Securing a small business loan is often the most significant hurdle an entrepreneur faces. Whether you are looking to launch a startup, expand your current operations, or bridge a seasonal cash flow gap, access to capital is the fuel that powers the engine of commerce. However, the lending landscape has evolved dramatically over the last decade. Gone are the days when a simple handshake at a local bank sufficed. Today, getting a small business loan requires a strategic blend of financial literacy, meticulous preparation, and a deep understanding of the diverse lending products available in the “Money” sector.

Defining Your Financial Objectives and Exploring Loan Types

Before approaching a lender, you must have a crystalline understanding of why you need the money and how it will generate a return on investment. Lenders are risk-averse by nature; they want to ensure that the capital they provide will facilitate growth rather than simply delaying an inevitable decline.

Identifying the Purpose of the Loan

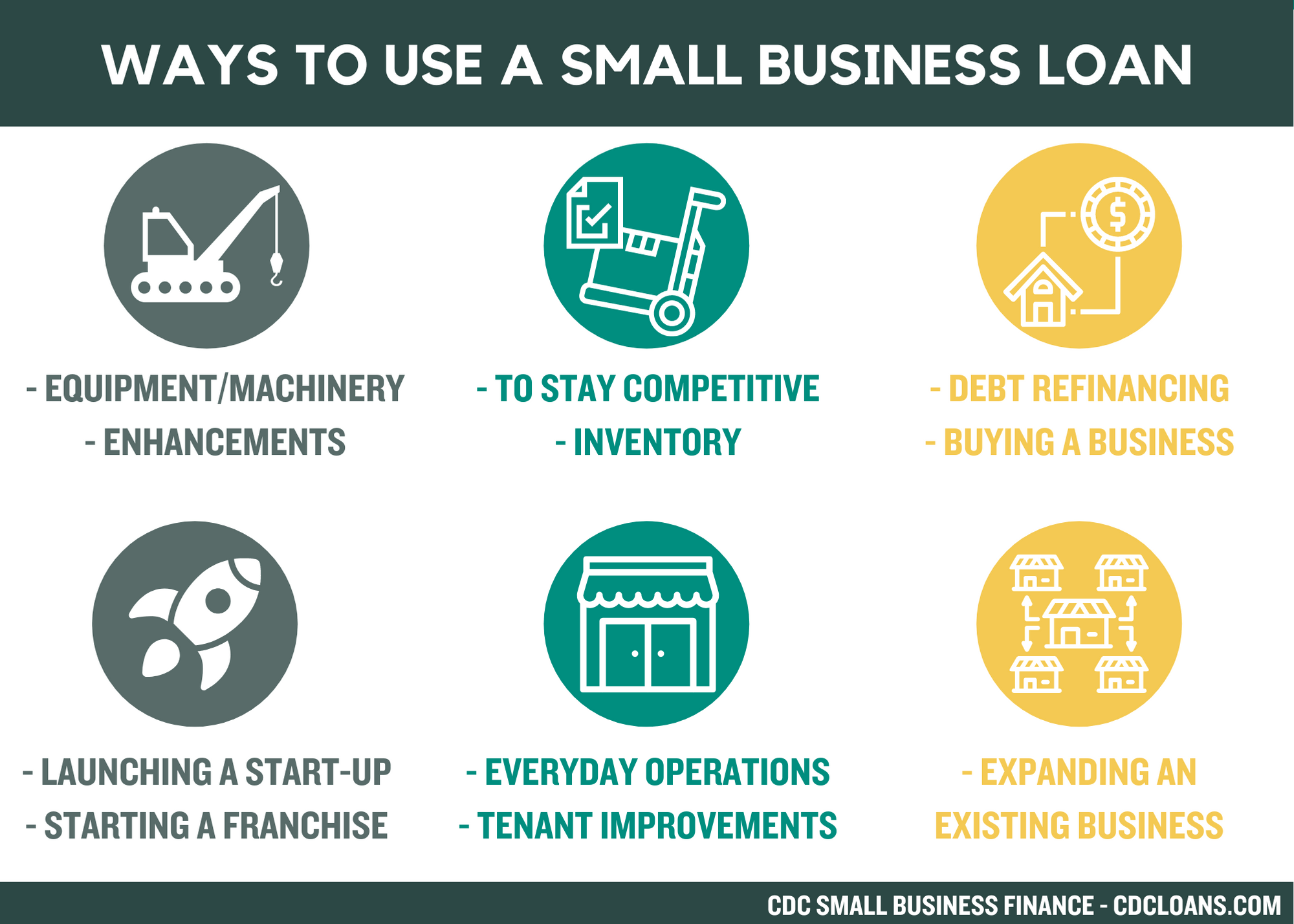

The “why” behind your loan request dictates the “what” of your loan product. Are you purchasing real estate? You likely need a long-term commercial mortgage. Are you buying inventory for the holiday season? A short-term line of credit or merchant cash advance might be more appropriate. Identifying whether your need is for working capital, equipment financing, or debt refinancing is the first step in narrowing down your search.

SBA Loans: The Gold Standard of Business Financing

The U.S. Small Business Administration (SBA) does not lend money directly to business owners. Instead, it guarantees a portion of loans made by partner lenders, reducing the risk for the bank. The SBA 7(a) program is the most popular, offering versatile funding for working capital or debt refinancing. The 504 loan program is specifically designed for major fixed assets like real estate or heavy machinery. While SBA loans offer the lowest interest rates and longest repayment terms, they also require the most documentation and have the longest approval times.

Traditional Bank Loans vs. Online Alternative Lenders

Traditional banks remain the go-to for established businesses with high credit scores and substantial collateral. They offer stability and competitive rates but are notorious for strict “credit boxes.” Conversely, online or “FinTech” lenders have filled the gap for newer businesses or those with less-than-perfect credit. These lenders use proprietary algorithms to assess risk beyond just a credit score, offering faster funding—sometimes within 24 hours—though often at significantly higher interest rates.

The Prerequisites: Building a Creditworthy Profile

A lender’s primary concern is your ability to repay. To assess this, they look at several key financial indicators. Understanding these metrics allows you to “clean up” your financial house before the application hits an underwriter’s desk.

The Significance of Personal and Business Credit Scores

Even if your business is an LLC or a corporation, most lenders will scrutinize your personal credit score, especially for small businesses. A personal FICO score above 680 is generally the threshold for traditional financing. Simultaneously, you should be building a business credit profile through bureaus like Dun & Bradstreet or Experian Business. Timely payments to vendors and low credit utilization on business cards are essential for proving that the entity itself is a reliable borrower.

Understanding the Debt Service Coverage Ratio (DSCR)

Lenders use the Debt Service Coverage Ratio (DSCR) to determine if your business generates enough net operating income to cover its debt obligations. The formula is simple: Net Operating Income divided by Total Debt Service. Most lenders look for a DSCR of 1.25 or higher. This means that for every dollar of debt payment, the business generates $1.25 in profit. If your ratio is lower, you may need to reduce existing overhead or request a smaller loan amount to qualify.

The Role of Collateral and Personal Guarantees

Collateral acts as a safety net for the lender. This can include business assets like equipment, inventory, or accounts receivable, or personal assets like equity in your home. In many cases, especially for small businesses, lenders require a “Personal Guarantee.” This is a legal agreement stating that the business owner is personally responsible for the debt if the business fails to pay. Understanding the weight of this commitment is vital for any business owner’s personal financial security.

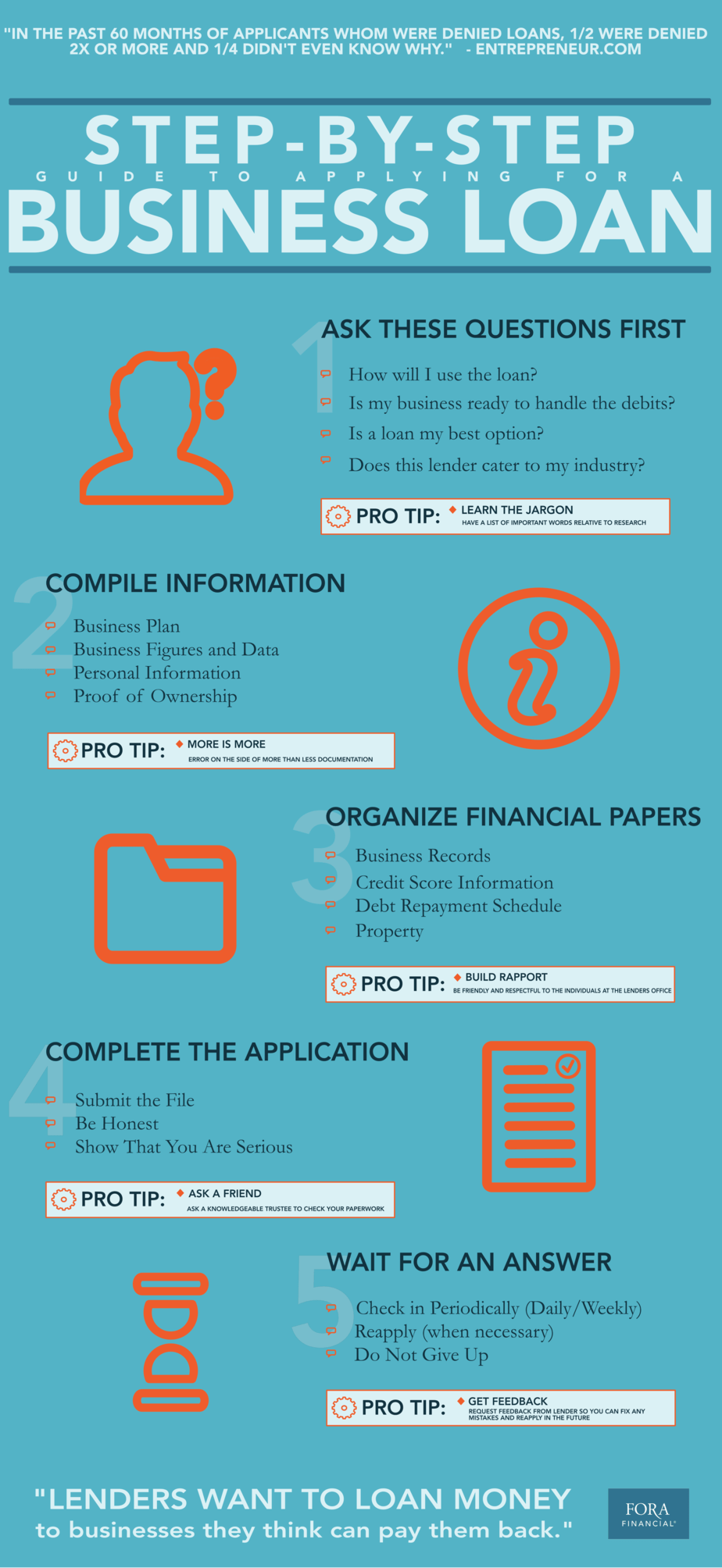

The Documentation Phase: Preparing Your Loan Package

Applying for a loan is a rigorous administrative task. The more organized your documentation, the more professional you appear to a loan officer. A disorganized application is often interpreted as a sign of a disorganized business.

Crafting a Compelling Business Plan

While some online lenders skip this, traditional banks and the SBA require a formal business plan. This document should outline your company’s mission, market analysis, management team, and, most importantly, financial projections for the next three to five years. Your projections must be realistic and backed by historical data or industry benchmarks. This is your opportunity to “sell” the lender on the future of your company.

Essential Financial Statements

You will need to provide at least two to three years of both personal and business tax returns. Additionally, you must produce updated versions of the “Big Three” financial statements:

- Balance Sheet: Showing assets, liabilities, and equity.

- Profit and Loss (P&L) Statement: Showing revenue and expenses over a specific period.

- Cash Flow Statement: Proving that you have the liquidity to handle day-to-day operations while servicing a loan.

Legal and Ownership Documents

Lenders need to know exactly who they are doing business with. Be prepared to provide articles of incorporation, business licenses, commercial leases, and any existing contracts with major clients or suppliers. If your business has multiple partners, each individual with a 20% stake or more will likely need to provide their financial information and undergo a background check.

Evaluating Offers and Managing Long-term Debt

Once you receive an approval, the work shifts from acquisition to evaluation. Not all money is “good” money, and the terms of a loan can be just as impactful as the interest rate.

Analyzing the Annual Percentage Rate (APR)

Many alternative lenders quote “factor rates” or “monthly interest,” which can make a loan look cheaper than it actually is. Always calculate the Annual Percentage Rate (APR), which includes the interest rate plus all fees (origination fees, processing fees, etc.). A loan with a 10% interest rate and a 5% origination fee is significantly more expensive than a flat 12% interest rate loan. Understanding the true cost of capital ensures that your debt doesn’t eat into your profit margins.

Repayment Structures and Prepayment Penalties

The structure of your repayment can affect your daily operations. Traditional loans usually have monthly payments, while some short-term online loans or merchant cash advances require daily or weekly withdrawals from your bank account. This can create a strain on your cash flow. Furthermore, check for “prepayment penalties.” Some lenders charge a fee if you pay the loan off early, as they lose out on the interest they expected to earn. Ideally, you want a loan that rewards you for early repayment.

Post-Funding: Strategic Reinvestment and Relationship Building

After the funds hit your account, the focus moves to stewardship. Use the capital strictly for the purposes outlined in your application. Mixing loan funds with personal expenses is a fast track to financial ruin and potential legal issues. Finally, keep your lender informed. If you hit a rough patch, proactive communication is always better than missing a payment. Maintaining a good relationship with your lender turns them into a long-term partner, making it much easier to secure higher levels of funding as your business scales.

By treating the loan process as a strategic financial exercise rather than a desperate search for cash, you position your business for sustainable growth. The world of business finance is complex, but with the right preparation and a clear understanding of the “Money” niche, securing a small business loan becomes a manageable and transformative milestone for your enterprise.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.