Purchasing a home is often the most significant financial decision an individual or family will make. For many, it represents not just a dwelling, but a cornerstone of wealth building and financial stability. However, the path to homeownership can be paved with various financial terms and requirements, one of the most frequently encountered — and often misunderstood — being Private Mortgage Insurance, or PMI. Understanding “what is the PMI percentage” is crucial for anyone navigating the mortgage landscape, as it directly impacts your monthly housing costs and long-term financial planning.

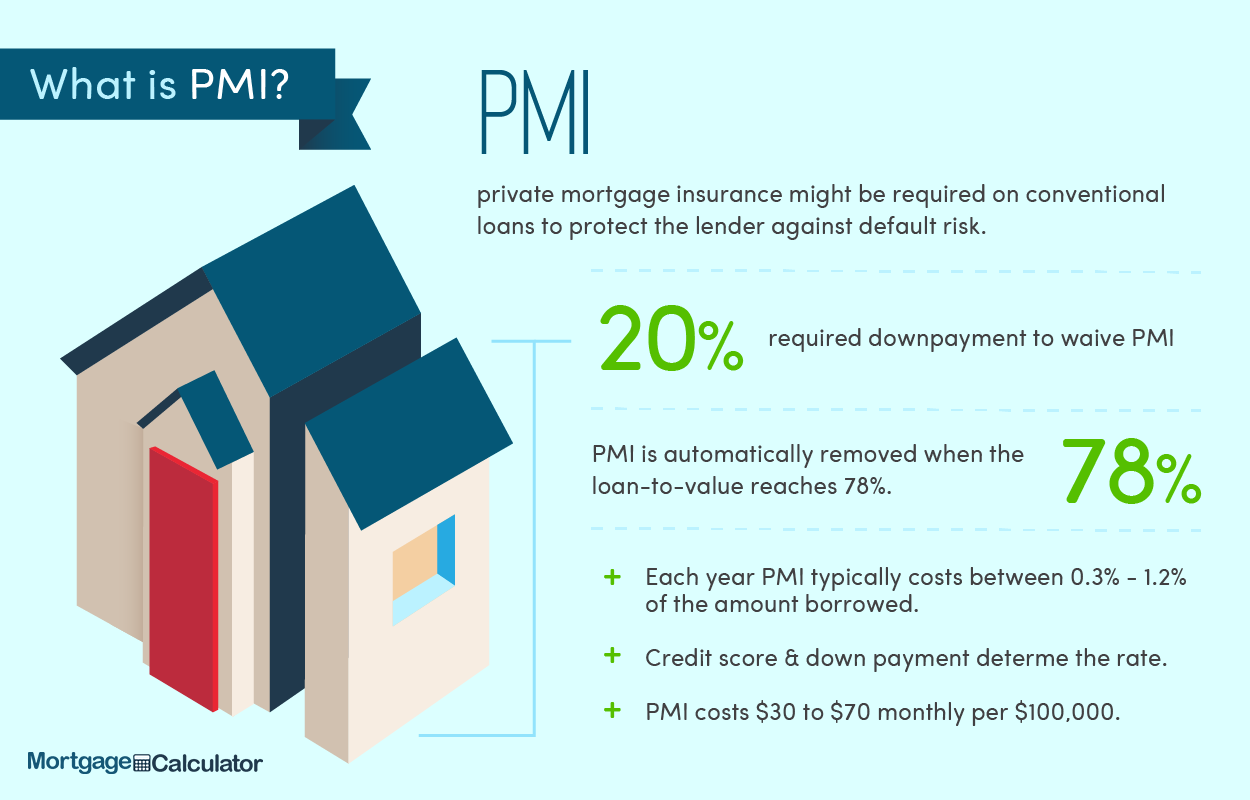

At its core, PMI is a type of insurance policy that protects the mortgage lender, not the homeowner, in the event that the borrower defaults on their loan. While it serves a vital purpose for lenders, it’s an additional cost borne by the borrower, typically when they put down less than 20% of the home’s purchase price. The “PMI percentage” refers to the rate at which this insurance premium is calculated, determining how much extra you’ll pay each month on top of your principal, interest, taxes, and homeowner’s insurance. This article will demystify PMI, explain how its percentage is determined, analyze its impact, and outline strategies to minimize or eliminate this additional expense, empowering you with the knowledge to make informed financial decisions on your journey to homeownership.

Demystifying Private Mortgage Insurance (PMI)

Private Mortgage Insurance is a critical component of the mortgage industry, enabling more individuals to achieve homeownership even if they don’t have a substantial down payment saved. While it can feel like an unwelcome extra cost, understanding its underlying purpose and mechanics is the first step toward managing it effectively.

The Core Purpose of PMI

The primary function of PMI is to mitigate risk for mortgage lenders. When a borrower puts down less than 20% of a home’s value, the loan-to-value (LTV) ratio is higher, making the loan inherently riskier for the lender. Should the borrower default on their mortgage payments and the home goes into foreclosure, the lender faces the possibility of not recouping the full outstanding loan amount if the property’s sale price doesn’t cover it. PMI acts as a safety net, compensating the lender for a portion of their loss in such scenarios. It essentially makes higher-LTV loans palatable for financial institutions, broadening access to credit for a larger segment of the population. Without PMI, lenders would likely require larger down payments, thereby making homeownership less accessible for many first-time buyers or those with limited savings.

When PMI Becomes a Requirement

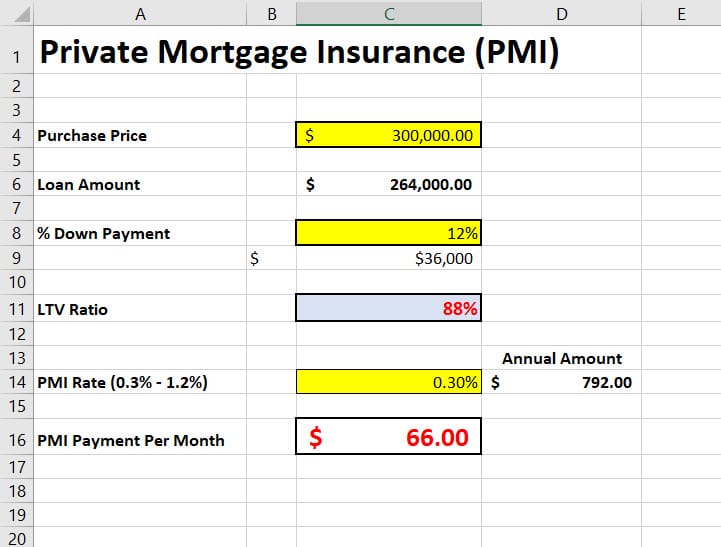

The most common trigger for PMI is a down payment that is less than 20% of the home’s purchase price. For instance, if you’re buying a $300,000 home and only put down $30,000 (10%), your loan-to-value ratio is 90% ($270,000 / $300,000). Because this LTV is above the 80% threshold, PMI will almost certainly be required by your lender. It’s important to note that this 20% threshold is a widely accepted industry standard, stemming from historical data indicating a higher probability of default on loans with lower equity stakes from the borrower. While 20% is the benchmark, some specific loan products or niche lenders might have slightly different requirements, but these are exceptions rather than the norm.

Who Benefits (and Who Pays)?

This is a crucial distinction. While the lender is the direct beneficiary of PMI coverage, the borrower is solely responsible for paying the premiums. This can be a source of frustration for homeowners, as they are paying for a service that protects someone else’s financial interests. However, from the lender’s perspective, the borrower is taking on a higher-risk loan, and the PMI premium is the cost of that additional risk, making the loan viable. Understanding this dynamic helps frame PMI not as an arbitrary fee, but as an integral part of the financial structure that enables a low-down-payment mortgage. It’s a trade-off: in exchange for a smaller upfront investment, you pay an ongoing insurance premium.

Understanding the PMI Percentage: Calculation and Impact

The “PMI percentage” is not a fixed number; it’s a variable rate determined by a combination of factors. This percentage is critical because it directly influences your monthly mortgage payment and, consequently, your overall budget.

Factors Influencing Your PMI Rate

Several key factors play into how your specific PMI percentage is determined:

- Loan-to-Value (LTV) Ratio: This is arguably the most significant factor. The higher your LTV (i.e., the smaller your down payment), the higher the perceived risk for the lender, and thus the higher your PMI percentage will likely be. For example, a 5% down payment (95% LTV) will typically incur a higher PMI rate than a 15% down payment (85% LTV).

- Credit Score: Your credit score is a direct reflection of your financial reliability. Borrowers with excellent credit scores demonstrate a lower risk of default and will generally qualify for lower PMI percentages compared to those with lower scores. Lenders and PMI providers use credit scores as a primary indicator of a borrower’s ability to manage debt responsibly.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to cover your mortgage payments, making you a less risky borrower and potentially qualifying you for a lower PMI rate.

- Loan Term and Type: The length of your mortgage (e.g., 15-year vs. 30-year) can influence your PMI rate, with shorter terms sometimes leading to slightly lower rates due to less exposure for the insurer. Fixed-rate versus adjustable-rate mortgages can also play a role, though typically a less dominant one than LTV and credit score.

- Property Type: While less common, the type of property (e.g., single-family home vs. multi-unit dwelling) can sometimes marginally affect the risk assessment and, by extension, the PMI rate.

How PMI is Calculated and Applied

The PMI percentage is generally applied to the original loan amount on an annual basis. For example, if your PMI percentage is 0.5% and your original loan amount is $270,000, your annual PMI premium would be $1,350 (0.005 * $270,000). This annual amount is then divided by 12 and added to your monthly mortgage payment. So, in this example, you’d pay an additional $112.50 per month.

It’s crucial to understand that while the percentage is applied to the original loan amount, the equity you build over time helps you eventually eliminate PMI, even though the calculation basis doesn’t change monthly. The percentage itself is usually fixed for the life of the PMI coverage, but the duration of payments depends on your equity growth.

The Real Cost: Monthly vs. Upfront PMI

While most commonly paid monthly, PMI can also be structured in other ways, each with its own financial implications:

- Borrower-Paid PMI (BPMI): This is the most common form, where the premium is included in your monthly mortgage payment. It offers flexibility as it can be canceled once sufficient equity is achieved.

- Lender-Paid PMI (LPMI): In this scenario, the lender pays for the PMI premium upfront, but in exchange, they typically charge a slightly higher interest rate on the loan. While this means no separate monthly PMI payment, the higher interest rate lasts for the life of the loan and generally cannot be canceled. This makes LPMI less flexible and potentially more expensive over the long term, as you’re effectively paying for the PMI through increased interest for the entire mortgage term, even after you’ve built significant equity.

- Single-Premium PMI: Here, the entire PMI premium is paid as a one-time lump sum at closing. This can either be paid out of pocket or financed into the loan. If financed, it increases your loan amount and thus your total interest paid. The advantage is no ongoing monthly PMI payments, but the downside is the large upfront cost or increased debt.

- Split-Premium PMI: This is a hybrid approach where a portion of the PMI is paid upfront at closing, and the remaining balance is paid through lower monthly premiums.

Each option has trade-offs, and the best choice depends on your specific financial situation, cash flow, and long-term goals. It’s vital to discuss these options with your lender and compare the total cost over the expected life of the loan.

Strategies to Avoid or Eliminate PMI

While PMI is often a necessary component for many homebuyers, it’s also a temporary one that most homeowners strive to eliminate. Proactive planning can help you either avoid it from the outset or get rid of it as quickly as possible, freeing up hundreds of dollars in your monthly budget.

The 20% Down Payment Advantage

The most straightforward way to avoid PMI altogether is to make a down payment of 20% or more of the home’s purchase price. This immediately brings your LTV ratio to 80% or below, eliminating the lender’s requirement for PMI. While saving a 20% down payment can be a significant challenge, especially in competitive housing markets, the long-term savings from avoiding PMI — not to mention lower overall interest costs due to a smaller loan amount — are substantial. For a $300,000 home, a 20% down payment means $60,000 upfront. If this is achievable, it’s almost always the most financially prudent path.

Refinancing Your Mortgage

If you initially purchased your home with less than a 20% down payment and are now paying PMI, refinancing your mortgage can be an effective strategy to eliminate it. As your home’s value appreciates and you pay down your loan principal, your equity stake naturally increases. When your equity reaches 20% or more of your current home value, you might be able to refinance into a new loan that doesn’t require PMI. This strategy is particularly effective when interest rates are favorable, allowing you to potentially secure a lower rate alongside PMI elimination. However, refinancing comes with closing costs, so it’s essential to calculate whether the savings from eliminating PMI and potentially lowering your interest rate outweigh these upfront expenses.

Requesting PMI Cancellation

The Homeowners Protection Act (HPA) of 1998 provides specific rights regarding PMI cancellation for conventional loans. You have the right to request PMI cancellation when your loan-to-value (LTV) ratio reaches 80% based on the original appraised value or the original purchase price of your home, whichever is less. To do this, you typically need:

- A good payment history (no 30-day late payments in the last year, no 60-day late payments in the last two years).

- No subordinate liens (like a second mortgage or home equity line of credit).

- Your lender may require an appraisal to confirm the property’s value has not decreased.

This method relies on proactive engagement with your loan servicer. Keep track of your principal balance and compare it to your home’s original value.

Automatic PMI Termination

Beyond your right to request cancellation, the HPA also mandates automatic PMI termination under specific conditions:

- Automatic Termination: Your loan servicer must automatically terminate PMI when your mortgage balance is scheduled to reach 78% of the original value of your home, based on your original amortization schedule. This happens even if you haven’t made any extra payments.

- Final Termination: Regardless of your payment history or the original schedule, PMI must be terminated when you reach the midpoint of your loan’s amortization period (e.g., after 15 years on a 30-year mortgage), provided you are current on your payments.

These automatic termination points provide a safety net, ensuring that PMI doesn’t linger indefinitely. However, note that these thresholds are based on the original value, meaning property appreciation doesn’t accelerate automatic termination, though it can help with a borrower-initiated request for cancellation or a refinance.

The Financial Implications and Long-Term Outlook

While PMI is a temporary cost, its presence can significantly impact your immediate budget and long-term financial trajectory. Understanding these implications is key to making strategic decisions about your homeownership journey.

Budgeting for PMI: A Necessary Consideration

For many homeowners, especially those making a low down payment, PMI adds a tangible amount to their monthly housing expenses. This additional cost can range from 0.3% to 1.5% of the original loan amount annually, which, for a $250,000 loan, could mean anywhere from $62.50 to $312.50 per month. These figures might seem small individually, but they add up. When budgeting for a home, it’s crucial to factor in not just the principal and interest, but also property taxes, homeowner’s insurance, and PMI. Overlooking PMI can lead to an underestimation of your true monthly housing burden, potentially stretching your budget thinner than anticipated or limiting your eligibility for a higher loan amount. Accurate budgeting ensures that you can comfortably afford your home and meet all your financial obligations.

The Opportunity Cost of PMI

Every dollar spent on PMI is a dollar that could have been used elsewhere. This is known as opportunity cost. Instead of protecting a lender, that money could have gone towards:

- Building Equity Faster: Extra principal payments could accelerate your loan repayment, reducing the amount of interest paid over the life of the loan and reaching the PMI cancellation threshold sooner.

- Savings and Investments: These funds could be allocated to an emergency fund, a retirement account, or other investment vehicles, allowing your money to grow over time.

- Home Improvements: Investing in your home can increase its value and improve your living situation.

- Debt Reduction: Paying down other high-interest debts, such as credit card balances, could significantly improve your overall financial health.

While PMI enables homeownership, recognizing its opportunity cost encourages homeowners to strategically work towards its elimination to reallocate those funds more productively within their personal finance ecosystem.

Strategic Homeownership and Wealth Building

The goal of eliminating PMI should be viewed as part of a broader strategy for building wealth through homeownership. By actively working to cancel PMI, you are not only reducing your monthly expenses but also increasing your monthly cash flow, which can then be redirected towards accelerating your equity growth or enhancing other financial goals.

Consider the long-term impact: a 30-year mortgage with PMI for the first 5-7 years means you’re paying a significant amount over time. By aggressively paying down your principal or strategically refinancing, you shorten this period, effectively creating more “free” money each month. This disciplined approach to managing your mortgage—understanding all its components, including the PMI percentage—empowers you to maximize the financial benefits of homeownership, turning your primary residence into a powerful asset for long-term financial security rather than just a liability.

Conclusion

Understanding “what is the PMI percentage” is far more than just knowing a number; it’s about comprehending a fundamental aspect of modern home financing that impacts millions of homeowners. Private Mortgage Insurance serves as a bridge to homeownership for those with smaller down payments, protecting lenders while placing an additional cost burden on borrowers.

The PMI percentage itself is a dynamic figure, influenced by factors such as your loan-to-value ratio, credit score, and debt-to-income ratio. It directly translates into a monthly expense that necessitates careful budgeting and awareness. While it’s often an unavoidable initial cost, it is also a temporary one. By strategically employing tactics such as making a larger down payment, refinancing when advantageous, or proactively requesting its cancellation, homeowners can significantly reduce or eliminate this expense.

Ultimately, navigating PMI effectively is a critical step in prudent personal finance and successful homeownership. By staying informed, actively managing your mortgage, and working towards its elimination, you can optimize your housing costs, free up valuable capital, and accelerate your journey toward financial independence and robust wealth building through your most significant asset: your home.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.