Understanding how much interest you will earn on your capital is the cornerstone of effective financial planning. Whether you are tucking money away in a traditional savings account, exploring high-yield options, or venturing into the world of fixed-income securities, the math behind your earnings dictates how quickly you can achieve your financial goals. Interest is, in its simplest form, the price of money—either the cost of borrowing it or the reward for lending it to a financial institution.

In an era of fluctuating inflation and shifting central bank policies, calculating your potential returns is no longer a “set it and forget it” task. To truly answer the question, “How much interest will I earn?” one must look beyond the surface-level percentage and analyze compounding frequencies, tax implications, and the vehicle chosen for the investment.

Understanding the Fundamentals of Interest Calculation

To project your future wealth accurately, you must first distinguish between the two primary ways interest is calculated: simple and compound. While they may sound similar, the long-term difference in the “interest earned” column can be staggering.

Simple Interest vs. Compound Interest

Simple interest is calculated solely on the principal amount—the initial sum of money you deposit or invest. The formula is straightforward: Principal × Interest Rate × Time. If you invest $10,000 at a 5% simple interest rate for five years, you earn $500 every year, totaling $2,500.

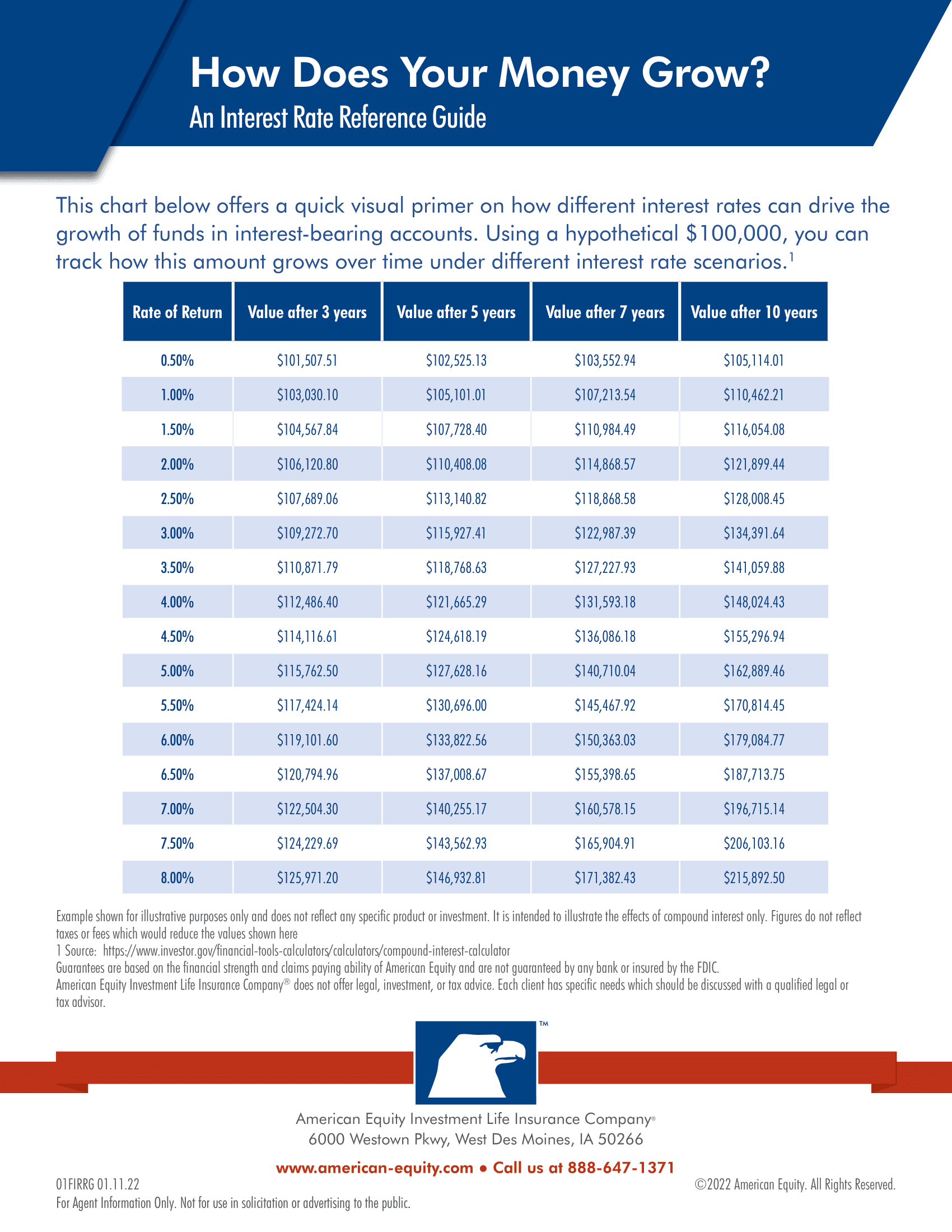

Compound interest, however, is what Albert Einstein famously called the “eighth wonder of the world.” It is calculated on the initial principal and also on the accumulated interest of previous periods. In the same $10,000 scenario at 5% interest, but compounded annually, you would earn interest on the $500 gained in year one during year two. By the end of five years, you would have earned approximately $2,762.82. The difference grows exponentially over longer horizons.

The Critical Role of the Annual Percentage Yield (APY)

When comparing financial products, you will often see two different rates: the Interest Rate and the Annual Percentage Yield (APY). While the interest rate tells you the base percentage, the APY reflects the real rate of return on your deposit after taking into account the effect of compounding interest.

If a bank offers a 5% interest rate compounded monthly, the APY will actually be 5.116%. When asking how much you will earn, always use the APY for your calculations, as it provides a standardized way to compare different financial products regardless of their compounding schedules.

Choosing the Right Vehicle for Interest Accumulation

The amount of interest you earn is heavily dependent on the “liquidity” of your money—how easily you can access it. Generally, the less access you have to your funds, the higher the interest rate the institution is willing to pay.

High-Yield Savings Accounts (HYSA)

For many, the first step in earning interest is moving money from a standard checking account to a High-Yield Savings Account. Traditional “brick-and-mortar” banks often offer interest rates as low as 0.01%, which effectively means you are losing purchasing power to inflation. Online-first banks, however, often offer HYSAs with rates 10 to 20 times higher than the national average. These accounts are ideal for emergency funds because they offer a competitive return while keeping your money liquid.

Certificates of Deposit (CDs)

If you do not need immediate access to your cash, a Certificate of Deposit (CD) might offer a higher rate than a standard savings account. When you open a CD, you agree to leave your money with the bank for a set term—ranging from a few months to several years. In exchange for this “time commitment,” the bank pays a fixed interest rate that is usually higher than a savings account. However, be cautious: withdrawing money before the term ends usually results in an “early withdrawal penalty,” which can eat into the very interest you were trying to earn.

Money Market Accounts (MMAs)

Money Market Accounts are a hybrid between savings and checking accounts. They typically offer higher interest rates than standard savings accounts and may come with check-writing privileges or a debit card. While they often require a higher minimum balance to avoid fees, they are an excellent tool for those who want to earn a respectable interest rate while maintaining a degree of transactional flexibility.

Factors That Influence Your Total Earnings

Beyond the interest rate itself, several external and structural factors will determine the actual “take-home” amount of interest you accumulate.

Compounding Frequency

The frequency with which interest is added to your account balance—daily, monthly, quarterly, or annually—impacts the total return. The more frequently interest is compounded, the faster your balance grows. For example, $100,000 at a 4% interest rate compounded annually yields $4,000 in one year. If that same amount is compounded daily, you would earn approximately $4,081. While $81 may seem negligible on a small scale, for large balances or long timeframes, the compounding frequency is a vital variable in the wealth-building equation.

Inflation and the “Real” Rate of Return

To understand how much you are truly earning, you must subtract the rate of inflation from your nominal interest rate. If your savings account is earning 4% interest, but the cost of goods and services (inflation) is rising at 3%, your “real” rate of return is only 1%. If inflation exceeds your interest rate, you are effectively losing “purchasing power,” even though your account balance is numerically increasing. This is why investors often look toward higher-yield, albeit higher-risk, assets during periods of high inflation.

The Impact of Taxes on Interest Income

In many jurisdictions, the interest you earn is considered taxable income. Unless the money is held in a tax-advantaged account (like a Roth IRA or a 401(k) in the United States), you must pay taxes on your earnings at your ordinary income tax rate. If you are in a 24% tax bracket and earn $1,000 in interest, you might only see $760 of that after Uncle Sam takes his cut. When projecting your future earnings, always factor in the “after-tax yield” to get a realistic picture of your financial growth.

Moving Beyond Savings: Fixed-Income and Market Interest

For those asking “how much interest will I earn” with an eye toward larger wealth accumulation, the conversation must shift from bank deposits to the broader fixed-income market.

Bonds and Treasury Securities

When you buy a bond, you are essentially acting as the bank. You lend money to a government or a corporation for a set period, and in return, they pay you interest in the form of “coupons.”

- Treasury Bills/Bonds: Backed by the government, these are considered the safest investments. The interest is often exempt from state and local taxes, making the effective yield higher than it might initially appear.

- Corporate Bonds: These typically offer higher interest rates than government bonds because they carry a higher risk of default.

Dividend-Yielding Stocks

While dividends are technically a distribution of a company’s profits and not “interest” in the traditional sense, they function similarly for the investor looking for regular income. “Dividend yields” allow you to calculate how much cash flow you will receive relative to the price of the stock. For a conservative investor, a portfolio of “Dividend Aristocrats”—companies that have increased their dividends for at least 25 consecutive years—can provide a predictable stream of income that often outpaces traditional bank interest.

Strategies and Tools for Projecting Your Interest

Calculating your earnings doesn’t have to be a guessing game. By using a few mathematical shortcuts and digital tools, you can map out your financial trajectory with precision.

The Rule of 72

The Rule of 72 is a quick, useful formula to estimate how long it will take to double your money at a given interest rate. Simply divide 72 by your interest rate. For example, if you are earning 6% interest, it will take approximately 12 years (72 ÷ 6 = 12) to double your initial investment. This rule is a great mental benchmark for comparing the long-term effectiveness of different interest-bearing accounts.

Utilizing Online Interest Calculators

For more complex scenarios involving monthly contributions, varying interest rates, and tax considerations, online compound interest calculators are indispensable. These tools allow you to visualize the “growth curve” of your investments. Seeing the visual representation of how a $500 monthly contribution can turn into hundreds of thousands of dollars over 20 years is often the motivation needed to remain disciplined with your savings.

Diversification of Interest Streams

To maximize the interest you earn while mitigating risk, consider a “laddering” strategy. This is commonly done with CDs or Bonds. By buying multiple CDs with different maturity dates (e.g., 1-year, 2-year, and 3-year), you ensure that a portion of your money becomes available at regular intervals. This allows you to reinvest at higher rates if interest rates rise, while still locking in better returns than a standard savings account for the bulk of your cash.

In conclusion, the amount of interest you will earn is a variable determined by your choice of financial vehicle, the frequency of compounding, and your ability to navigate taxes and inflation. By shifting your perspective from simple interest to compound growth and seeking out high-yield opportunities, you can turn your idle cash into a powerful engine for wealth creation. Finance is rarely about how much you make; it is about how much your money makes for you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.