Navigating the intricacies of retirement planning in the UK begins with a fundamental understanding: the State Pension age. Far from a static figure, the age at which UK citizens can claim their State Pension has been a subject of significant governmental review and adjustment, reflecting demographic shifts, economic realities, and evolving life expectancies. For anyone planning their financial future, from young professionals to those nearing retirement, grasping the current and projected State Pension age is not merely a bureaucratic detail but a critical cornerstone of a robust personal finance strategy. This article delves into the specifics of the UK State Pension age, its trajectory, and the essential steps you need to take to ensure a financially secure retirement.

The Evolving Landscape of the UK State Pension Age

The State Pension age in the UK has undergone significant transformations over recent decades, moving from a fixed age for men and women to a more dynamic, increasingly equalised, and rising benchmark. These changes are driven by a complex interplay of factors, primarily the nation’s changing demographics and the imperative to ensure the long-term sustainability of the State Pension system.

Current State Pension Age

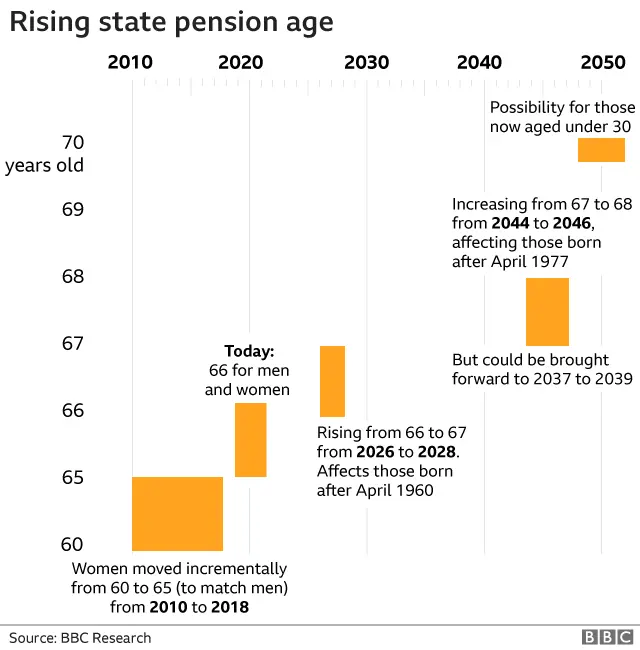

As of the current system, the State Pension age in the UK for both men and women stands at 66 years old. This represents the culmination of a gradual equalisation process, which saw women’s State Pension age rise from 60 to 65 between 2010 and 2018, before both genders’ ages were increased to 66 by October 2020. This harmonisation marked a significant shift, ending the historical disparity in State Pension ages between men and women and setting a universal benchmark for eligibility. Understanding this current age is the baseline for all personal retirement calculations, but it is merely the starting point in a continually moving landscape.

How Your State Pension Age is Determined

The process by which the State Pension age is set and subsequently adjusted is far from arbitrary. It is primarily influenced by government reviews, actuarial projections, and a mandate to balance societal welfare with fiscal responsibility. Key factors include:

- Life Expectancy: Perhaps the most significant driver, increasing life expectancy means people are living longer in retirement, placing greater strain on the State Pension fund. Adjusting the pension age aims to reflect this extended period of receiving benefits.

- Demographic Changes: Birth rates, migration, and the proportion of the working-age population relative to retirees all play a role. A shrinking workforce supporting a growing retired population necessitates adjustments.

- Financial Sustainability: The government’s ability to fund the State Pension system is paramount. Reviews assess the affordability of the current system and project future costs, leading to recommendations for changes to ensure the system remains viable without placing an undue burden on taxpayers.

The official way to determine your precise State Pension age is through the UK government’s online checker. This tool takes your date of birth and calculates your exact eligibility age, which is crucial as transition periods can sometimes mean slight variations for those born around the cusp of changes.

Future Projections and Increases

The current State Pension age of 66 is not the final destination. The UK government has already legislated for further increases and has proposed even more in the pipeline, underscoring the dynamic nature of retirement planning:

- Age 67 by 2028: The State Pension age is set to rise to 67 for both men and women between 2026 and 2028. This increase will primarily affect those born on or after 6 April 1960.

- Age 68 by 2046 (and potentially earlier): The government has long-term plans to increase the State Pension age to 68 between 2044 and 2046. However, recent independent reviews (such as the Cridland Review and the review by Baroness Neville-Rolfe) have recommended bringing this increase forward to between 2037 and 2039. While no final decision has been made on accelerating this timeline, the strong possibility of an earlier rise to 68 highlights the constant need for individuals to monitor policy developments and adapt their financial plans accordingly. These future increases are critical considerations for anyone under the age of 50, as they are highly likely to be affected.

Financial Implications for Your Retirement Planning

The evolving State Pension age has profound implications for personal finance and retirement planning. It dictates how long you might need to work, how much you need to save, and the overall shape of your financial independence. Proactive planning is not just advisable; it’s essential.

The Gap Between Desired Retirement and State Pension Age

One of the most immediate impacts of a rising State Pension age is the potential for a growing gap between when individuals might wish to retire and when they become eligible for their State Pension. Many people aspire to retire earlier than 66, 67, or 68, whether for health reasons, personal choice, or to pursue other interests. However, without adequate alternative income streams, early retirement becomes financially challenging, as individuals would need to fund this period entirely from private savings or other pensions without the safety net of the State Pension. This potential gap necessitates careful financial modelling, considering how many years one might need to cover solely from personal provisions. Failing to account for this gap can lead to unexpected financial strain during what should be a comfortable transition into retirement.

Increased Reliance on Private Pensions and Savings

With the State Pension age rising and the State Pension itself designed to be a foundation rather than a sole source of income, there is an ever-increasing emphasis on personal responsibility for retirement provision. This means that private pensions, such as workplace pensions (often established through auto-enrolment) and personal pensions (like Self-Invested Personal Pensions or SIPPs), along with other forms of savings and investments, are becoming more critical than ever.

The State Pension alone provides a relatively modest income, currently around £221.20 per week for the full new State Pension (2024/25 figures). For most, this amount is insufficient to maintain their desired lifestyle in retirement. Therefore, individuals must build a robust private retirement pot through consistent contributions to workplace schemes, making additional voluntary contributions (AVCs), or investing in personal pension products and other savings vehicles. The earlier one starts saving, the more time investments have to grow through compounding, significantly easing the burden of later-life contributions.

Adapting Your Financial Strategy

The dynamic nature of the State Pension age demands a flexible and adaptive financial strategy. What might have been a suitable plan a decade ago may no longer be appropriate. Regular reviews of your retirement goals, savings rate, and investment performance are crucial. This adaptability involves:

- Re-evaluating your target retirement age: Is your desired retirement age still realistic given the State Pension age and your current savings?

- Adjusting contribution levels: If your State Pension age has shifted, or if you’re behind on your savings goals, you might need to increase your monthly contributions to your private pensions and other investments.

- Considering investment strategies: As the timeline to retirement changes, so too might the appropriateness of certain investment risks. A longer working life might allow for a longer investment horizon, potentially justifying a different risk profile.

- Building a buffer: Financial advisors often recommend building a “buffer” to cover unexpected costs or periods of unemployment before retirement. A rising State Pension age makes this buffer even more critical for navigating potential changes or desired early retirement.

Building a Robust Multi-Pillar Retirement Strategy

A financially secure retirement in the UK relies not on a single source of income but on a multi-pillar strategy. This approach combines the foundational State Pension with robust private provisions and diversified investments, creating a comprehensive safety net and ensuring a comfortable post-work life.

Maximising Your Workplace and Personal Pensions

The cornerstone of private retirement savings for many UK citizens is the pension. These come in two main forms:

- Workplace Pensions: Since the introduction of auto-enrolment in 2012, most employees are automatically enrolled into a workplace pension scheme. This is a significant advantage as both you and your employer contribute, and the government adds tax relief, effectively boosting your savings with three sources of money. It is crucial to contribute at least enough to get your employer’s maximum contribution, as this is essentially free money you would otherwise miss out on. Consider increasing your contributions beyond the minimum, perhaps through Additional Voluntary Contributions (AVCs), if your budget allows.

- Personal Pensions: For the self-employed, those who are not auto-enrolled, or individuals wishing to consolidate previous workplace pensions, personal pensions (such as Self-Invested Personal Pensions or SIPPs) offer greater control. SIPPs allow you to choose from a wide range of investments, from funds and shares to investment trusts. These also benefit from tax relief on contributions. Regularly reviewing the performance and charges of your personal pension is vital to ensure it aligns with your financial goals.

Diversifying with Savings and Investments

While pensions are tax-efficient vehicles specifically designed for retirement, a well-rounded strategy also includes other forms of savings and investments. These provide flexibility and liquidity that pensions, with their access restrictions, cannot:

- ISAs (Individual Savings Accounts):

- Stocks & Shares ISAs: Offer a tax-efficient way to invest in the stock market, with all capital gains and income (dividends) being tax-free. These are excellent for long-term growth and can complement pensions.

- Cash ISAs: Provide a tax-free home for your accessible savings, suitable for emergency funds or shorter-term goals.

- General Investment Accounts (GIAs): For those who have maximised their ISA allowance, GIAs allow further investment, though capital gains and income will be subject to tax.

- Property: For some, property can form part of a retirement strategy, either as an asset to downsize from later to release equity, or as a source of rental income if additional properties are owned. However, property comes with its own risks and illiquidity.

The principle of diversification is key across all investments. Spreading your money across different asset classes, sectors, and geographies helps mitigate risk and can lead to more consistent returns over the long term.

Considering Alternative Income Streams

Even with a robust pension and investment portfolio, considering alternative income streams can add an extra layer of financial security and flexibility in retirement:

- Part-time Work or Consulting: Many retirees choose to work part-time, either for financial reasons or to stay engaged. This could be in a previous profession on a consultancy basis or pursuing a new, less demanding role.

- Side Hustles: Turning a hobby into a small income-generating venture can be a rewarding way to supplement retirement income.

- Rental Income: If you own additional properties, rental income can provide a steady passive cash flow.

- Equity Release: For homeowners, equity release schemes can provide a lump sum or regular income by unlocking wealth tied up in your home, though this should be considered carefully due to its implications for your estate.

These alternative streams can offer vital flexibility, cover unexpected expenses, or simply provide additional disposable income to enhance your retirement lifestyle.

Essential Steps for Proactive Retirement Planning

Understanding the State Pension age and the various financial vehicles available is only half the battle. The other half involves taking concrete, proactive steps to plan and execute your retirement strategy. This isn’t a one-time task but an ongoing process of assessment and adjustment.

Verify Your State Pension Age

The very first and most crucial step is to accurately determine your specific State Pension age. Do not rely on general figures or assumptions. Use the official UK government website tool by searching “Check your State Pension age.” This will provide you with the definitive age at which you become eligible, based on your date of birth. This figure forms the bedrock of all subsequent retirement calculations and helps you understand your financial timeline.

Conduct a Comprehensive Financial Health Check

Once you know your State Pension age, the next step is to get a clear picture of your current financial standing. This “health check” should include:

- Reviewing Existing Pensions: Gather statements for all workplace and personal pensions you’ve accumulated. Use the government’s Pension Tracing Service if you’ve lost track of old schemes. Understand their current value, how they’re invested, and any associated fees.

- Assessing Savings and Investments: Tally up all your ISAs, general investment accounts, property equity, and any other assets that could contribute to your retirement.

- Evaluating Debts: Understand your current liabilities, such as mortgages, loans, or credit card debt. Ideally, you want to enter retirement debt-free.

- Projecting Retirement Expenses: Create a realistic budget for your retirement. Consider your desired lifestyle, potential travel, hobbies, healthcare costs, and essential living expenses. This projection will help you determine your “retirement income target.”

Seek Professional Financial Guidance

While this article provides a general overview, personal circumstances are unique. For complex situations, significant wealth, or simply peace of mind, seeking advice from a qualified independent financial advisor (IFA) is invaluable. An IFA can:

- Offer tailored advice: Based on your specific income, assets, debts, risk tolerance, and retirement goals.

- Optimise investment strategies: Help you build a diversified portfolio that aligns with your timeline and objectives.

- Navigate tax planning: Advise on tax-efficient ways to save, draw down your pension, and manage your estate.

- Consolidate pensions: Help you manage multiple pension pots and potentially reduce fees.

- Provide peace of mind: Give you confidence that your retirement plan is robust and on track.

Choosing an IFA regulated by the Financial Conduct Authority (FCA) is essential to ensure they adhere to professional standards and consumer protection.

Conclusion

The State Pension age in the UK is a dynamic target, continually adjusted in response to societal and economic shifts. Far from being a static number, its evolution necessitates a proactive and adaptive approach to personal financial planning. Understanding your specific State Pension age, coupled with a robust strategy that maximises private pensions, diversified investments, and considers alternative income streams, is paramount. By taking essential steps like verifying your eligibility, conducting regular financial health checks, and seeking professional guidance, you can build a resilient financial future, ensuring a secure and comfortable retirement despite the ever-changing landscape. Your financial well-being in later life is a journey, not a destination, and careful planning today is the key to unlocking the retirement you desire tomorrow.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.