In the modern economic climate, the question “What is the current interest rate?” is rarely met with a single, simple number. Interest rates are the heartbeat of the financial system, influencing everything from the cost of a morning cup of coffee to the long-term feasibility of a thirty-year mortgage. When people ask about current rates, they are typically looking for the Federal Funds Rate, the average mortgage rate, or perhaps the yield on a high-yield savings account.

Understanding these rates is not just an academic exercise; it is a fundamental requirement for sound personal and business financial planning. In an era defined by fluctuating inflation and shifting central bank policies, staying informed about the cost of capital is the difference between financial stagnation and wealth accumulation.

The Federal Funds Rate: The Engine of the Economy

At the core of all interest rates in the United States is the Federal Funds Rate. This is the interest rate at which commercial banks borrow and lend their excess reserves to each other overnight. While it might sound like a niche banking mechanic, it is the primary tool used by the Federal Reserve (the “Fed”) to manage economic growth and price stability.

How the Fed Influences Your Wallet

The Federal Reserve operates under a “dual mandate”: to promote maximum employment and maintain stable prices (low inflation). When inflation rises too high, the Fed increases the Federal Funds Rate. This makes borrowing more expensive for businesses and consumers, which slows down spending and cools the economy. Conversely, when the economy is sluggish, the Fed lowers rates to encourage borrowing and investment.

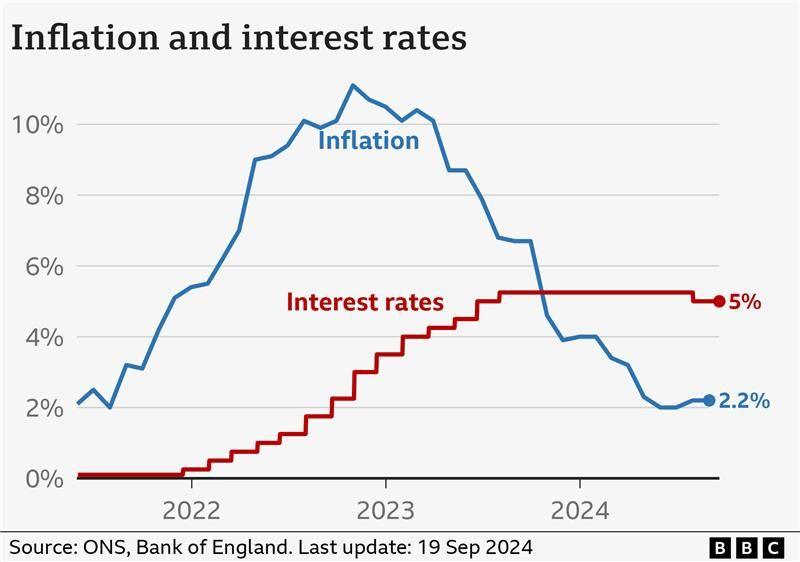

Currently, we are in a transitional period. Following a series of aggressive hikes to combat post-pandemic inflation, the Federal Reserve has shifted its stance toward “maintenance” or gradual reduction. For the consumer, this means that while the “prime rate”—the base rate banks charge their most creditworthy customers—remains higher than it was five years ago, the peak of the rate-hiking cycle has likely passed.

The Ripple Effect on the Prime Rate

The Prime Rate is usually set exactly 3 percentage points above the Federal Funds Rate. If the Fed sets the target range at 5.25% to 5.50%, the Prime Rate will sit at approximately 8.50%. This is the benchmark used for most private student loans, home equity lines of credit (HELOCs), and credit card interest rates. Monitoring the Fed’s monthly meetings is essential for anyone carrying variable-interest debt, as even a quarter-point shift can add thousands of dollars in interest costs over the life of a loan.

The State of Consumer Borrowing: Mortgages and Auto Loans

For most households, the “current interest rate” that matters most is the one attached to their home or vehicle. These rates do not move in perfect lockstep with the Federal Reserve, but they are heavily influenced by the same economic indicators—specifically the yield on the 10-Year Treasury Note.

Navigating the Mortgage Market

Mortgage rates reached historic lows during 2020 and 2021, often dipping below 3%. Today, the landscape is vastly different. Current 30-year fixed-rate mortgages have hovered between 6% and 7.5% recently, significantly impacting housing affordability.

When rates are high, the “purchasing power” of the average buyer diminishes. For example, a $2,500 monthly budget might have bought a $500,000 home at a 3% interest rate, but at 7%, that same budget might only support a $350,000 loan. This shift has led to a “lock-in effect,” where current homeowners are reluctant to sell and move because they do not want to trade their existing 3% rate for a new 7% rate.

The Rising Cost of Auto Financing and Credit Cards

The impact of current interest rates is arguably most painful in the realms of short-to-medium-term debt. Auto loan rates have climbed steadily, with well-qualified buyers often seeing rates between 5% and 8%, while those with average credit may face double-digit interest.

Credit cards are even more sensitive. Because most credit cards have variable Annual Percentage Rates (APRs), they rise almost immediately after a Fed rate hike. Currently, the average credit card APR is over 20%, the highest in decades. For those carrying a balance, the interest charges can quickly become a “debt spiral,” where the monthly payment barely covers the interest, leaving the principal balance untouched.

The Silver Lining: Interest Rates as a Tool for Savers

While high interest rates are a burden for borrowers, they represent a golden age for savers. For over a decade following the 2008 financial crisis, interest rates on savings accounts were practically zero, meaning money kept in a bank actually lost purchasing power due to inflation.

High-Yield Savings Accounts (HYSA)

In the current environment, the “current interest rate” for savers is quite attractive. High-yield savings accounts, often offered by online-only banks, are providing APYs (Annual Percentage Yields) ranging from 4% to over 5%. This is a significant shift from the 0.01% offered by many traditional brick-and-mortar institutions.

For an individual with a $20,000 emergency fund, the difference is stark. At 0.01%, that fund earns $2 a year. At 5%, it earns $1,000 a year. Utilizing high-yield accounts has become a critical strategy for personal finance management in 2024 and 2025.

Certificates of Deposit (CDs) and Treasury Bills

For those who do not need immediate access to their cash, Certificates of Deposit (CDs) and U.S. Treasury Bills offer a way to “lock in” current high rates. If the Federal Reserve begins to cut rates in the coming months, the interest offered on savings accounts will drop quickly. However, a CD allows a saver to guarantee a specific rate for a set term, such as 12 or 24 months.

U.S. Treasury Bills (T-Bills) are also a popular choice for conservative investors. They are backed by the full faith and credit of the government and currently offer yields that compete with the best savings accounts, often with the added benefit of being exempt from state and local taxes.

Strategic Financial Management in a High-Rate Environment

In a world where the cost of money is high, your financial strategy must evolve. The “cheap money” era of the 2010s allowed for certain risks and inefficiencies that are no longer sustainable.

Prioritizing Debt Repayment

The first priority in a high-interest environment is aggressive debt management. If you have high-interest debt, such as credit card balances or personal loans, the “Interest Avalanche” method is highly effective. This involves paying the minimum on all debts while putting every extra dollar toward the debt with the highest interest rate. In today’s market, paying off a credit card with a 22% APR is the equivalent of a guaranteed 22% return on your investment—a figure that no stock market index can consistently promise.

Re-evaluating Investment Valuations

Interest rates also dictate the value of investments. In the world of business finance, the “Discounted Cash Flow” (DCF) model is used to value companies. When interest rates rise, the “discount rate” applied to future earnings also rises, which generally lowers the current value of a stock.

This is particularly true for growth stocks and tech companies that expect to make most of their money in the distant future. As a result, many investors have shifted their focus toward “value” stocks—companies that are already profitable and pay dividends—which tend to be more resilient when interest rates are high.

Future Outlook: Will Rates Go Down?

The most common follow-up to “What is the current interest rate?” is “When will it go down?” The answer depends entirely on economic data, specifically the Consumer Price Index (CPI) and employment reports.

The Path to “Neutral”

Economists often speak of a “neutral” interest rate—a rate that neither stimulates nor restricts the economy. Most estimates place this neutral rate somewhere between 2.5% and 3.5%. Currently, we are well above that level, meaning the Fed’s policy is “restrictive.”

The consensus among market analysts is that as inflation continues its slow descent toward the 2% target, the Federal Reserve will begin a cycle of “normalization” cuts. However, consumers should not expect a return to the 0% rates of the past. Those were emergency measures for extreme crises. A “normal” interest rate environment likely means mortgage rates in the 5% to 6% range and savings rates in the 3% range.

Conclusion: Staying Agile

Interest rates are the weather of the financial world. You cannot control them, but you can certainly dress for them. By understanding the current Federal Funds Rate, choosing the right borrowing products, and maximizing the yield on your savings, you can protect your purchasing power and grow your net worth regardless of what the Fed decides in its next meeting.

In this environment, financial literacy is your greatest asset. Whether you are looking to buy a home, start a business, or simply optimize your savings, staying tuned to the current interest rate landscape is the foundation of a successful financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.