The sight of a sea of red across financial tickers is an experience that evokes a visceral reaction in seasoned investors and novices alike. When the market “crashes”—typically defined as a sudden and double-digit percentage drop in stock indices over a few days—the immediate question on everyone’s lips is: Why?

Market crashes are rarely the result of a single, isolated event. Instead, they are usually the culmination of mounting pressures, shifts in sentiment, and structural vulnerabilities that finally reach a breaking point. To understand why the market crashes, one must look beyond the immediate headlines and examine the interplay between macroeconomic policy, investor psychology, and the technical mechanics of modern trading.

The Catalyst: Identifying the Triggers of Market Volatility

Every market crash has a narrative spark. While the underlying tinder may have been drying for years, a specific catalyst usually sets the fire. Identifying these triggers is essential for understanding whether a downturn is a temporary correction or the start of a prolonged bear market.

Macroeconomic Shifts and Interest Rate Hikes

The most frequent driver of market instability is a change in central bank policy, particularly regarding interest rates. For the better part of a decade, the global economy has often operated in a “low-rate environment.” When central banks, such as the Federal Reserve, raise interest rates to combat inflation, the “cost of money” increases.

Higher rates make borrowing more expensive for corporations, which can eat into profit margins and slow down expansion. Perhaps more importantly, higher rates increase the “discount rate” used by analysts to value future earnings. When the discount rate rises, the present value of stocks—especially high-growth tech stocks—drops significantly. If the market perceives that the Fed is moving too aggressively, a sell-off often ensues as investors pivot from “risk-on” assets to safer fixed-income securities.

Geopolitical Instability and Global Supply Chains

Markets thrive on predictability. Geopolitical conflicts, trade wars, or sudden shifts in international relations introduce a variable that algorithmic models struggle to price accurately. For instance, a conflict in a region responsible for a large portion of the world’s energy or semiconductor supply can send shockwaves through the market. This creates a “supply-side shock,” driving up costs for businesses and decreasing consumer purchasing power. When investors cannot calculate the future risks associated with these global disruptions, they often choose to exit their positions and move to cash, triggering a downward spiral.

Speculative Bubbles and Overvaluation

Sometimes, the market crashes simply because it became too expensive. During periods of “irrational exuberance,” stock prices decouple from their fundamental earnings. Metrics such as the Price-to-Earnings (P/E) ratio may reach historic highs that are unsustainable in the long run. When a bubble forms—whether it is in dot-com stocks, housing, or speculative growth sectors—it only takes a small dip in confidence for the entire structure to collapse. As soon as the first wave of investors begins to take profits, the lack of fundamental support beneath the current prices causes the floor to fall out.

The Mechanics of a Sell-Off: How Liquidity and Psychology Drive Prices

Once a crash begins, the “why” often shifts from external economic factors to the internal mechanics of the financial system itself. A crash is frequently an exercise in momentum, where the act of selling generates more selling.

The Role of Algorithmic Trading and High-Frequency Execution

In the modern era, a significant portion of market volume is driven by algorithms. These “black box” systems are programmed to execute trades based on specific technical triggers. If a major index drops below a certain “support level,” thousands of automated systems may be triggered to sell simultaneously. This can create a “flash crash,” where prices plummet faster than human traders can react. These algorithms are designed to protect capital, but when they all move toward the exit at the same time, they evaporate the available liquidity, making price drops even more extreme.

Margin Calls and the Liquidity Spiral

Many institutional and individual investors trade on “margin”—essentially using borrowed money from brokers to increase their position size. When the value of their holdings drops below a certain threshold, brokers issue a “margin call,” requiring the investor to deposit more cash or sell their assets immediately.

If the investor cannot provide the cash, the broker forced-liquidates their positions. This forced selling happens regardless of whether the investor wants to sell or believes in the long-term value of the stock. In a crash, a wave of margin calls creates a “liquidity spiral”: forced selling leads to lower prices, which leads to more margin calls, which leads to even more forced selling.

Fear, Panic, and the Herding Effect

Despite the rise of AI in trading, human psychology remains the ultimate driver of market cycles. Behavioral finance teaches us that “loss aversion”—the pain of losing money—is twice as powerful as the joy of gaining it. When investors see their portfolios shrinking, the prehistoric “fight or flight” response kicks in. Fear leads to a “herding effect,” where individuals sell simply because everyone else is selling. This collective panic often pushes prices far below their actual intrinsic value, turning a rational correction into an irrational crash.

Historical Context: Learning from Past Financial Crises

To understand the current market behavior, one must look at the blueprints provided by history. While the names and industries change, the underlying patterns of market crashes remain remarkably consistent.

The 2008 Housing Bubble and Systemic Risk

The Great Recession of 2008 was a masterclass in “systemic risk.” It wasn’t just that housing prices fell; it was that the entire global banking system was interconnected through complex derivatives tied to those houses. When the underlying assets (subprime mortgages) failed, the “contagion” spread to every sector of the economy. This taught the financial world that a crash in one niche area can lead to a total market shutdown if the leverage is high enough and the connections are opaque.

The Dot-Com Burst: Lessons in Valuation

In the late 1990s, the “New Economy” promised that traditional valuation metrics no longer applied. Companies with no revenue and no path to profitability were valued in the billions based on “eyeballs” and “clicks.” When the realization set in that profits actually mattered, the NASDAQ plummeted. This crash serves as a perpetual reminder that regardless of how revolutionary a technology is, the market will eventually demand a return on investment.

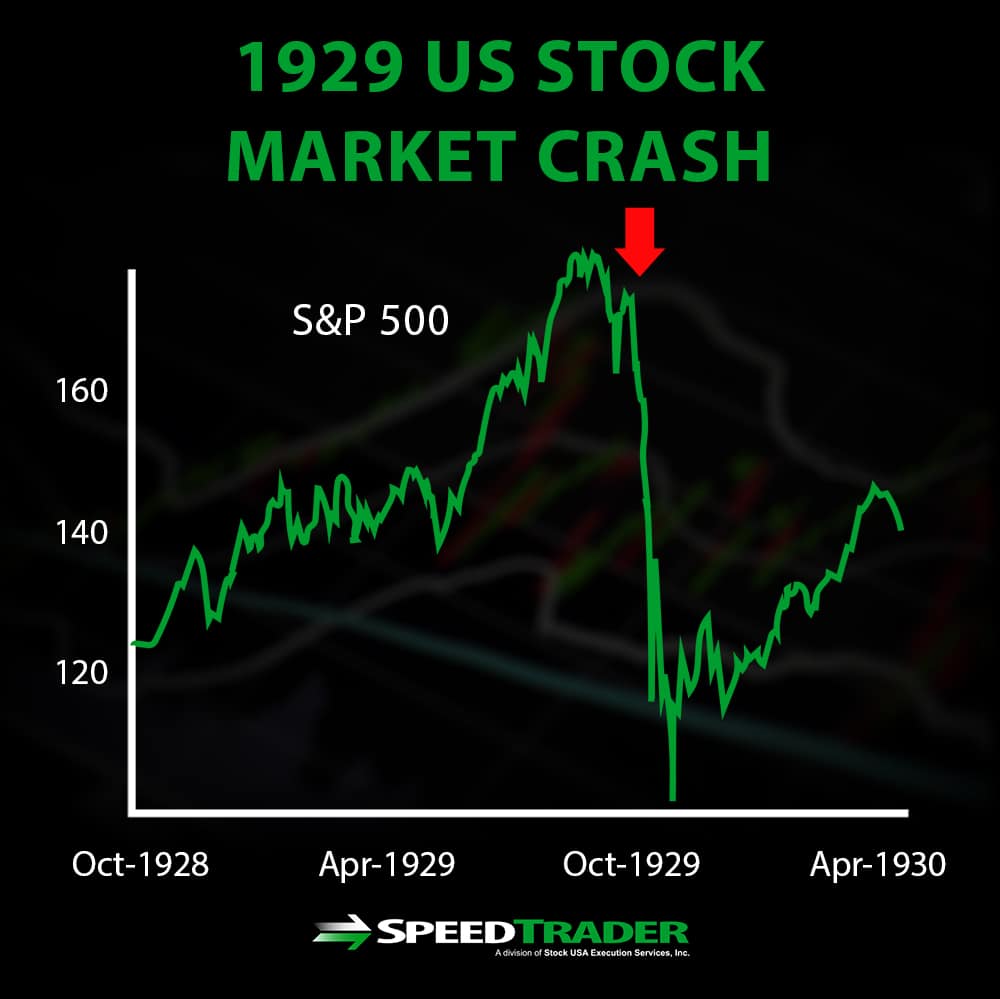

Black Monday and the Importance of Circuit Breakers

The 1987 “Black Monday” crash, where the Dow Jones fell over 22% in a single day, was a watershed moment for market structure. It highlighted how decoupled the market could become from reality due to early automated trading programs. In response, exchanges implemented “circuit breakers”—temporary halts in trading that allow investors to catch their breath and digest information during a rapid decline. These mechanisms are still in use today to prevent a total “meltdown” scenario.

Navigating the Aftermath: Strategies for Personal Finance and Recovery

For the individual investor, the “why” of a crash is often less important than the “what now?” Managing your money during and after a crash requires a blend of discipline, strategy, and emotional control.

Assessing Portfolio Diversification

A market crash is the ultimate stress test for your portfolio. It reveals exactly where you are over-leveraged or over-exposed. True diversification involves holding assets that do not move in lockstep with each other. If your “diversified” portfolio of 20 different tech stocks all dropped 30% at once, you weren’t actually diversified. The aftermath of a crash is the ideal time to rebalance into different asset classes—such as bonds, commodities, or international equities—to ensure that the next downturn doesn’t hit as hard.

The Psychology of “Staying the Course”

Historically, the worst mistake an investor can make during a crash is “panic-selling” at the bottom. Market recoveries are often as sudden and violent as the crashes themselves. Missing out on just the five best trading days in a decade can significantly reduce long-term returns. For those with a long-time horizon (10+ years), a market crash is often a “paper loss” that only becomes real if you hit the sell button. Maintaining an emergency fund outside of the market is the best way to ensure you aren’t forced to sell your investments at a loss to cover living expenses.

Identifying Value in a Bear Market

From a business finance perspective, a market crash is essentially a “sale” on the world’s greatest companies. While it feels counterintuitive to buy when prices are falling, this is how wealth is built. Professional investors look for “quality” during a crash—companies with strong balance sheets, low debt, and consistent cash flow that have been dragged down by the general market malaise. By shifting the perspective from “my net worth is shrinking” to “I am buying future cash flows at a discount,” an investor can navigate the emotional turbulence of a crash with a sense of purpose.

In conclusion, market crashes are a natural, albeit painful, part of the economic cycle. They serve to clear out excess, punish speculation, and reset the stage for the next period of growth. By understanding the triggers, the mechanics, and the historical precedents, you can move from a position of fear to one of informed resilience. The market will always have its “red days,” but for the disciplined investor, the crash is not the end of the story—it is merely a challenging chapter in a long-term journey toward financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.