The Stock Market Crash of 1929, often referred to as the “Great Crash,” remains the most devastating stock market collapse in the history of the United States. It was not a single-day event but a systemic dissolution of wealth that began in late October and signaled the beginning of the ten-year Great Depression. For modern investors and financial students, the 1929 crash serves as a foundational case study in market psychology, the dangers of excessive leverage, and the necessity of regulatory oversight. To understand the “how” and “why” of this financial catastrophe is to understand the very mechanics of modern global finance.

The Roaring Twenties: The Seeds of Financial Excess

Before the devastation of 1929, the United States experienced a decade of unprecedented economic expansion known as the “Roaring Twenties.” This was an era of profound technological advancement and cultural shifts, but beneath the surface of the jazz age, a precarious financial bubble was inflating.

Speculation and the Rise of Margin Trading

During the 1920s, the stock market became a national pastime. It was no longer reserved for the wealthy elite; ordinary citizens, from barbers to domestic workers, began pouring their savings into equities. This surge was fueled by a dangerous financial innovation: “buying on margin.” Investors could purchase stocks by paying only a small fraction of the price—sometimes as little as 10%—and borrowing the rest from brokers. This meant that for every $100 an investor put in, they were controlling $1,000 worth of stock. While this amplified gains during the bull market, it created a structural fragility where even a minor dip in prices could trigger a catastrophic wave of forced liquidations.

The Industrial Boom and Overproduction

The decade saw the mass production of automobiles, radios, and household appliances. While this drove corporate profits initially, by the late 1920s, production began to outpace consumer demand. Wages had not risen fast enough to allow the working class to continue purchasing these goods at the same rate. This led to an accumulation of unsold inventory and a slowdown in industrial production—a fundamental economic warning sign that the soaring stock market chose to ignore throughout 1928 and early 1929.

The Timeline of the Crash: From Black Thursday to Black Tuesday

The crash was characterized by a series of sharp drops punctuated by brief, desperate attempts by the financial establishment to stabilize the market. The volatility of October 1929 destroyed the illusion of permanent prosperity.

October 24, 1929: The First Tremor (Black Thursday)

The first sign of true panic occurred on Thursday, October 24. As the market opened, prices plummeted, and the volume of trading reached a record 12.9 million shares. In a bid to stop the bleeding, a group of powerful bankers, led by Richard Whitney (Vice President of the New York Stock Exchange) and backed by JP Morgan, began buying large blocks of “blue chip” stocks like U.S. Steel at prices above the current market. This temporary show of confidence succeeded in steadying the market for the weekend, but the underlying panic remained.

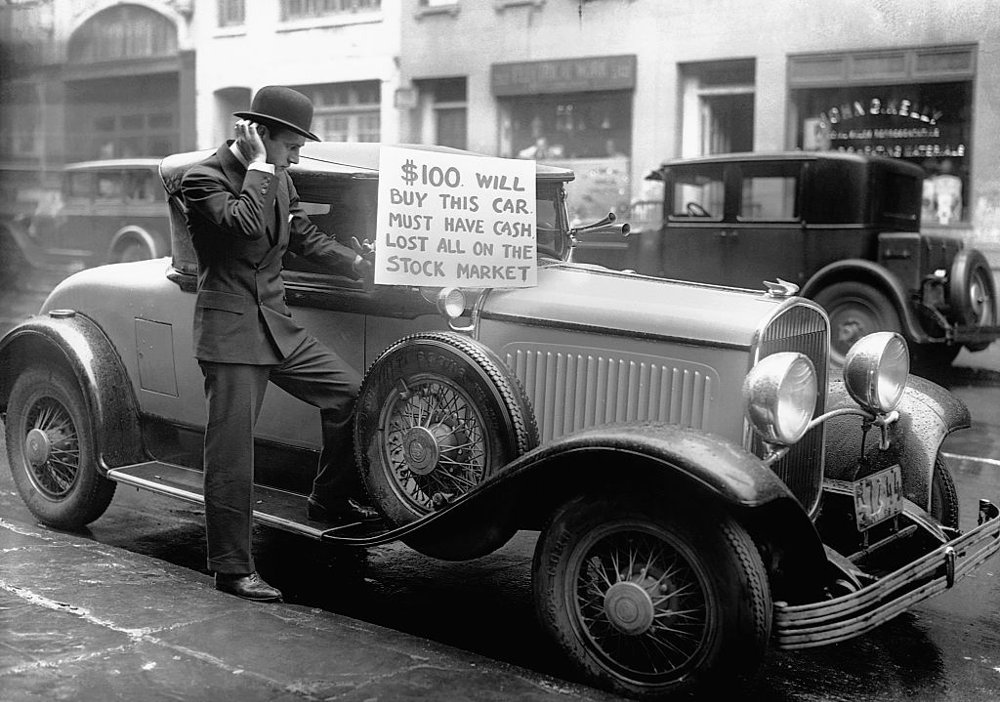

October 29, 1929: The Day the Bottom Fell Out (Black Tuesday)

The following Monday saw further declines, leading into the infamous Black Tuesday. On October 29, the market collapsed completely. Panic-stricken investors rushed to sell their shares at any price, but for many stocks, there were simply no buyers. Over 16 million shares were traded—a record that would not be broken for nearly 40 years. By the end of the day, billions of dollars in wealth had evaporated. Ticker tape machines, unable to keep up with the volume of trades, ran hours late, leaving investors in a terrifying information vacuum as their fortunes vanished.

The Economic Fallout: From Wall Street to Main Street

While the stock market crash was a financial event, its repercussions quickly bled into the “real” economy, affecting millions who had never owned a single share of stock. The transition from a market correction to a global depression was driven by several interlocking factors.

The Collapse of the Banking System

In 1929, there was no Federal Deposit Insurance Corporation (FDIC). When the stock market crashed, many banks that had heavily invested their depositors’ money in the market—or lent it to speculators—found themselves insolvent. News of bank failures led to “bank runs,” where panicked depositors lined up to withdraw their cash before the bank ran dry. Because banks only keep a fraction of their deposits in reserve, these runs led to the failure of thousands of institutions, wiping out the life savings of millions of families and freezing the credit markets necessary for business operations.

The Onset of the Great Depression

The loss of wealth led to a drastic reduction in consumer spending. Families who had lost their savings or feared for their jobs stopped buying cars, clothes, and appliances. In response, businesses cut production and laid off workers, which further reduced consumer demand in a vicious deflationary spiral. By 1933, the U.S. unemployment rate had reached a staggering 25%. This systemic failure highlighted the danger of a “wealth effect” in reverse, where a drop in asset prices leads to a total freezing of the productive economy.

Structural Causes and Systemic Failures

To prevent a repeat of 1929, modern economists have spent decades analyzing the structural failures that allowed the crash to occur. It was not merely bad luck; it was the result of a financial system operating without guardrails.

Lack of Financial Regulation

In 1929, the financial industry was largely self-regulated. There were no requirements for companies to provide transparent, audited financial statements to the public. Insider trading was common, and “stock pools” allowed wealthy investors to manipulate stock prices to their advantage before dumping shares on unsuspecting retail investors. The absence of a central regulatory body meant that the market was essentially a “Wild West,” where fraud and misinformation were rampant.

The Role of the Federal Reserve

The Federal Reserve, established in 1913, was still in its infancy during the crash. Many historians argue that the Fed’s policy in the late 1920s was a major contributor to the disaster. They initially kept interest rates low, which encouraged the speculative bubble. Then, as the crash began, they failed to act as a “lender of last resort,” allowing the money supply to contract by nearly one-third. This contraction made it impossible for the economy to recover, turning a sharp recession into a decade-long depression.

Timeless Lessons for Modern Investors

The legacy of 1929 is written into the very DNA of our current financial system. By examining the mistakes of the past, modern investors can better navigate the complexities of today’s markets.

The Importance of Diversification and Risk Management

One of the most painful lessons of 1929 was the danger of over-concentration. Many investors had their entire net worth tied up in a handful of speculative stocks. Today, the principle of diversification—spreading investments across different asset classes, industries, and geographies—is the cornerstone of personal finance. Furthermore, the crash illustrated the extreme risk of using “leverage” (borrowed money). While margin trading still exists today, it is strictly regulated to prevent the kind of chain-reaction liquidations seen in 1929.

Understanding Market Psychology and Bubbles

The 1929 crash proved that markets are not always rational. They are driven by human emotions: greed during the upswing and fear during the downswing. The “herd mentality” that drove prices to unsustainable levels in 1929 can still be seen in modern “meme stocks” or the dot-com bubble of the late 90s. Insightful investors use the history of 1929 to recognize when prices have become detached from fundamental value, allowing them to exercise caution when the rest of the market is in a state of euphoria.

The Evolution of Financial Safeguards

In the wake of the crash, the U.S. government implemented sweeping reforms that define the “Money” landscape today. The Securities and Exchange Commission (SEC) was created in 1934 to enforce federal securities laws and protect investors from fraud. The Glass-Steagall Act was passed to separate commercial banking from investment banking, ensuring that depositors’ money was not used for risky speculation. While some of these regulations have evolved or been repealed, the core philosophy remains: a healthy economy requires transparency, liquidity, and oversight to prevent the kind of systemic collapse that defined the year 1929.

By studying the Stock Market Crash of 1929, we do not just learn about a historical tragedy; we gain the tools to build more resilient financial futures. The “Great Crash” serves as a permanent reminder that while markets are engines of wealth, they must be fueled by reality and steered by discipline.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.