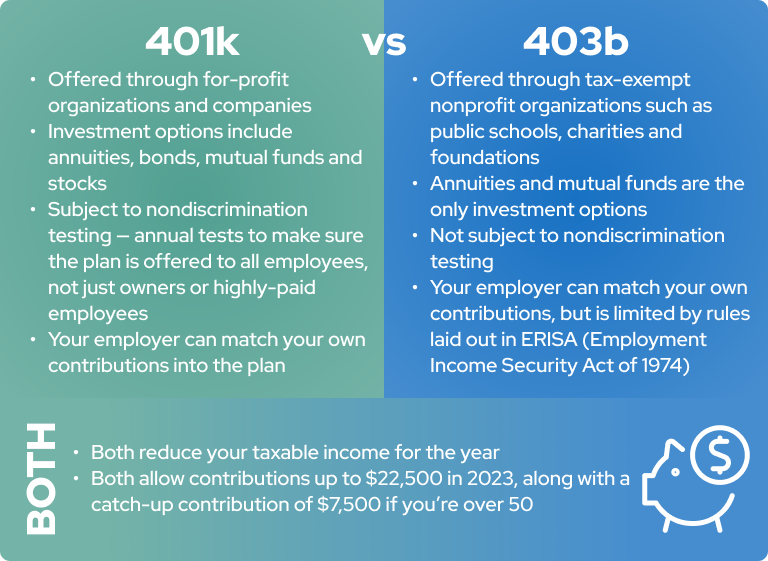

The 401(k) plan is the most widely recognized employer-sponsored retirement plan in the United States. It takes its name from a specific section of the Internal Revenue Code that authorized its creation in the late 1970s. Primarily offered by for-profit companies in the private sector, a 401(k) allows employees to contribute a portion of their pre-tax (or post-tax, with a Roth 401(k)) salary directly into an investment account.

Key characteristics of a 401(k) include:

- Eligibility: Generally available to employees of private sector companies.

- Employer Matching: A significant advantage of many 401(k) plans is the employer match, where the company contributes a certain amount to an employee’s account, often matching a percentage of the employee’s contribution up to a specific limit. This is essentially “free money” and is a powerful incentive to participate.

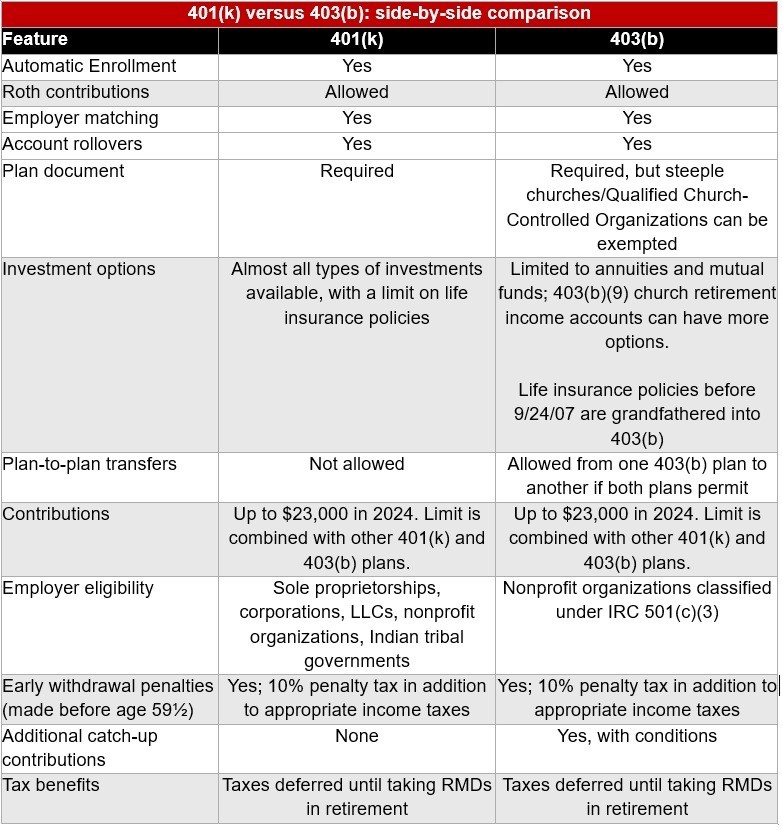

- Contribution Limits: The IRS sets annual limits on how much an individual can contribute. These limits are periodically adjusted for inflation and typically include “catch-up” contributions for those aged 50 and over.

- Investment Options: Typically offers a diverse range of investment choices, including mutual funds, exchange-traded funds (ETFs), and sometimes individual stocks or bonds. The specific options are curated by the plan administrator, usually an external financial institution.

- Vesting Schedule: Employer contributions often come with a vesting schedule, meaning you must work for the company for a certain period before you fully “own” the employer-matched funds. If you leave before being fully vested, you may forfeit a portion of those contributions.

- Loan Provisions: Many 401(k) plans allow participants to borrow from their account, with interest repaid to their own account. However, defaulting on a 401(k) loan can lead to significant tax penalties.

- Roth 401(k) Option: Many plans now offer a Roth 401(k) option, allowing after-tax contributions that grow tax-free and can be withdrawn tax-free in retirement, provided certain conditions are met.

The 401(k) is governed by the Employee Retirement Income Security Act (ERISA), which provides a robust framework of protections for plan participants, including disclosure requirements, fiduciary responsibilities for plan administrators, and detailed reporting standards. This regulatory oversight aims to ensure the security and proper management of retirement assets.

The Non-Profit’s Powerhouse: What is a 403(b)?

The 403(b) plan, often referred to as a “tax-sheltered annuity” (TSA) or “tax-deferred annuity,” shares many similarities with the 401(k) but is designed specifically for employees of non-profit organizations. This includes public schools, universities, hospitals, charitable organizations, and churches. Like the 401(k), it derives its name from the relevant section of the Internal Revenue Code.

Key characteristics of a 403(b) include:

- Eligibility: Exclusively available to employees of 501(c)(3) tax-exempt organizations and public educational institutions.

- Employer Matching: While less common than in 401(k)s, some non-profit employers do offer matching contributions, which are a significant benefit.

- Contribution Limits: Generally follows the same annual contribution limits as the 401(k), including catch-up contributions for those 50 and older. However, some 403(b) plans offer special “15-year rule” catch-up contributions for long-term employees, allowing them to contribute an additional amount if they have more than 15 years of service with the same employer and haven’t maximized contributions in previous years.

- Investment Options: Traditionally, 403(b) plans were primarily invested in annuity contracts, which are insurance products that provide a guaranteed income stream in retirement. While annuities are still common, many 403(b) plans now also offer a selection of mutual funds. The range of investment options can sometimes be more limited or feature higher fees compared to some 401(k) plans.

- Vesting Schedule: Similar to 401(k)s, employer contributions to 403(b)s may also be subject to vesting schedules.

- Loan Provisions: Like 401(k)s, 403(b) plans often allow participants to borrow against their account balance.

- Roth 403(b) Option: Many plans now offer a Roth 403(b) option, similar in principle to the Roth 401(k).

While 403(b) plans can fall under ERISA, many governmental and church plans are exempt, meaning they may not have the same level of regulatory oversight as ERISA-covered plans. This difference in regulation can impact fiduciary responsibilities and disclosure requirements, making it crucial for participants to understand their specific plan’s structure.

A Head-to-Head Comparison: Key Distinctions and Overlaps

While their shared goal is retirement savings, a deeper dive reveals critical differences between 401(k) and 403(b) plans that can influence your financial strategy. Understanding these distinctions, alongside their fundamental similarities, is key to maximizing your retirement readiness.

Employer Eligibility and Investment Landscape

The most fundamental difference lies in who offers these plans. A 401(k) is the domain of for-profit private sector companies, from small businesses to multinational corporations. In contrast, a 403(b) is exclusively for employees of non-profit entities, including public school systems, universities, hospitals, and charities. This distinction in employer type directly impacts the plan’s overall structure and the regulatory framework it operates under.

Regarding investment options, 401(k) plans typically offer a broad spectrum of mutual funds, index funds, and target-date funds, often curated by large investment firms. The competitive nature of the private sector can sometimes drive down administrative fees and expand investment choices within 401(k) plans. 403(b) plans, historically, have been more focused on annuity contracts, which offer guaranteed income but can sometimes come with higher fees and less investment flexibility. While many 403(b)s now include mutual funds, the selection might still be narrower or feature different fee structures compared to a typical 401(k). It’s crucial for 403(b) participants to scrutinize the fees associated with their investment choices, particularly with annuities.

The regulatory environment also varies. 401(k) plans are almost universally governed by ERISA, which mandates strict fiduciary duties for plan sponsors, ensuring they act in the best interests of plan participants. While many 403(b) plans are also ERISA-covered, some governmental and church 403(b)s are exempt. This exemption means they might not be subject to the same rigorous oversight regarding reporting, disclosure, and fiduciary standards, placing more responsibility on the participant to understand the plan’s details and associated risks.

Contribution Mechanics, Matching, and Tax Implications

When it comes to contribution limits, 401(k) and 403(b) plans generally follow the same annual IRS guidelines for employee contributions (and “catch-up” contributions for those 50 and over). However, 403(b) plans offer a unique “15-year rule” catch-up provision for long-serving employees of the same non-profit organization. This allows additional contributions above the standard limits, which can be a significant advantage for those nearing retirement in the non-profit sector.

Employer matching contributions are a key draw for both plans. While common in 401(k)s, where companies often match a percentage of employee contributions, they are less universally offered in 403(b) plans. Non-profits, often operating with tighter budgets, may not always have the capacity to offer generous matching contributions. When an employer match is available in either plan, it should be considered a priority to contribute at least enough to receive the full match, as it represents an immediate, risk-free return on your investment.

Tax implications are largely similar for traditional versions of both plans: contributions are made pre-tax, reducing your current taxable income, and earnings grow tax-deferred until withdrawal in retirement, at which point they are taxed as ordinary income. Both plans also commonly offer a Roth option, allowing after-tax contributions that grow tax-free and can be withdrawn tax-free in retirement, provided specific conditions (like being over age 59½ and having held the account for at least five years) are met. The choice between traditional (pre-tax) and Roth (after-tax) contributions hinges on your current income tax bracket versus your expected income tax bracket in retirement.

Similarities: Despite their differences, 401(k) and 403(b) plans share fundamental goals and features. Both aim to provide a tax-advantaged way to save for retirement, encouraging long-term investing. Both typically allow for pre-tax or Roth contributions, offer tax-deferred growth, and impose penalties for early withdrawals before age 59½ (with some exceptions like hardship withdrawals). Both also have provisions for loans, allowing participants to borrow against their vested balance, though this is generally not recommended unless absolutely necessary due to the potential for missed investment growth and tax implications if the loan isn’t repaid.

Beyond the Basics: Strategic Planning and Modern Tools

Understanding the structural differences between a 401(k) and a 403(b) is just the first step. To truly optimize your retirement savings, you need to engage in strategic planning, leverage available technology, and cultivate a robust financial identity.

Making the Right Choice for Your Retirement Goals

Ultimately, the “better” plan isn’t about the plan type itself, but about the specific features of the plan available to you and how well it aligns with your personal financial goals. For most individuals, the decision between a 401(k) and a 403(b) is often made for them based on their employer. However, if you have career choices between the private and non-profit sectors, these distinctions become more critical.

When evaluating any employer-sponsored plan, consider the following:

- Employer Match: This is paramount. Always contribute enough to get the full match.

- Investment Options: Assess the diversity, quality, and expense ratios of the available funds. Lower fees mean more of your money working for you.

- Vesting Schedule: Understand how long it takes to fully “own” employer contributions.

- Fees: Both administrative fees and investment management fees can erode returns over time. Ask for detailed fee disclosures.

- Roth Option: Determine if a Roth 401(k) or 403(b) is available and if it suits your current and projected future tax situation.

- Catch-Up Contributions: For those nearing retirement, special catch-up provisions can be significant.

- Loan Provisions: Understand the terms, but generally try to avoid borrowing from your retirement.

Remember, your employer-sponsored plan is often just one piece of your overall retirement strategy. Consider supplementing it with other accounts like an Individual Retirement Account (IRA) – either traditional or Roth – especially if your employer’s plan has limited options or high fees, or if you want more control over your investments. A qualified financial advisor can provide personalized guidance, helping you analyze your specific situation and tailor a comprehensive retirement plan.

Integrating Technology and Personal Branding into Your Financial Strategy

In today’s digital age, technology plays an increasingly vital role in personal finance, and retirement planning is no exception. Leveraging the right tech tools can significantly enhance your ability to monitor, manage, and optimize your retirement accounts:

- Financial Planning Apps: Tools like Mint, Personal Capital, or YNAB (You Need A Budget) can consolidate all your financial accounts, including your 401(k) or 403(b), into a single dashboard. This provides a holistic view of your net worth, spending habits, and investment performance, allowing for better tracking and adjustments.

- Robo-Advisors: Platforms like Betterment or Wealthfront offer automated, algorithm-driven investment management at lower fees than traditional financial advisors. They can help with portfolio diversification, rebalancing, and even tax-loss harvesting for accounts outside your employer plan, ensuring your investments stay aligned with your risk tolerance and goals.

- Online Brokerage Platforms: For those who prefer a more hands-on approach or want to open an IRA alongside their employer plan, platforms like Fidelity, Vanguard, or Schwab offer extensive tools, research, and educational resources to help you choose and manage your investments.

- Digital Security: With increased reliance on online financial management, robust digital security practices are paramount. Two-factor authentication, strong unique passwords, and being vigilant against phishing scams are crucial for protecting your retirement nest egg from cyber threats.

Beyond technology, consider the concept of personal branding in your financial life. Your financial decisions, your approach to saving, and your investment philosophy collectively contribute to your “financial brand.” A strong financial brand reflects prudence, foresight, and a disciplined approach to wealth accumulation. This isn’t about public perception, but about your internal commitment to financial health. It involves:

- Strategic Decision-Making: Choosing the right retirement plan, understanding its features, and actively managing your contributions are elements of strategic financial branding.

- Consistent Execution: Regularly contributing, rebalancing your portfolio, and reviewing your plan are consistent actions that build a strong financial foundation.

- Knowledge Acquisition: Continuously educating yourself about financial markets, tax laws, and investment strategies empowers you to make smarter decisions, further solidifying your knowledgeable financial brand.

- Seeking Expert Advice: Knowing when to consult a financial advisor or tax professional demonstrates a sophisticated approach to managing complex financial situations.

By integrating smart tech solutions and consciously building a strong financial brand, you move beyond simply participating in a retirement plan to actively orchestrating your financial future with confidence and control.

Conclusion: Charting Your Course to a Secure Retirement

The distinction between a 401(k) and a 403(b) is more than just a code difference; it reflects the diverse landscape of employment in the United States and the tailored financial solutions designed for each sector. While both serve as powerful vehicles for tax-advantaged retirement savings, their differing eligibility requirements, typical investment offerings, and regulatory environments necessitate a thorough understanding from participants.

Whether you’re employed by a private corporation with a 401(k) or a non-profit organization with a 403(b), the core principles remain the same: start saving early, contribute consistently, understand your plan’s features, and take advantage of any employer matching contributions. By actively engaging with your retirement plan, leveraging modern financial technology to monitor your progress, and cultivating a disciplined approach to your personal finances, you are not just saving for retirement—you are actively building a secure and prosperous future. The path to your golden years is a journey of informed choices, strategic planning, and consistent action, irrespective of the specific plan code on your financial statement.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.