Taxation is arguably the single largest recurring expense for most working professionals and business owners. While paying taxes is a legal obligation and a contribution to the infrastructure of society, the tax code itself is written with various incentives designed to encourage specific economic behaviors, such as saving for retirement, investing in businesses, or engaging in philanthropy. Reducing your income tax liability is not about evasion; it is about tax avoidance—the legal process of organizing your financial affairs to minimize the amount of tax you owe.

By taking a proactive, year-round approach to your finances, you can significantly lower your effective tax rate. This guide explores the most effective strategies for reducing income tax, ranging from retirement planning and investment management to business-related deductions and strategic credits.

1. Maximizing Contributions to Tax-Advantaged Retirement Accounts

One of the most direct and effective ways to reduce your taxable income is by utilizing retirement accounts. The internal revenue code provides substantial benefits to those who prioritize long-term savings, effectively “hiding” a portion of your income from the tax collector in the short term.

The Power of Employer-Sponsored Plans (401(k) and 403(b))

For many employees, the 401(k) or 403(b) plan is the cornerstone of tax reduction. Contributions made to a traditional employer-sponsored plan are “pre-tax,” meaning the money is taken out of your paycheck before federal and state income taxes are calculated. For example, if you earn $100,000 and contribute $20,000 to your 401(k), the government only sees $80,000 of taxable income. This not only lowers your immediate tax bill but can also potentially drop you into a lower tax bracket. Furthermore, these funds grow tax-deferred, meaning you do not pay taxes on interest, dividends, or capital gains until you withdraw the money in retirement.

Individual Retirement Accounts (IRAs): Traditional vs. Roth

If you do not have access to an employer plan, or if you want to save beyond what your employer offers, Traditional IRAs offer a similar tax-deduction benefit, provided you meet certain income requirements. The contribution is deducted from your gross income, reducing your tax liability for the year. Conversely, while a Roth IRA does not provide an immediate tax break—contributions are made with after-tax dollars—it offers a different form of tax reduction: tax-free growth and tax-free withdrawals in retirement. For high-income earners who expect to be in a higher tax bracket later in life, the Roth IRA is a powerful tool for long-term tax mitigation.

The Triple Tax Benefit of Health Savings Accounts (HSAs)

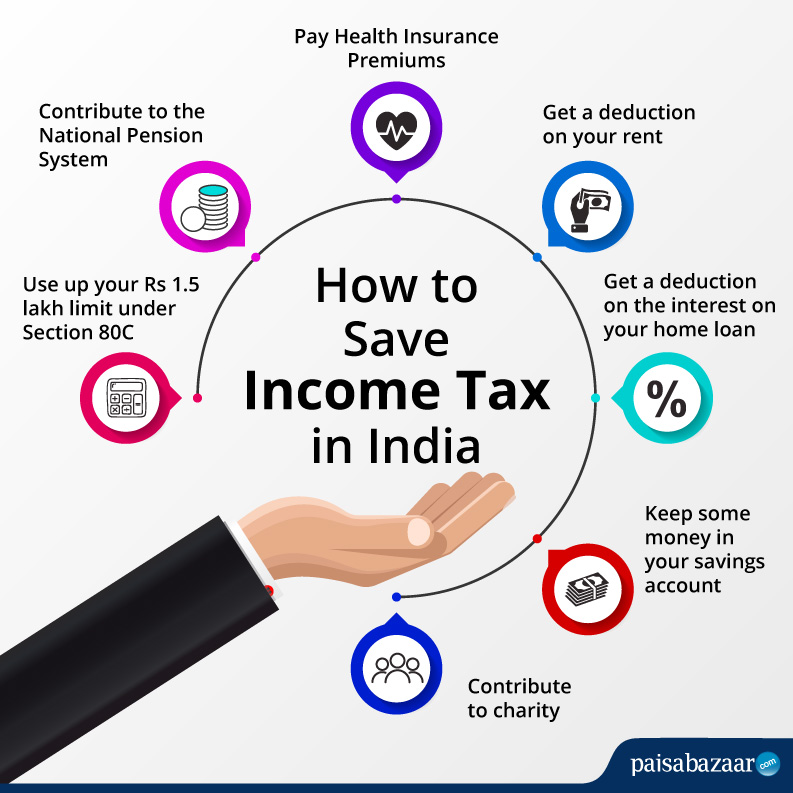

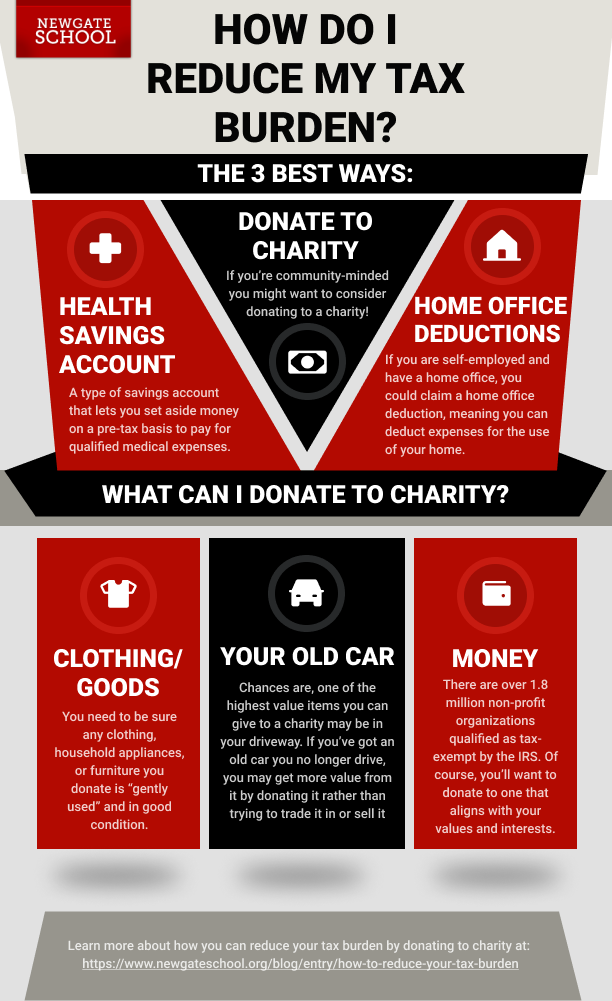

Often overlooked as a retirement tool, the Health Savings Account (HSA) is arguably the most tax-advantaged vehicle available. To qualify, you must be enrolled in a High Deductible Health Plan (HDHP). The HSA offers a triple tax advantage: contributions are 100% tax-deductible (lowering your current income tax), the investments grow tax-free, and withdrawals for qualified medical expenses are tax-free. If you can afford to pay for current medical expenses out of pocket and leave the HSA funds to grow, it essentially functions as a secondary retirement account with superior tax benefits.

2. Navigating Deductions and Tax Credits to Lower Your Bill

Understanding the difference between a tax deduction and a tax credit is fundamental to wealth management. A deduction reduces the amount of income that is subject to tax, while a credit is a dollar-for-dollar reduction in the actual tax you owe.

Choosing Between Standard and Itemized Deductions

The Tax Cuts and Jobs Act of 2017 significantly increased the standard deduction, leading many taxpayers to move away from itemizing. However, for those with significant mortgage interest, high state and local taxes (up to the $10,000 SALT cap), or substantial medical expenses, itemizing can still result in a lower tax bill than the standard deduction. It is essential to run the numbers both ways every year. If your total itemized deductions are close to the standard deduction limit, you might consider “clumping” or “bunching” deductions—such as making two years’ worth of charitable contributions in a single tax year—to surpass the threshold and maximize your savings.

Maximizing High-Value Tax Credits

Tax credits are the gold standard of tax reduction because they directly slash your final bill. The Child Tax Credit remains a vital tool for families, providing a significant reduction per qualifying child. For those pursuing higher education, the American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC) can offset the costs of tuition and fees. Additionally, as the economy shifts toward sustainability, credits for energy-efficient home improvements or the purchase of qualifying electric vehicles provide substantial opportunities to lower your tax liability while investing in your own assets.

Above-the-Line Deductions for Immediate Impact

“Above-the-line” deductions, or adjustments to income, are particularly valuable because you can claim them regardless of whether you take the standard deduction or itemize. These include deductions for student loan interest, educator expenses, and moving expenses for active-duty military members. These adjustments lower your Adjusted Gross Income (AGI), which is the benchmark used to determine your eligibility for various other credits and deductions. By lowering your AGI, you may become eligible for tax breaks that would otherwise be phased out at higher income levels.

3. Tax-Efficient Investment Strategies for Long-Term Growth

How you manage your investment portfolio can have a profound impact on your annual tax bill. Strategic investing is not just about choosing the right assets; it is about holding them in a way that minimizes the government’s take.

Utilizing Tax-Loss Harvesting to Offset Gains

Tax-loss harvesting is a sophisticated strategy used to minimize the taxes paid on investment gains. If you have investments that have declined in value, you can sell them to realize a loss. These losses can be used to offset any capital gains you realized during the year. If your losses exceed your gains, you can use up to $3,000 of the excess loss to offset your regular earned income. Any remaining loss can be carried forward to future years. This strategy allows you to “make the best of a bad situation” by using underperforming assets to reduce your overall tax burden.

The Importance of Asset Location and Holding Periods

Where you hold your assets matters just as much as what you hold. Tax-inefficient assets, such as actively managed mutual funds or REITs (Real Estate Investment Trusts) that produce high levels of taxable ordinary income, are best held in tax-deferred accounts like a 401(k) or IRA. Conversely, tax-efficient assets like index funds or stocks you plan to hold for the long term should be kept in taxable brokerage accounts. Furthermore, holding an asset for more than a year subjects the gains to long-term capital gains tax rates (0%, 15%, or 20%), which are significantly lower than the ordinary income tax rates applied to short-term gains.

Municipal Bonds and Tax-Exempt Interest

For investors in high tax brackets, municipal bonds offer a unique advantage. The interest earned on bonds issued by state and local governments is generally exempt from federal income tax. In many cases, if you live in the state where the bond was issued, the interest is also exempt from state and local taxes. While the interest rates on “munis” may be lower than corporate bonds, the “tax-equivalent yield” often makes them a superior choice for those looking to protect their income from heavy taxation.

4. Business-Owner and Side-Hustle Tax Optimizations

If you are a business owner, freelancer, or have a side hustle, you have access to a much broader range of tax reduction strategies than a traditional W-2 employee. The tax code is designed to reward entrepreneurship by allowing for the deduction of necessary business expenses.

Deducting Legitimate Business Expenses

Every dollar you spend to operate your business is a dollar that can potentially be deducted from your taxable revenue. This includes everything from marketing costs and software subscriptions to professional services like legal and accounting fees. The key is maintaining meticulous records. By capturing every “ordinary and necessary” expense, you ensure that you are only paying tax on your net profit, not your gross revenue.

Understanding the Qualified Business Income (QBI) Deduction

The QBI deduction, also known as Section 199A, allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income from their taxes. This is a massive benefit for sole proprietorships, partnerships, and S-corporations. While there are income limits and complexity regarding “specified service trades or businesses,” the QBI deduction represents one of the most significant tax-saving opportunities for the modern entrepreneur, effectively allowing a large portion of business income to go untaxed.

The Home Office Deduction and Section 179

If you use a portion of your home exclusively for business, you may be eligible for the home office deduction. This allows you to deduct a percentage of your rent or mortgage interest, utilities, insurance, and repairs. Additionally, for business owners purchasing equipment, Section 179 of the tax code allows you to deduct the full purchase price of qualifying equipment (like computers, machinery, or office furniture) in the year it was purchased, rather than depreciating it over several years. This provides an immediate and substantial reduction in taxable income during years of heavy capital investment.

5. Proactive Tax Planning and Annual Review Strategies

Tax reduction is not a task for April; it is a discipline for December and every month leading up to it. Proactive planning ensures that you are not surprised by a high bill and that you have time to implement strategies before the tax year closes.

Year-End Tax Moves to Secure Savings

As the year draws to a close, it is vital to perform a “tax projection.” If you realize your income is higher than expected, you might choose to defer further income into the following year or accelerate deductible expenses into the current year. For example, a freelancer might delay invoicing a client until January 1st to keep that income off the current year’s return. Similarly, making an extra mortgage payment in December can allow you to deduct the interest on that payment in the current tax year.

The Role of Charitable Giving in Tax Planning

Philanthropy is a powerful way to reduce your tax bill while supporting causes you care about. Beyond simple cash donations, donating appreciated securities (like stocks that have gone up in value) is a highly efficient strategy. By donating the stock directly to a 501(c)(3) organization, you avoid paying capital gains tax on the appreciation and can still claim a deduction for the full fair market value of the asset. For those who do not have a specific charity in mind but want the tax break now, a Donor-Advised Fund (DAF) allows you to make a large contribution today, take the immediate tax deduction, and distribute the funds to charities over time.

In conclusion, reducing your income tax is a multi-faceted endeavor that requires a blend of retirement discipline, investment savvy, and a thorough understanding of the tax code’s various deductions and credits. By viewing tax planning as an integral part of your overall financial strategy—rather than a yearly chore—you can preserve more of your wealth, increase your investment capital, and achieve your long-term financial goals with greater efficiency. Always consult with a qualified tax professional to ensure that your strategies are compliant with the latest tax laws and tailored to your specific financial situation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.