For most individuals, a home is the most significant purchase they will ever make. Because the cost of real estate often exceeds the average person’s liquid savings, the global financial system relies on a specialized instrument known as a mortgage loan. A mortgage is not merely a debt; it is a sophisticated financial tool designed to facilitate property ownership while mitigating risk for the lender. Understanding the intricacies of how these loans function is the cornerstone of personal financial literacy and long-term wealth building.

Understanding the Mechanics of a Mortgage Loan

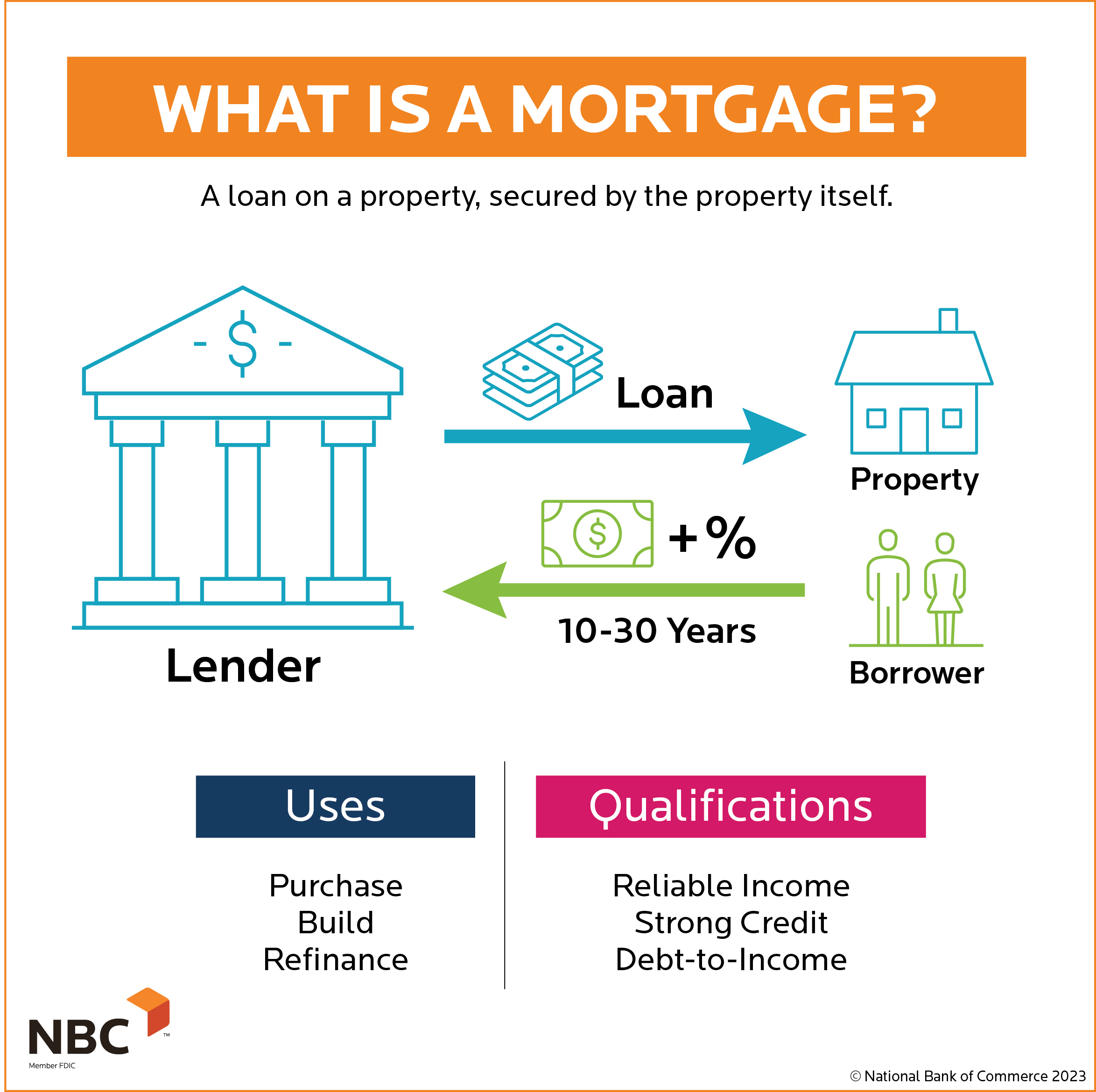

At its core, a mortgage is a legal agreement in which a borrower receives funds from a lender (usually a bank or mortgage company) to purchase a property. The borrower agrees to pay back the loan over a specific period, typically 15 to 30 years, with interest. What distinguishes a mortgage from other types of personal debt is the concept of collateral.

Principal and Interest

Every mortgage payment is comprised of two primary components: principal and interest. The principal is the actual amount of money borrowed to purchase the home. The interest is the cost of borrowing that money, expressed as a percentage. In the early years of a mortgage, a higher percentage of the monthly payment goes toward interest. As the loan matures, a greater portion is applied to the principal—a process known as amortization.

Collateral and Liens

In a mortgage agreement, the property itself serves as collateral. This means the lender holds a “lien” on the property title. If the borrower fails to meet the repayment terms, the lender has the legal right to seize the property through a process called foreclosure. This security allows lenders to offer much lower interest rates on mortgages compared to unsecured debts like credit cards or personal loans.

The Role of Down Payments

A down payment is the initial upfront portion of the total purchase price paid by the buyer. In the realm of personal finance, the down payment serves as the buyer’s initial equity in the home. While 20% is often cited as the gold standard to avoid additional costs, many modern loan programs allow for down payments as low as 3% or even 0% for specific demographics. However, a larger down payment reduces the total loan amount, lowers monthly payments, and often secures a better interest rate.

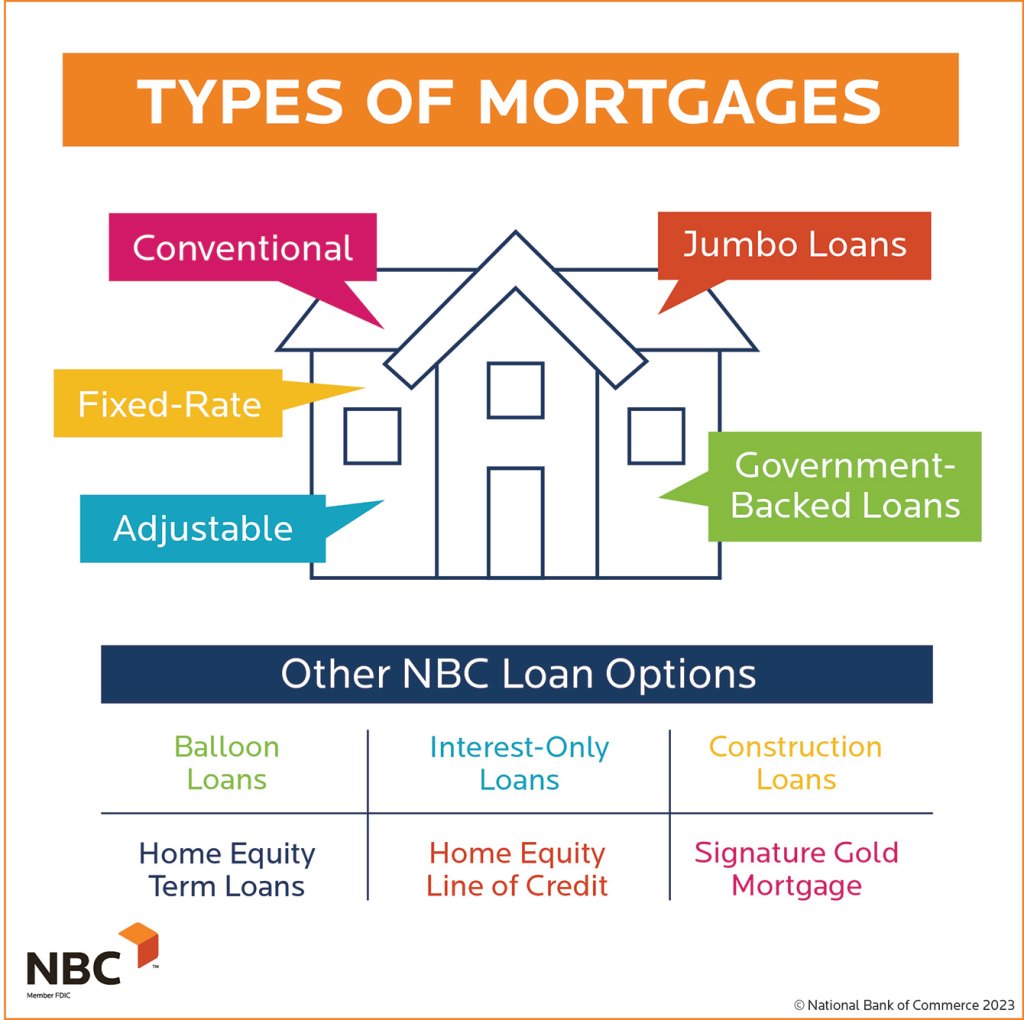

Diverse Types of Mortgage Loans

The financial market offers a variety of mortgage products tailored to different economic situations, risk tolerances, and long-term goals. Selecting the right type of loan can save a homeowner tens of thousands of dollars over the life of the debt.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

A fixed-rate mortgage maintains the same interest rate for the entire duration of the loan. This provides predictability and protection against rising market rates, making it the most popular choice for long-term homeowners.

Conversely, an Adjustable-Rate Mortgage (ARM) offers a lower initial interest rate for a set period (e.g., five or seven years), after which the rate adjusts periodically based on market indices. ARMs can be beneficial for those who plan to sell or refinance before the introductory period ends, but they carry the risk of significantly higher payments if interest rates climb.

Government-Backed Loans

To encourage homeownership, various government agencies provide insurance or guarantees on loans issued by private lenders.

- FHA Loans: Insured by the Federal Housing Administration, these are popular among first-time buyers due to lower credit score requirements and down payments as low as 3.5%.

- VA Loans: Guaranteed by the Department of Veterans Affairs, these offer $0 down payment options for active-duty service members and veterans.

- USDA Loans: These target rural and suburban homebuyers with low-to-moderate incomes, often requiring no down payment.

Conventional and Jumbo Loans

Conventional loans are not insured by the federal government and typically follow the lending guidelines set by Fannie Mae and Freddie Mac. They often require higher credit scores but offer more flexibility. When a loan amount exceeds the “conforming limits” set by these entities—common in high-cost real estate markets—it is classified as a Jumbo Loan, which usually carries stricter qualification requirements and higher interest rates.

The Financial Lifecycle of a Mortgage

The journey of a mortgage begins long before the keys are handed over and continues until the final payment is recorded. Navigating this cycle requires a strategic approach to personal finance.

The Application and Pre-Approval Process

Before shopping for a home, savvy buyers seek “pre-approval.” This involves a lender reviewing the borrower’s tax returns, pay stubs, bank statements, and credit history to determine the maximum loan amount. Pre-approval serves as a financial “green light,” signaling to sellers that the buyer is serious and financially capable. During the formal application, lenders perform a deep dive into the borrower’s financial health to finalize the loan terms.

Amortization: How Your Payments Work

Most mortgages follow an amortization schedule. In a standard 30-year fixed-rate mortgage, the monthly payment remains the same, but the internal distribution changes. In the first month, interest is calculated based on the full loan balance. As the balance decreases each month, the interest portion of the payment shrinks, and the principal portion grows. Understanding this schedule is vital for homeowners who wish to strategically make extra payments to reduce the total interest paid over time.

Closing Costs and Escrow

The “sticker price” of a home does not include the various fees associated with finalizing a mortgage. Closing costs—which include appraisal fees, title insurance, attorney fees, and origination fees—typically range from 2% to 5% of the purchase price. Additionally, many lenders require an escrow account. This is a neutral holding area where a portion of the monthly mortgage payment is set aside to pay for annual property taxes and homeowners insurance, ensuring these critical bills are paid on time.

Factors That Influence Your Mortgage Terms

A mortgage is not a one-size-fits-all product. Lenders use several metrics to calculate the level of risk a borrower represents, which directly impacts the interest rate and terms offered.

Credit Scores and Debt-to-Income (DTI) Ratios

A credit score is perhaps the most influential factor in securing a favorable mortgage. A higher score demonstrates a history of responsible debt management, qualifying the borrower for the lowest available interest rates. Equally important is the Debt-to-Income (DTI) ratio, which measures the percentage of monthly gross income that goes toward paying debts. Most lenders prefer a DTI ratio below 36%, though some programs allow for higher limits.

The Impact of Interest Rates and Inflation

Mortgage rates are heavily influenced by the broader economy, specifically the Federal Reserve’s monetary policy and the yield on the 10-year Treasury note. When inflation is high, interest rates typically rise to cool the economy, making mortgages more expensive. Conversely, in a sluggish economy, rates may drop to encourage borrowing. Timing a mortgage application during a low-rate environment can lead to massive long-term savings.

Private Mortgage Insurance (PMI)

If a borrower puts down less than 20% on a conventional loan, lenders usually require Private Mortgage Insurance (PMI). This insurance protects the lender—not the borrower—in the event of a default. While PMI allows for lower down payments, it adds an extra monthly cost. Once the homeowner reaches 20% equity in the property through appreciation or principal pay-down, they can usually request to have PMI removed, effectively lowering their monthly obligation.

Strategic Mortgage Management for Long-Term Wealth

For the financially astute, a mortgage is more than a monthly bill; it is a component of a larger investment portfolio. Managing a mortgage effectively can accelerate net worth and provide financial flexibility.

Refinancing and Home Equity

Refinancing involves replacing an existing mortgage with a new one, typically to secure a lower interest rate, change the loan term, or tap into home equity. As property values rise and the loan balance decreases, the “equity” (the difference between the home’s value and the loan balance) grows. Homeowners can use a “cash-out refinance” to access this equity for home improvements, debt consolidation, or other investments, though this increases the total debt.

Accelerated Payments and Early Payoff

One of the most effective ways to build wealth is to minimize interest expenses. By making one extra payment per year or slightly increasing the monthly principal payment, a homeowner can shave years off a 30-year mortgage. However, investors must weigh this against the “opportunity cost.” If the mortgage interest rate is 3% and the stock market is returning 7%, it may be more mathematically advantageous to invest extra cash rather than paying down the low-interest mortgage early.

The Mortgage as a Hedge Against Inflation

In a unique way, a fixed-rate mortgage serves as a hedge against inflation. While the price of consumer goods and the cost of rent tend to rise with inflation, a fixed-rate mortgage payment stays the same. Over a 20-year period, the “real” value of that monthly payment decreases as the borrower’s income likely rises with inflation, effectively making the debt cheaper to service over time.

In conclusion, a mortgage loan is a multifaceted financial instrument that serves as the bridge between current income and future property ownership. By mastering the nuances of loan types, interest rates, and equity management, individuals can transform a simple debt into a powerful engine for personal financial stability and generational wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.