In the landscape of American financial institutions, few names carry as much weight or evoke as much loyalty as USAA (United Services Automobile Association). However, unlike giants such as State Farm or Geico, USAA is not a provider available to the general public. It occupies a unique niche in the “Money” category, functioning as a specialized financial cooperative designed for a very specific demographic. To understand who USAA insurance is for, one must look beyond the marketing and into the structural, economic, and eligibility frameworks that define the organization.

This article explores the financial intricacies of USAA, detailing who qualifies for membership, the monetary advantages of their insurance products, and how their services integrate into a broader personal finance strategy.

Understanding USAA’s Unique Financial Ecosystem

USAA is not a traditional corporation; it is a reciprocal inter-insurance exchange. This distinction is vital for anyone analyzing it from a personal finance perspective. In a standard insurance model, profit is distributed to shareholders. In a reciprocal exchange, the policyholders are the “members,” and the organization’s financial health directly impacts the benefits provided back to those members.

The Core Mission: Serving the Military Community

Since its founding in 1922 by 25 Army officers who couldn’t find reliable auto insurance due to the perceived risks of military life, USAA has focused on a singular mission: the financial security of the military community. This focus allows USAA to tailor its financial products to the unique lifestyle of service members—such as frequent relocations (PCS), deployments, and the specific transition periods between active duty and civilian life.

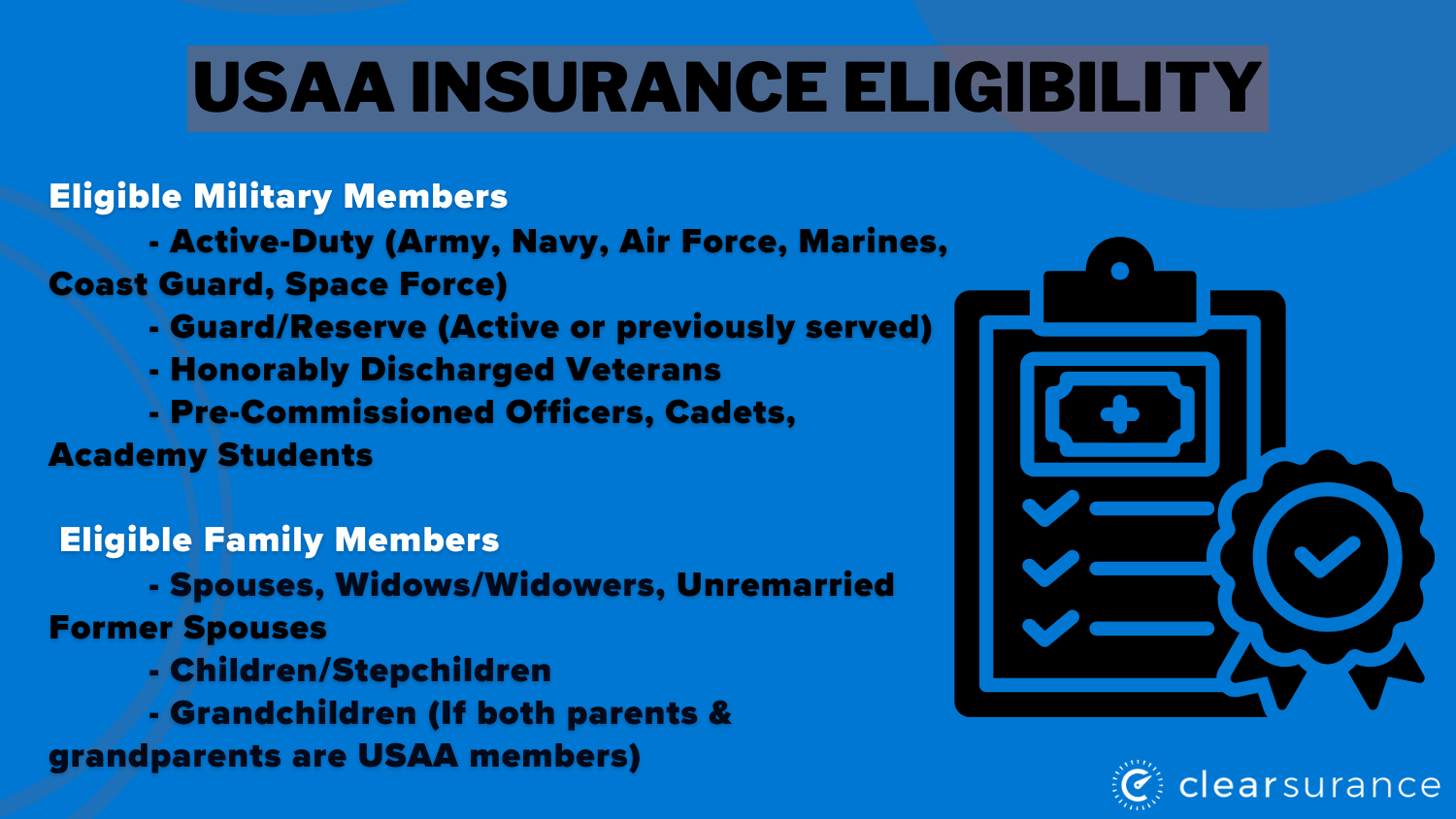

Eligibility Requirements: Who Qualifies?

The question of “who is it for” is strictly governed by eligibility rules. USAA is for:

- Active Duty Military: Members of the U.S. Air Force, Army, Coast Guard, Marine Corps, Navy, and Space Force.

- Veterans: Those who have retired or separated from the U.S. military with a discharge type of Honorable.

- Cadets and Midshipmen: Individuals in U.S. service academies, in ROTC on scholarship, or at officer candidate schools.

- Family Members: Spouses and children of USAA members.

This “hereditary” eligibility is a significant financial asset. Once a parent joins USAA, their children become eligible, creating a multi-generational legacy of financial stability and access to competitive rates.

The Economic Value Proposition of USAA Insurance

When evaluating insurance through a financial lens, the primary metrics are the “Premium vs. Coverage” ratio and the long-term return on investment. USAA consistently ranks at the top of these metrics, often outperforming commercial competitors in both cost and claims satisfaction.

Competitive Pricing and Dividend Distributions

Because USAA does not have to answer to Wall Street shareholders, they can price their premiums closer to the actual cost of risk. For the consumer, this often translates to lower monthly outflows for auto, home, and renters insurance.

Furthermore, a standout feature of the USAA “Money” model is the Subscriber’s Account. When the association performs well financially and maintains adequate reserves, a portion of the capital is returned to members in the form of dividends or allocations to these accounts. For long-term members, these annual distributions can significantly offset the net cost of their insurance, a financial perk rarely found in the standard private sector.

Comprehensive Coverage Options for Diverse Financial Needs

USAA’s insurance suite is designed to protect a member’s entire balance sheet. Their offerings include:

- Property and Casualty (P&C): Highly competitive auto and homeowners’ insurance that includes unique military-specific clauses, such as coverage for uniforms or waived deductibles for certain deployment-related scenarios.

- Valuable Personal Property: High-limit coverage for jewelry, firearms, and electronics, often at lower rates than standalone “floater” policies.

- Umbrella Insurance: A critical tool for wealth protection, providing an extra layer of liability coverage that protects a member’s assets from devastating lawsuits.

Banking and Beyond: Integrating Insurance into Wealth Management

For the savvy individual, insurance is not an isolated expense; it is a component of a comprehensive financial plan. USAA facilitates this by bridging the gap between insurance and banking, creating a “one-stop-shop” that simplifies cash flow management.

Seamless Financial Synergy

By housing insurance, checking, and savings accounts under one roof, USAA members can automate their financial lives. The “Total Cost of Ownership” for their financial services is lowered through bundled discounts. For example, members often receive discounts on their auto insurance simply for having a recurring direct deposit into a USAA bank account or for maintaining a certain balance. From a personal finance standpoint, this reduces the administrative burden and ensures that insurance premiums are always accounted for in the monthly budget.

Long-term Investment and Retirement Planning

Beyond the immediate protection of assets, USAA provides tools for long-term wealth accumulation. While they have transitioned some of their investment arms to partners like Charles Schwab and Victory Capital, the integration remains tight.

- Life Insurance: USAA offers Term and Whole Life policies that are particularly valuable for military families, as they often lack the “war clause” exclusions found in some civilian policies. This ensures that even in high-risk professions, the family’s financial future is secure.

- Annuities and IRAs: Through their partnerships, USAA assists members in transitioning from military pensions (such as the Blended Retirement System) into diversified private portfolios, ensuring that the wealth protected by their insurance is also allowed to grow.

Evaluating the Pros and Cons for the Modern Consumer

While the financial benefits of USAA are substantial, no institution is without its drawbacks. A professional financial analysis requires looking at the limitations as well as the perks.

Customer Service Excellence and Claims Processing

From a “Money” perspective, the value of an insurance policy is zero if the company does not pay out claims efficiently. USAA is legendary for its claims processing. In the event of a total loss (such as a house fire or a major car accident), their speed of reimbursement helps members avoid high-interest debt that often arises during financial emergencies. The high Net Promoter Score (NPS) associated with USAA suggests that members feel their “money’s worth” is realized most during times of crisis.

Limitations and Eligibility Constraints

The most significant “con” of USAA is its exclusivity. For the 93% of the U.S. population with no military connection, the financial benefits of USAA remain out of reach. Additionally, as the organization has grown, some members have noted that the “small-cooperative” feel has shifted toward a more corporate atmosphere.

From a competitive standpoint, while USAA is often the cheapest, it is not always the cheapest for every specific profile. High-risk drivers or individuals with a history of frequent claims may occasionally find better rates with “non-standard” insurers, although they would sacrifice the member-centric benefits and dividends unique to the USAA model.

Conclusion: Is USAA the Right Financial Partner for You?

USAA insurance is for the military-affiliated individual who views insurance not just as a legal requirement, but as a strategic pillar of their financial health. It is for the veteran who wants their years of service to translate into lower living expenses, and for the military spouse who needs a financial institution that understands the complexities of a mobile lifestyle.

If you are eligible, the financial math almost always favors joining. Between the competitive premiums, the unique Subscriber’s Account distributions, and the high-quality claims service, USAA provides a level of “financial peace of mind” that is difficult to quantify but easy to see on a balance sheet.

In the world of personal finance, the goal is to minimize unnecessary expenses while maximizing protection and growth. For the U.S. military community, USAA remains one of the most effective tools available to achieve that balance. By leveraging the power of a collective, disciplined demographic, USAA continues to prove that who an insurance company is for matters just as much as what they sell.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.