Filing an income tax return is often viewed as a daunting annual chore, a complex maze of numbers and legal jargon that many approach with trepidation. However, in the realm of personal finance and money management, tax filing is one of the most critical events of the fiscal year. It is not merely a legal obligation; it is an opportunity to audit your financial health, optimize your cash flow, and ensure that you are retaining as much of your hard-earned wealth as possible. Understanding the mechanics of how to file an income tax return empowers you to transition from a passive participant in the economy to a proactive manager of your personal capital.

This guide provides a comprehensive roadmap for navigating the tax filing process, designed for individuals looking to sharpen their financial literacy and maximize their fiscal efficiency.

1. Understanding the Fundamentals of Income Tax Filing

Before diving into forms and spreadsheets, it is essential to understand what tax filing actually represents. At its core, an income tax return is a report filed with a government entity (such as the IRS in the United States) that declares your earnings, expenses, and other pertinent financial information for a specific calendar year.

Identifying Your Filing Status and Tax Bracket

The first step in a strategic approach to filing is identifying your filing status. Whether you are filing as Single, Married Filing Jointly, or Head of Household, your status dictates your standard deduction and the tax brackets that apply to your income. In a progressive tax system, your income is taxed at different rates as it crosses specific thresholds. Understanding where your “last dollar” sits—your marginal tax rate—is vital for making informed investment and savings decisions throughout the year.

The Distinction Between Gross, Adjusted, and Taxable Income

To file correctly, you must distinguish between your types of income. Your Gross Income includes everything from wages and bonuses to dividends and rental income. Your Adjusted Gross Income (AGI) is calculated by taking your gross income and subtracting specific “above-the-line” adjustments, such as student loan interest or contributions to a traditional IRA. Finally, your Taxable Income is what remains after you apply either the standard deduction or itemized deductions. This final figure is what the government actually uses to calculate your tax liability.

2. Navigating the Filing Process: A Step-by-Step Blueprint

Effective money management requires organization. Filing your taxes is significantly easier when you have a systematic process for gathering data and submitting your documentation.

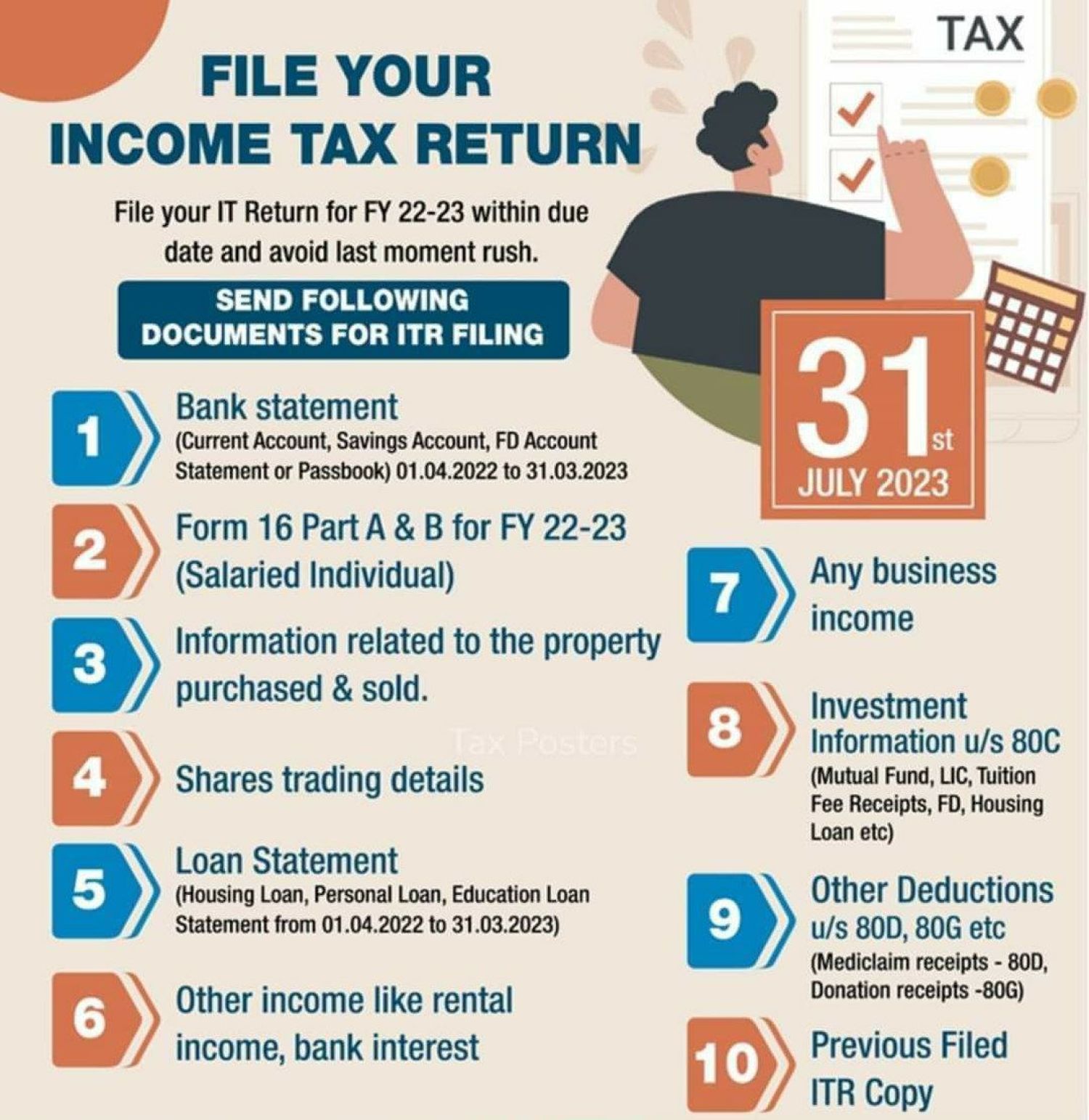

The Essential Documentation Checklist

Successful filing begins long before you open tax software. You must aggregate all forms of documentation that prove your income and justify your deductions. For most employees, this starts with the W-2 form. For freelancers and those with side hustles, 1099-NEC or 1099-K forms are the standard. Beyond income, you need records of “money out” that might be tax-advantaged, such as mortgage interest statements (Form 1098), records of charitable contributions, and receipts for business-related expenses.

Choosing Between Standard Deduction and Itemizing

One of the most pivotal decisions in the filing process is deciding whether to take the standard deduction or to itemize. The standard deduction is a fixed dollar amount that reduces the income on which you’re taxed. Itemizing, on the other hand, allows you to list specific expenses—such as medical bills, state and local taxes (SALT), and home mortgage interest. From a personal finance perspective, the rule is simple: calculate both and choose the one that results in the lowest tax liability. For many, the increased standard deduction introduced in recent years makes itemizing less common, but for high-income earners or those with significant deductible expenses, itemizing remains a powerful tool for wealth preservation.

The Logistics of E-Filing vs. Manual Submission

In the modern financial landscape, electronic filing (e-filing) has become the gold standard. E-filing is not only faster, but it also reduces the margin for mathematical error significantly compared to paper returns. When you e-file and opt for direct deposit, your tax refund—if you are owed one—is processed much faster, allowing you to put that money back into your savings or investment vehicles sooner.

3. Maximizing Your Return through Credits and Deductions

The difference between an average taxpayer and a savvy financial manager lies in the ability to identify and claim every available tax break. Credits and deductions are the primary tools used to lower your effective tax rate.

Leveraging Tax Deductions to Lower Taxable Income

Deductions are “subtractions” from your income. For individuals focused on building wealth, deductions like contributions to a 401(k) or a Health Savings Account (HSA) are dual-purpose: they reduce your current tax bill while simultaneously building your future net worth. If you are self-employed, you can deduct a portion of your home office, equipment, and even half of your self-employment tax. These deductions are essential for maintaining the profitability of a business or side hustle.

Utilizing Tax Credits for Dollar-for-Dollar Savings

While deductions lower the amount of income you are taxed on, tax credits are even more valuable because they reduce your actual tax bill dollar-for-dollar. For example, if you owe $5,000 in taxes and qualify for a $2,000 credit, your bill drops directly to $3,000. Common credits include the Child Tax Credit, the Earned Income Tax Credit (EITC) for low-to-moderate-income earners, and various education credits like the American Opportunity Tax Credit (AOTC). Understanding which credits apply to your life stage can save you thousands of dollars.

4. Digital Tools and Professional Resources for Tax Management

In the age of fintech, you do not have to navigate the complexities of tax law alone. There are numerous tools and professional services designed to streamline the filing process and ensure accuracy.

Selecting the Right Financial Software

Tax preparation software has democratized the filing process. These platforms use interview-style interfaces to guide you through your financial year, flagging potential deductions you might have missed. For individuals with simple financial lives, many of these tools offer free filing. For those with complex portfolios—including crypto assets, rental properties, or foreign investments—premium versions of these tools provide the necessary forms and guidance to ensure compliance.

When to Consult a Certified Public Accountant (CPA)

While software is powerful, it is not a replacement for professional advice in complex financial situations. If you own a corporation, have a high net worth, or are dealing with complex estate issues, hiring a CPA or a tax attorney is a wise investment. A professional can provide year-round tax planning, helping you structure your finances in a way that minimizes liability long before the filing deadline arrives. In the world of money management, the fee paid to a tax professional is often dwarfed by the savings they generate through expert planning.

5. Avoiding Common Pitfalls and Planning for the Future

The filing process does not end the moment you hit “submit.” A disciplined approach to finance involves post-filing review and future preparation.

Avoiding Audits and Ensuring Accuracy

Mathematical errors, mismatched names or Social Security numbers, and failing to report all sources of income are “red flags” that can trigger an audit. While audits are rare, they are time-consuming and potentially costly. Ensuring that your return perfectly matches the information reported to the government by your employer and financial institutions is the best way to maintain a low profile and avoid legal complications.

Strategic Planning for the Next Fiscal Year

The best time to prepare for next year’s tax return is immediately after you file the current one. Use your completed return as a diagnostic tool. Did you receive a massive refund? If so, you essentially gave the government an interest-free loan; you might consider adjusting your withholding to keep more money in your monthly paycheck for investing. Conversely, if you owed a large sum, you may need to increase your withholdings or make quarterly estimated payments to avoid penalties.

Mastering the art of filing an income tax return is a cornerstone of robust personal finance. By understanding the terminology, staying organized, maximizing credits, and using the right tools, you transform a mundane requirement into a strategic advantage. Taxes are one of life’s few certainties, but with the right approach, they do not have to be a source of financial stress. Instead, they can be a clear, annual indicator of your journey toward financial independence and wealth optimization.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.