In the intricate tapestry of personal finance, a living will often emerges as a less discussed but profoundly impactful document. Far more than just a medical directive, a living will is a cornerstone of proactive financial planning, designed to protect an individual’s autonomy, manage potential healthcare costs, and alleviate significant financial and emotional burdens on their loved ones during critical times. Understanding its nature, purpose, and integration into a holistic financial strategy is essential for anyone looking to secure their future and provide clear guidance for their care.

The concept of a “living will” can sometimes be confused with other estate planning documents, yet its distinct role makes it indispensable. It’s a proactive step, taken while an individual is of sound mind, to dictate preferences for medical treatment should they become incapacitated and unable to communicate those wishes themselves. From a financial perspective, this document is not merely about personal desires; it’s about preventing protracted legal battles, controlling potential healthcare expenditures, and ensuring that an individual’s resources are managed according to their expressed intent, rather than being drained by unwanted or prolonged medical interventions.

The Core Purpose of a Living Will in Personal Finance

At its heart, a living will serves as an individual’s voice when they can no longer speak for themselves. This fundamental purpose extends deeply into personal finance, safeguarding assets and minimizing potential financial distress for families.

Defining a Living Will: Beyond Just Medical Directives

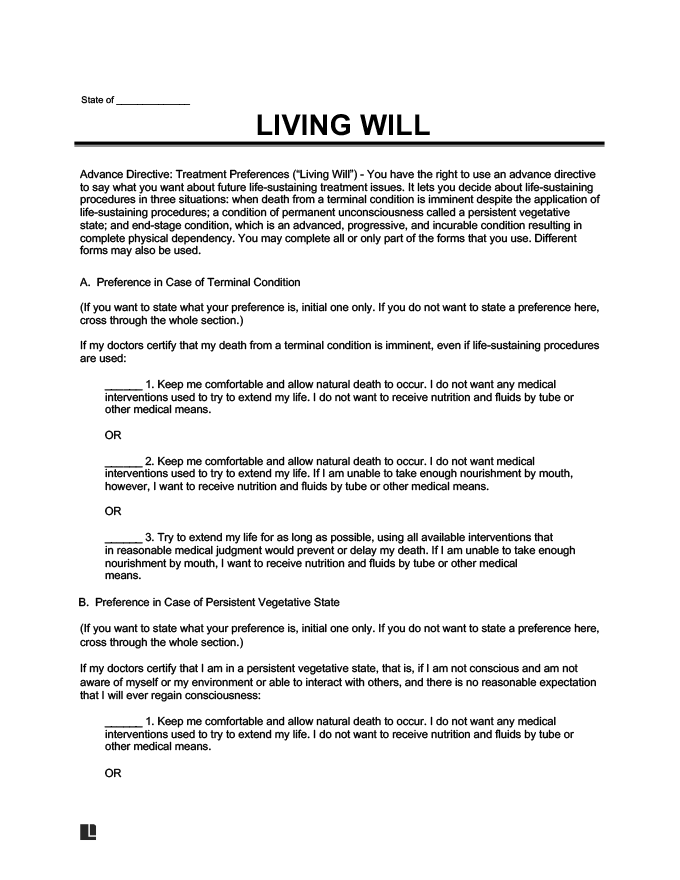

A living will, legally known as an Advance Directive for Healthcare, is a written legal document that outlines your preferences for medical care in specific circumstances, particularly at the end of life or if you suffer from a debilitating injury or illness that leaves you unable to make decisions. It typically addresses scenarios such as life support, artificial nutrition and hydration, pain management, and other medical interventions. While seemingly purely medical, the decisions within a living will have direct financial consequences. For instance, choosing to forgo aggressive treatments in certain situations can prevent prolonged hospital stays and extensive medical bills that could otherwise deplete an estate or place a significant financial strain on family members responsible for healthcare costs. It’s a powerful tool for self-determination that also provides a financial safety net.

Empowering Personal Autonomy and Preventing Financial Strain

The primary benefit of a living will is the preservation of personal autonomy. It ensures that your medical wishes are honored, even if you are unconscious or otherwise incapacitated. From a financial standpoint, this translates into avoiding treatments you wouldn’t want, thereby preventing unnecessary medical expenses. Without a living will, difficult decisions often fall to family members, who may face agonizing choices without clear guidance, potentially leading to disagreements and expensive legal challenges to determine a course of action. These legal fees, coupled with the costs of potentially unwanted or prolonged medical care, can quickly erode savings, investments, and other assets intended for beneficiaries or other financial goals. By clearly stating your preferences, you preempt these costly and emotionally draining scenarios, effectively safeguarding your financial legacy and reducing potential financial strain on your loved ones.

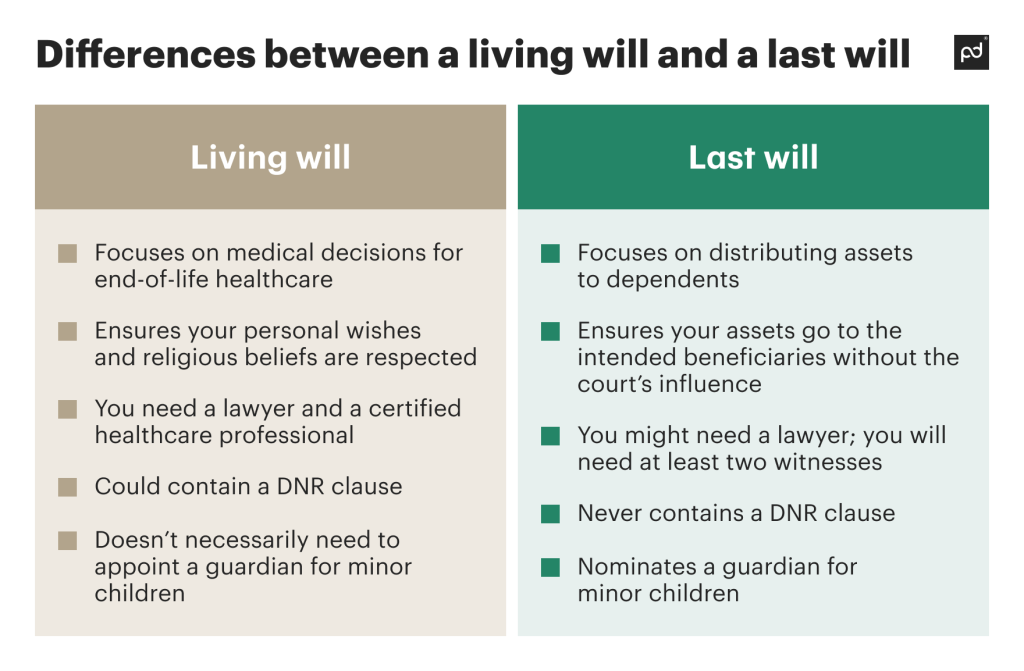

Distinguishing from a Last Will and Testament

It is crucial to differentiate a living will from a Last Will and Testament. While both are critical estate planning documents, they serve distinct purposes. A Last Will and Testament dictates how your assets will be distributed after your death and names guardians for minor children. It is primarily concerned with your estate’s financial distribution post-mortem. A living will, conversely, comes into effect while you are still alive but incapacitated. It pertains to your medical care and end-of-life decisions, essentially guiding healthcare professionals and your designated healthcare proxy in managing your treatment. Both documents are essential for a complete financial and estate plan, working in tandem to ensure your wishes regarding both your person and your property are respected and executed efficiently.

The Financial and Familial Implications of Not Having a Living Will

The absence of a living will can have profound and often devastating financial consequences, extending beyond mere medical bills to affect family dynamics and long-term financial stability.

Potential for Costly Legal Battles and Probate Issues

Without a living will, if you become incapacitated, there may be no clear legal directive for your medical care. This vacuum can force family members to seek court intervention to appoint a guardian or conservator to make healthcare decisions on your behalf. These legal proceedings are not only emotionally taxing but also financially burdensome, incurring significant attorney fees, court costs, and administrative expenses. Such expenses can quickly deplete an individual’s assets, impacting their estate and the inheritance intended for beneficiaries. Moreover, disagreements among family members regarding appropriate medical care can exacerbate these legal costs, drawing out the process and creating lasting rifts, all while financial resources are diverted from beneficial uses to legal battles.

Burden on Family Members: Emotional and Financial Toll

Beyond the direct legal costs, the absence of a living will places an immense emotional and financial burden on family members. They are forced to make excruciating decisions about life and death, often under immense stress, grief, and uncertainty, without the guiding light of your expressed wishes. This can lead to guilt, conflict, and prolonged emotional distress. Financially, family members may also incur unexpected travel expenses, lost wages due to time off work, and direct healthcare costs if they are legally responsible or feel compelled to contribute. The ambiguity can lead to treatments being pursued longer than necessary or desired, escalating bills that then fall to the family or the estate, creating an unforeseen financial obligation that could have been mitigated with clear directives.

Unintended Financial Consequences of Prolonged Care

In situations where there is no living will, medical professionals and family members, erring on the side of caution or driven by hope, might opt for aggressive, prolonged life-sustaining treatments. While this approach is understandable from an emotional perspective, it can have dire financial consequences. Extended stays in intensive care units, reliance on advanced medical technology, and continuous specialized care accumulate massive bills that can quickly exhaust private insurance limits, Medicare/Medicaid benefits, and personal savings. This can lead to a rapid depletion of an individual’s financial resources, leaving little or nothing for their family or other financial goals. In extreme cases, it can even force families into debt or financial hardship to cover these unforeseen costs, a scenario that a thoughtfully prepared living will is designed to prevent.

Key Components and Considerations for Your Living Will

Crafting an effective living will requires careful consideration of various medical and legal aspects, all of which have underlying financial implications.

Specifying Medical Treatments and Interventions

A comprehensive living will clearly specifies your wishes regarding various medical treatments and interventions. This typically includes decisions about:

- Life support: Do you want mechanical ventilation, CPR, or other life-sustaining measures?

- Artificial nutrition and hydration: Do you want to receive food and water through tubes if you can’t eat or drink on your own?

- Pain management: Your preferences for pain relief, even if it means sedation that could hasten death.

- Antibiotics: Your stance on receiving antibiotics for life-threatening infections.

- Organ donation: Your decision regarding donating organs or tissues.

Each of these decisions can impact the duration and intensity of medical care, and consequently, the associated costs. For instance, electing to forgo certain aggressive treatments under specific conditions can significantly reduce long-term medical expenditures, preserving assets that might otherwise be consumed by prolonged, technology-intensive care. This detailed specification ensures your financial resources align with your personal values.

Appointing a Healthcare Proxy (Durable Power of Attorney for Healthcare)

An integral part of most advance directives is the appointment of a healthcare proxy, also known as a Durable Power of Attorney for Healthcare. This legal document designates a trusted individual (your agent or proxy) to make medical decisions on your behalf if you become unable to do so. This person should be someone who understands your values and is willing and able to advocate for your wishes, even if those decisions are difficult. From a financial perspective, appointing a proxy is critical because they can ensure that your financial directives regarding healthcare costs are adhered to. They can liaise with medical billing departments, insurance providers, and financial advisors, making decisions that are not only medically appropriate but also financially responsible according to your pre-stated preferences. Without a designated proxy, medical institutions might make default decisions that could have significant and unintended financial ramifications.

State-Specific Requirements and Legal Nuances

The legal requirements for a living will vary significantly by state. These variations can include specific language requirements, witness mandates (e.g., how many witnesses are needed, and if they can be beneficiaries or healthcare providers), and notarization rules. For instance, some states have specific statutory forms for advance directives, while others allow for more personalized documents. It is crucial to adhere to your state’s specific regulations to ensure the document is legally binding and enforceable. Failure to comply can render your living will invalid, leading to the very financial and emotional burdens it was designed to prevent. Consulting with an attorney specializing in estate planning is highly recommended to ensure your living will is properly drafted, executed, and compliant with all applicable laws, thereby securing its financial and medical efficacy.

Integrating a Living Will into a Comprehensive Financial Plan

A living will is not a standalone document but a vital component that interlocks with other elements of a robust financial plan, contributing to overall financial security and peace of mind.

A Pillar of Estate Planning: Beyond Just Asset Distribution

While often overshadowed by discussions of wills and trusts focused on asset distribution, a living will is a fundamental pillar of comprehensive estate planning. Estate planning is about managing your affairs—both personal and financial—during your lifetime and after your death. A living will fits squarely into the “during your lifetime” aspect, particularly concerning incapacity. By clearly articulating your healthcare wishes, you directly influence the financial trajectory of your estate. Minimizing unnecessary medical expenses due to prolonged or unwanted care preserves your assets for your beneficiaries, fulfilling the core objective of many estate plans. It ensures that the wealth you’ve accumulated is managed according to your values, rather than being consumed by medical costs in scenarios you would have preferred to avoid.

Synergy with Other Financial Documents (e.g., Powers of Attorney, Trusts)

For maximum effectiveness, a living will should work in synergy with other essential financial and legal documents. A Durable Power of Attorney for Finances, for instance, designates someone to manage your financial affairs (paying bills, managing investments) if you become incapacitated, complementing your healthcare proxy’s role in medical decision-making. If you have a Trust, the living will ensures that medical decisions align with the financial directives within the trust, preventing scenarios where medical costs might unexpectedly deplete trust assets. Integrating these documents ensures a seamless transition of decision-making authority across both medical and financial domains, preventing gaps or conflicts that could lead to financial distress or legal complications. A holistic approach guarantees that your entire financial and personal care strategy is coherent and protected.

Regular Review and Updates: A Dynamic Financial Tool

Life circumstances, medical advancements, personal wishes, and state laws are subject to change. Therefore, a living will should not be treated as a static document. It is a dynamic financial tool that requires periodic review and updates. Major life events such as marriage, divorce, the birth of children, the death of a designated proxy, or a significant change in health status warrant a review. Similarly, advancements in medical technology or changes in state healthcare laws might necessitate revisions to ensure your document remains relevant, legally sound, and reflective of your current wishes. Financial planners often recommend reviewing all estate planning documents, including your living will, every 3-5 years, or whenever a significant life event occurs, to ensure it continues to serve its protective financial and medical purpose effectively.

Practical Steps to Create and Secure Your Living Will

Establishing a living will is a straightforward process, yet it requires careful attention to detail and professional guidance to ensure its validity and effectiveness.

Consulting with Legal and Financial Professionals

The first and most crucial step in creating a living will is to consult with qualified legal and financial professionals. An estate planning attorney can guide you through the complexities of state-specific laws, help you articulate your medical preferences clearly and legally, and ensure the document is properly executed (witnessed, notarized, etc.). They can also explain the interplay between your living will and other estate planning documents. A financial advisor can help you understand the potential financial impact of your healthcare decisions, integrate your living will into your broader financial plan, and assess how it aligns with your long-term wealth preservation and distribution goals. Their combined expertise ensures that your living will is not only medically sound but also financially astute.

Digital vs. Physical Storage: Ensuring Accessibility

Once created, it is vital to store your living will securely and ensure it is easily accessible when needed. While physical copies are traditional, storing digital copies in secure, encrypted cloud services or digital vaults can enhance accessibility for your healthcare proxy and medical providers. However, ensure that digital access protocols are clear and that your proxy knows how to retrieve it. Key considerations include:

- Providing copies to your healthcare proxy: Your proxy must have an original or certified copy.

- Informing your primary care physician: Ensure your doctor has a copy and it’s part of your medical record.

- Keeping a copy at home: In an easily identifiable location.

- Using a medical alert wallet card: Some services provide cards indicating you have an advance directive and where it can be accessed.

The financial benefit here is immediate access, which can prevent delays in care or unnecessary medical interventions, thereby averting potentially significant and unwanted costs.

Communicating Your Wishes to Loved Ones

Finally, simply creating a living will is not enough; open communication with your loved ones is paramount. Discuss your wishes with your healthcare proxy and other close family members. Explain the decisions you’ve made and the reasons behind them. This conversation can be difficult, but it significantly reduces the emotional burden on your family, fosters understanding, and minimizes the potential for conflict or disagreement during a crisis. Financially, clear communication ensures that everyone understands the implications of your choices on your estate and healthcare expenses, helping them to respect your directives and avoid actions that might incur costs contrary to your wishes. This transparency is invaluable in preserving family harmony and financial integrity.

A living will is an indispensable instrument in the modern landscape of personal finance and estate planning. It empowers individuals to maintain control over their healthcare decisions, safeguard their financial assets from unforeseen medical expenses, and provide invaluable clarity to their loved ones during challenging times. By proactively engaging with this critical document, individuals not only protect their personal autonomy but also solidify their financial legacy, ensuring peace of mind for themselves and their families.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.