The year 2008 is etched into the collective memory as a period of profound financial upheaval, marking the onset of the Great Recession – the most severe economic downturn since the Great Depression of the 1930s. What began as a seemingly localized issue in the U.S. housing market rapidly metastasized into a global financial crisis, bringing some of the world’s largest financial institutions to their knees and sending shockwaves through every facet of personal finance, investment, and business. Understanding the intricate web of factors that converged to create this cataclysmic event is crucial for investors, consumers, and policymakers alike, offering invaluable lessons in risk management, market dynamics, and the interconnectedness of the global economy.

The Unraveling of the Housing Market: A House of Cards

The genesis of the 2008 recession can be traced directly back to a speculative bubble in the U.S. housing market, fueled by a dangerous cocktail of lax lending standards, innovative but ultimately toxic financial products, and an irrational exuberance among borrowers and lenders alike.

Subprime Lending Spree: The Foundation of Fragility

At the heart of the housing bubble was the proliferation of “subprime” mortgages. These were loans extended to borrowers with poor credit histories, low incomes, or high debt-to-income ratios, who would traditionally not qualify for conventional mortgages. Driven by a desire to expand homeownership and the promise of ever-increasing profits from securitized mortgages, lenders increasingly relaxed their underwriting standards. Mortgage brokers and originators, incentivized by commissions, aggressively marketed these loans, often without fully explaining the risks to borrowers. Many subprime mortgages featured adjustable-rate terms (ARMs) that began with low “teaser” rates, only to reset to significantly higher rates after a few years, making payments unaffordable for many borrowers. This aggressive push, coupled with the belief that housing prices would perpetually rise, created a self-reinforcing cycle of demand and speculation.

The Rise of Mortgage-Backed Securities (MBS) and CDOs: Amplifying Risk

The financial innovation that transformed localized mortgage risk into systemic global risk was the securitization of these loans. Lenders would package thousands of individual mortgages, including many subprime ones, into complex financial instruments called Mortgage-Backed Securities (MBS). These MBS were then sold to investors worldwide, including pension funds, hedge funds, and other banks, providing lenders with fresh capital to issue even more mortgages.

The complexity deepened with the creation of Collateralized Debt Obligations (CDOs). Investment banks would take tranches (slices) of various MBS, along with other asset-backed securities, and repackage them into new CDOs. These CDOs were then further divided into different risk classes, with “senior” tranches rated highly by credit rating agencies despite being backed by increasingly risky underlying assets. The rating agencies, often paid by the very institutions creating these products, failed to adequately assess the risk, giving AAA ratings to instruments that were far from safe. This process effectively obscured the true risk profile of the underlying subprime mortgages, spreading toxic assets throughout the global financial system and creating a highly opaque “shadow banking” system.

Housing Bubble Burst: The Inevitable Peak and Decline

For a time, the system seemed to work. Housing prices continued their upward trajectory, allowing many subprime borrowers to refinance their loans or sell their homes for a profit if payments became too high. However, this was a classic speculative bubble, unsustainable in the long run. As the Federal Reserve began raising interest rates in the mid-2000s to combat inflation, the cost of borrowing increased. Simultaneously, the low teaser rates on many subprime ARMs began to reset to much higher rates.

Millions of homeowners found themselves unable to afford their mortgage payments. Foreclosures surged, and the inventory of unsold homes began to climb. By 2006-2007, housing prices, which had seen unprecedented gains, peaked and began to fall precipitously. This decline had a devastating effect: borrowers could no longer refinance or sell their homes to escape unaffordable payments, as their homes were now “underwater” – worth less than the mortgage owed on them. The flood of foreclosures further depressed housing values, creating a vicious cycle that ultimately popped the bubble and initiated a cascade of losses across the financial system.

Contagion and Systemic Risk: The Domino Effect

The implosion of the housing market revealed the deep structural flaws and interconnectedness of the global financial system. What started as a problem in residential mortgages quickly turned into a full-blown financial crisis as the value of MBS and CDOs plummeted, infecting institutions worldwide.

Financial Institutions on the Brink: A Crisis of Confidence

As the underlying subprime mortgages defaulted, the value of the MBS and CDOs backed by them evaporated. Financial institutions that had heavily invested in these instruments, believing them to be safe and highly rated, faced massive write-downs and liquidity crises. The first major casualty was Bear Stearns, one of the oldest and largest investment banks, which collapsed in March 2008 and was hastily acquired by JPMorgan Chase with Federal Reserve assistance. This event signaled the severity of the crisis.

The crisis intensified in September 2008. Fannie Mae and Freddie Mac, government-sponsored enterprises that guaranteed and purchased a vast share of U.S. mortgages, were placed into conservatorship, effectively nationalized, to prevent their collapse. Days later, Lehman Brothers, another venerable investment bank, filed for bankruptcy – the largest bankruptcy in U.S. history. The decision not to bail out Lehman sent shockwaves through the markets, triggering widespread panic and an immediate loss of confidence in other major financial institutions. Merrill Lynch was forced into a fire sale acquisition by Bank of America, and the giant insurer AIG, which had written billions in credit default swaps, faced imminent collapse, requiring an unprecedented government bailout. These events demonstrated the profound systemic risk, where the failure of one major institution threatened to bring down the entire financial system.

The Role of Credit Default Swaps (CDS): Insurance That Amplified Danger

Compounding the problem was the unregulated market for Credit Default Swaps (CDS). These were essentially insurance contracts against the default of a bond or other debt instrument, such as MBS or CDOs. Investors could buy CDS to protect against losses, or they could sell CDS as a form of speculation. However, unlike traditional insurance, CDS contracts could be traded multiple times, and often, those buying CDS didn’t even own the underlying asset they were insuring, turning them into speculative bets.

AIG, in particular, had written hundreds of billions of dollars’ worth of CDS on MBS and CDOs. When these underlying assets began to default, AIG faced immense claims it couldn’t pay, putting it on the brink of collapse. The potential failure of AIG threatened to bankrupt not only its direct counterparties (banks that had bought CDS from AIG) but also countless other institutions indirectly tied to those counterparties, illustrating how an unregulated financial product could amplify risk and spread contagion throughout the global financial system.

Freezing of Credit Markets: Starving the Economy

The implosion of these major financial institutions and the uncertainty surrounding the value of their assets led to an almost complete seizure of the interbank lending market. Banks, fearing that other banks might be holding worthless assets or be on the verge of collapse, stopped lending to each other. This “credit crunch” meant that even healthy banks couldn’t get the short-term funding they needed to operate, impacting their ability to lend to businesses and consumers.

With credit drying up, businesses struggled to finance their operations, invest, or make payroll. Consumers found it harder to obtain mortgages, auto loans, or credit card financing. The flow of money, the lifeblood of any modern economy, effectively stopped, leading to widespread layoffs, business failures, and a sharp contraction in economic activity. The global economy teetered on the brink of a complete meltdown.

Government Intervention and Bailouts: Stemming the Tide

Faced with an unprecedented crisis, governments and central banks around the world were forced to take extraordinary measures to prevent a total financial collapse and restore stability.

TARP and Emergency Liquidity: The Federal Reserve’s Unprecedented Actions

In the U.S., the most significant legislative response was the Emergency Economic Stabilization Act of 2008, which created the Troubled Asset Relief Program (TARP). This controversial $700 billion program authorized the U.S. Treasury to purchase troubled assets (primarily MBS) from struggling banks and to inject capital directly into financial institutions through preferred stock purchases. The aim was to recapitalize banks, restore confidence, and unfreeze credit markets. While initially unpopular, TARP is widely credited with preventing a deeper financial catastrophe, and ultimately, most of the money lent was repaid with interest.

The Federal Reserve also played a critical role, acting as the “lender of last resort.” It dramatically cut interest rates to near zero, established numerous emergency lending facilities to provide liquidity to banks and other financial institutions, and embarked on “quantitative easing” – purchasing vast amounts of government bonds and other securities to inject money into the financial system and lower long-term interest rates. These unconventional measures were unprecedented in scope and scale.

Nationalization and Mergers: A Swift Response

Beyond TARP, the government orchestrated the effective nationalization of Fannie Mae and Freddie Mac and oversaw the forced mergers of several struggling institutions. The bailout of AIG, a company deemed “too big to fail,” involved the government taking a nearly 80% stake, extending tens of billions of dollars in loans to prevent its collapse and the ensuing ripple effect on its counterparties. These interventions, while politically unpopular, were seen as necessary to stabilize the financial system and protect the broader economy.

Global Repercussions: A World Interconnected

The crisis quickly transcended U.S. borders. European banks were significant holders of U.S. MBS and CDOs, and the freezing of credit markets affected financial institutions globally. Governments worldwide responded with their own stimulus packages, bank recapitalizations, and interest rate cuts. The crisis exposed the deeply interconnected nature of the global financial system, demonstrating that a severe shock in one major economy could rapidly propagate around the world, leading to a synchronous global recession.

The Aftermath and Long-Term Implications for Personal Finance and Investing

The immediate aftermath of the 2008 recession was marked by a severe global economic contraction, massive job losses, and a deep sense of insecurity among individuals and households. Its long-term implications continue to shape personal finance and investing today.

Shifting Regulatory Landscape: Dodd-Frank and Prevention Efforts

In response to the crisis, governments moved to overhaul financial regulations. In the U.S., the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 was enacted, aiming to prevent a recurrence of the crisis. Key provisions included stricter oversight of financial institutions, regulation of derivatives (like CDS), creation of the Consumer Financial Protection Bureau (CFPB) to protect consumers in financial transactions, and increased capital requirements for banks. While its effectiveness and scope remain subjects of debate, Dodd-Frank represented a significant effort to address the systemic vulnerabilities exposed by the crisis.

Investor Behavior and Risk Aversion: A Generation Scarred

The recession profoundly impacted investor psychology. Many individuals, especially those nearing retirement, saw significant portions of their savings and 401(k)s wiped out. This experience fostered a heightened sense of risk aversion, leading some to withdraw from equity markets or adopt more conservative investment strategies. A generation of investors became more skeptical of complex financial products and the pronouncements of financial institutions, emphasizing the importance of transparency and understanding what one invests in. The concept of “home as an ATM” or an ever-appreciating asset was thoroughly debunked, leading to a more cautious approach to real estate as an investment.

Impact on Personal Wealth and Retirement: A Slow Recovery

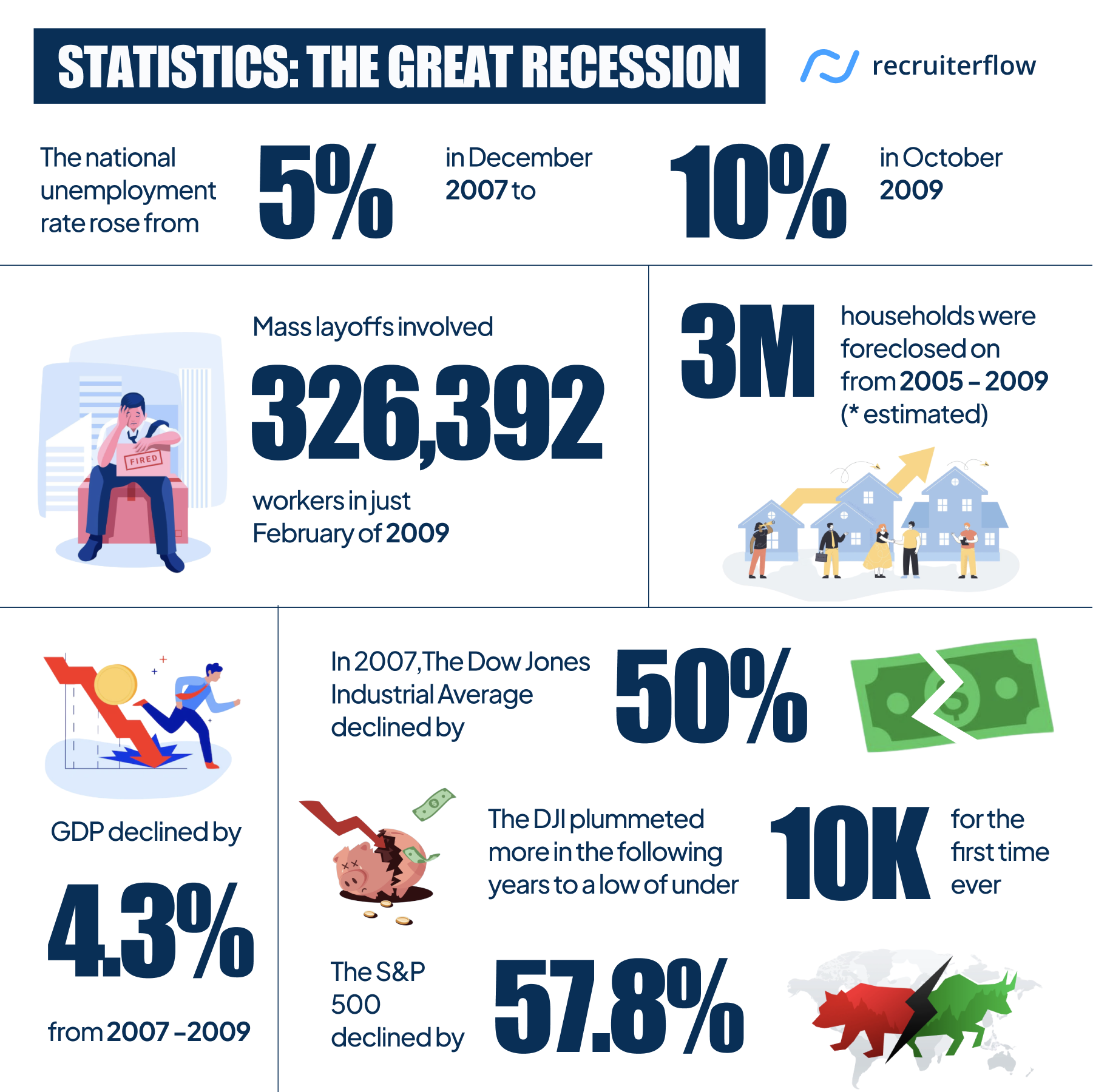

For millions, the recession meant job losses, foreclosures, and a significant decline in household wealth. The unemployment rate surged, peaking at 10% in October 2009. Many individuals struggled to recover their financial footing, leading to delayed retirements, increased personal debt, and a widening wealth gap. While the economy eventually recovered, the scars of the Great Recession lingered for years, affecting everything from wage growth to consumer spending habits. The crisis underscored the critical importance of emergency savings, diversified portfolios, and prudent debt management in protecting personal financial stability against unexpected economic shocks.

Lessons Learned and Future Preparedness

The 2008 recession was a painful but ultimately instructive period. It offered invaluable lessons about the inherent risks in complex financial systems, the importance of robust regulation, and the critical need for financial literacy at every level.

The Importance of Financial Literacy: Understanding Risks

One of the clearest takeaways is the paramount importance of financial education. Many borrowers did not fully understand the terms of their subprime mortgages, and many investors did not grasp the risks embedded in MBS and CDOs. For individuals, understanding concepts like compound interest, debt management, investment diversification, and the true cost of credit is essential. For businesses, comprehending market risks, liquidity management, and the implications of financial leverage is crucial. A well-informed populace and business community are better equipped to make sound financial decisions and resist speculative bubbles.

Strengthening Financial Resilience: Preparing for the Unexpected

The recession highlighted the vulnerability of those with inadequate savings and excessive debt. Building a strong financial foundation is now recognized as more critical than ever. This includes maintaining an emergency fund equivalent to several months of living expenses, avoiding high-interest debt, living within one’s means, and investing prudently for long-term goals. For businesses, maintaining healthy cash reserves and diversifying funding sources are key to weathering economic storms. The crisis reinforced the notion that while financial innovation can drive growth, it must be balanced with transparency, robust oversight, and a healthy skepticism towards promises of easy wealth.

The 2008 recession stands as a stark reminder of the intricate and often volatile nature of global financial markets. Its legacy continues to shape financial policy, corporate strategy, and individual financial decisions, underscoring the enduring need for vigilance, prudence, and an informed approach to personal finance and investing.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.