In the complex world of vehicle transactions, understanding the nuances of a car’s title is paramount to making sound financial decisions. The term “blue title Texas” might raise questions for buyers and sellers alike, hinting at a specific status or history that sets it apart from a standard “clean” title. While “blue title” isn’t an official designation used by the Texas Department of Motor Vehicles (TxDMV), it’s a term often used colloquially to refer to a specific type of branded title – most commonly a rebuilt title – or sometimes to a title with particular lien or bonding conditions, which often carries significant financial ramifications.

For anyone navigating the Texas vehicle market, deciphering the various title statuses is not just a matter of legal compliance but a critical component of personal finance, asset valuation, and risk management. This article will delve into what a “blue title” might signify in Texas, its financial implications for purchasing, insuring, and selling a vehicle, and how to make informed decisions to protect your financial interests.

The Foundation of Vehicle Titles in Texas

A vehicle title is more than just a piece of paper; it’s the legal document proving ownership and, crucially, detailing the vehicle’s history, particularly any significant events that might impact its value or safety. Understanding the different types of titles issued in Texas is the first step toward grasping the financial weight of a “blue title.”

The Role of a Clean Title

A “clean title” represents the ideal and most straightforward scenario in vehicle ownership. It indicates that the vehicle has never been deemed a total loss by an insurance company due to accident, flood, fire, or other damage. Vehicles with clean titles are generally easier to finance, insure, and resell, commanding higher market values because their history is free from major damaging events. From a financial perspective, a clean title minimizes risk and maximizes the liquidity and value of the asset. It assures lenders and insurers of the vehicle’s unblemished past, leading to favorable terms and broader market appeal.

Demystifying Branded Titles: Beyond “Clean”

Any title that is not “clean” is generally referred to as a “branded title.” These titles carry specific designations that reveal a significant event in the vehicle’s past. Branded titles are critical financial markers because they directly signal potential issues, reduced value, and increased risk. Common branded titles include:

- Salvage Title: Issued when an insurance company declares a vehicle a total loss because the cost of repairs exceeds a certain percentage (often 75-100%) of its fair market value. These vehicles are typically unsafe and cannot be legally driven until repaired and inspected.

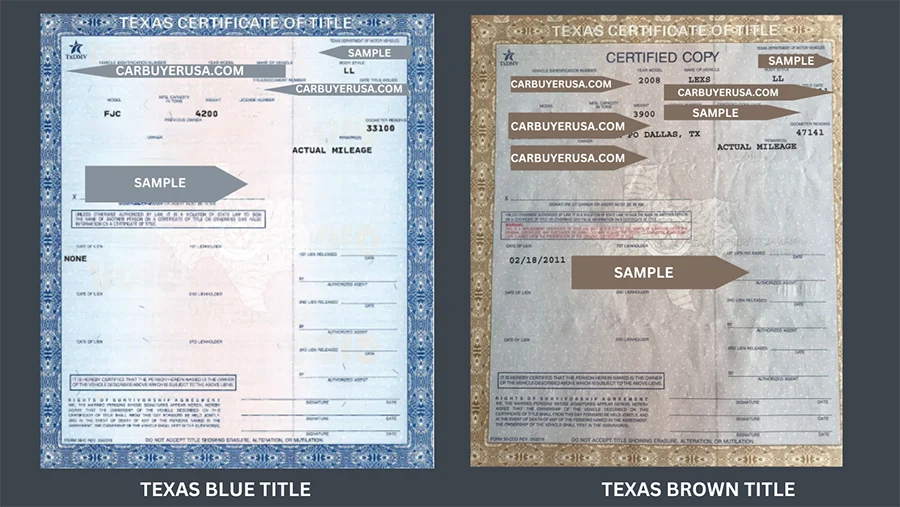

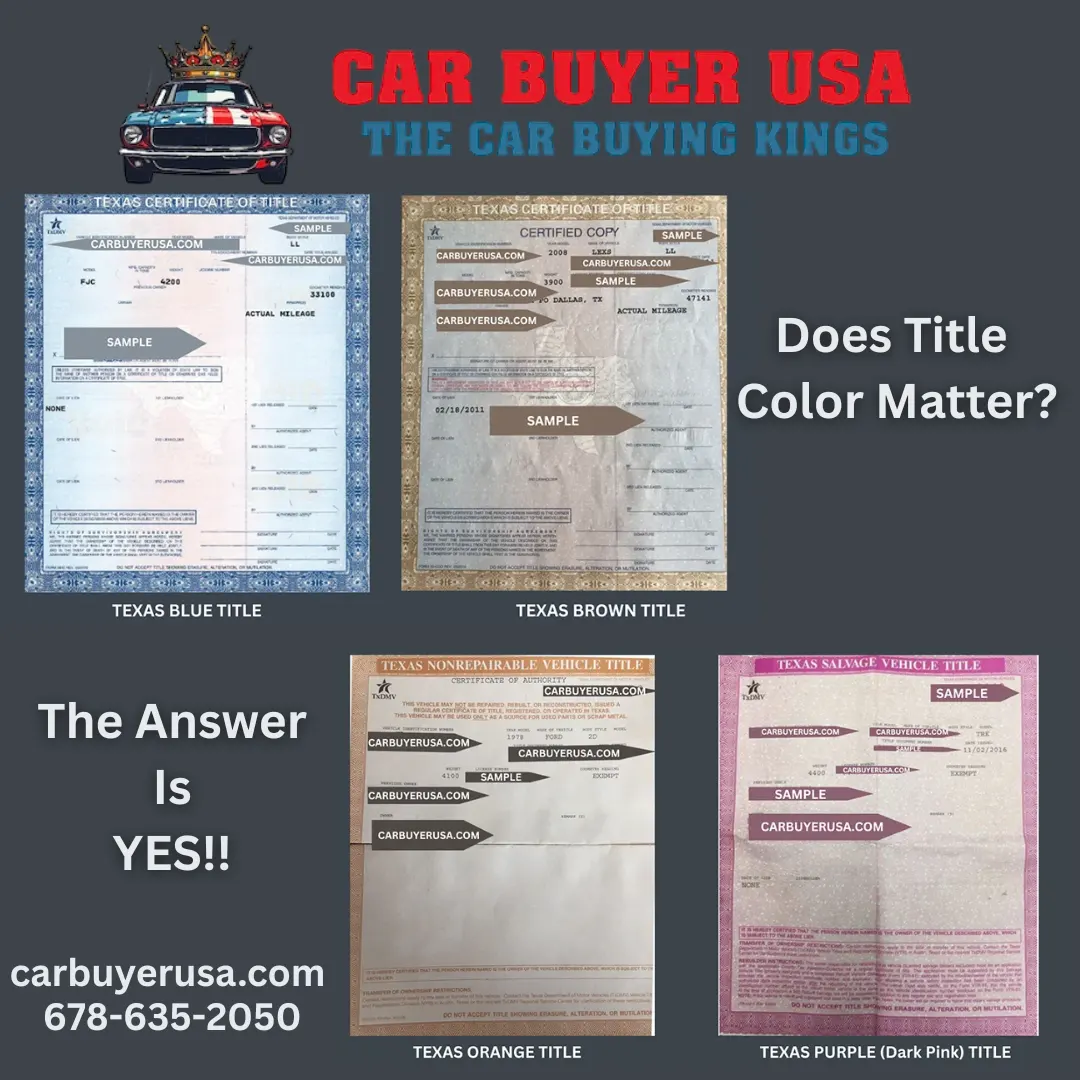

- Rebuilt/Reconstructed Title: Issued after a vehicle with a salvage title has been repaired and inspected to ensure it is roadworthy and safe. This is where the term “blue title” often comes into play in Texas, informally referring to a rebuilt title, especially if the physical document or its history is associated with a specific color or process.

- Flood Title: Indicates the vehicle has sustained significant water damage, which can lead to long-term electrical and mechanical issues.

- Lemon Law Buyback Title: Issued to vehicles that were repurchased by the manufacturer due to recurring, unfixable defects.

- Bonded Title: A special type of title for vehicles where the original title is lost, stolen, or improperly assigned, requiring the owner to post a surety bond to protect against future claims on the vehicle.

Each of these brands serves as a financial warning sign, indicating a departure from the typical clean-title vehicle’s value and utility.

Texas Specifics: Salvage, Rebuilt, and Other Designations

In Texas, the TxDMV meticulously records a vehicle’s history and applies appropriate branding. A vehicle declared a “salvage” in Texas cannot be registered or driven until it undergoes specific repairs and passes a state safety inspection. Once it passes, it is issued a rebuilt salvage title. This is often the point where the informal term “blue title” might be applied. Buyers and sellers need to consult the TxDMV’s official records to understand the precise branding, as relying on informal terms can lead to significant financial miscalculations. The financial implications stem directly from these official designations, which dictate how the vehicle is valued, insured, and sold.

Interpreting the “Blue Title” Phenomenon and Its Financial Weight

When someone refers to a “blue title Texas,” they are most likely describing a vehicle that has been designated as “rebuilt” after previously holding a “salvage” status, or perhaps a vehicle with a “bonded title.” The color “blue” might refer to a specific color used on certain state documents, or it could be a regional colloquialism. Regardless of the exact etymology of the term, its financial implications are rooted in the vehicle’s underlying branded status.

Colloquial Meanings of “Blue Title”

In Texas, the most common interpretation of a “blue title” among consumers and dealerships often points to a vehicle that has undergone a significant transformation: from a declared total loss (salvage) to a roadworthy, inspected vehicle (rebuilt). This distinction is critical from a financial perspective. A vehicle with a rebuilt title has a documented history of severe damage. While repaired and deemed safe, its past cannot be erased. Other less common interpretations could include a “bonded title” where there were issues with prior ownership proof, requiring a surety bond for its legal titling. In all these cases, the “blue title” signifies a deviation from a standard, clean title, and thus, a different financial profile.

Direct Impact on Vehicle Valuation and Market Price

The presence of a branded title—whether formally “rebuilt salvage” or colloquially “blue title”—has an immediate and substantial negative impact on a vehicle’s market value. Industry experts and pricing guides (like Kelley Blue Book or NADAguides) typically assign significantly lower values to branded title vehicles, often reducing their worth by 20% to 50% compared to an identical model with a clean title. This depreciation reflects several factors:

- Perceived Risk: Buyers are inherently wary of vehicles with a history of major damage, fearing latent issues or reduced longevity.

- Demand: The pool of potential buyers for branded title vehicles is smaller, reducing demand and driving down prices.

- Repair Quality: There’s always an element of uncertainty regarding the quality of the repairs performed on a previously salvaged vehicle. Even if inspected, the repairs might not restore the vehicle to its original factory condition or integrity.

For sellers, this means accepting a lower sales price. For buyers, it presents an opportunity for a cheaper purchase, but with the caveat of potentially higher future costs or reduced resale value.

Financing Hurdles and Lending Institution Perspectives

Securing financing for a vehicle with a branded title can be significantly more challenging. Many traditional lenders and banks are reluctant to offer loans for “blue title” or rebuilt vehicles, or they might offer less favorable terms:

- Higher Interest Rates: Lenders perceive a greater risk with branded titles, often mitigating this by charging higher interest rates.

- Stricter Down Payment Requirements: You might be required to put down a larger percentage of the purchase price.

- Shorter Loan Terms: Lenders may prefer shorter repayment periods to minimize their exposure.

- Reduced Loan-to-Value (LTV) Ratios: The amount they are willing to lend relative to the vehicle’s value will be lower, reflecting the depreciated worth of a branded title vehicle.

Some lenders may refuse to finance branded title vehicles altogether due to their diminished collateral value and higher default risk. This directly impacts a buyer’s ability to afford such a vehicle and can limit their purchasing options, effectively raising the true cost of ownership through financing limitations.

Navigating Insurance and Liability with a “Blue Title” Vehicle

The financial implications of a “blue title” extend beyond just purchase price and financing; they profoundly affect how a vehicle is insured and the owner’s potential liability.

Comprehensive vs. Liability Coverage Considerations

Insurance companies assess risk based on the vehicle’s condition and history. For a vehicle with a rebuilt or “blue title” status, securing comprehensive and collision coverage can be problematic. While liability insurance (which covers damage you cause to others) is generally available and legally required, full coverage (which covers damage to your own vehicle) is often difficult to obtain or comes with specific limitations:

- Limited Coverage Options: Some insurers may only offer liability, fire, and theft coverage, refusing comprehensive or collision.

- Stipulated Value Policies: If full coverage is offered, it might be under a “stipulated value” policy, where the insurer and owner agree on a pre-determined maximum payout in case of a total loss. This agreed value will almost always be significantly lower than a clean-title equivalent.

- Exclusions: Policies may include exclusions for damages related to the vehicle’s prior accident history.

This means that in the event of another accident, the owner of a “blue title” vehicle might face substantial out-of-pocket expenses for repairs, or receive a much smaller payout from their insurer, representing a significant financial risk.

Potential for Higher Premiums and Lower Payouts

Even when full coverage is available for a “blue title” vehicle, the premiums can sometimes be higher due to the increased perceived risk. Insurers may factor in the vehicle’s past damage history, making actuarial calculations that result in elevated rates. Crucially, in the event of a total loss, the payout will be based on the vehicle’s current depreciated market value as a branded title vehicle. This value is considerably lower than that of a clean-title vehicle, meaning the owner will recover far less than they might expect, leading to a substantial financial loss. This gap between expectation and reality can be a significant financial blow.

Understanding Owner Liability and Financial Risk

While a rebuilt “blue title” vehicle has passed inspection, its structural integrity or long-term reliability might still be compromised. If a defect related to prior damage causes an accident, the owner could face increased scrutiny or liability claims. Furthermore, ongoing maintenance costs might be higher due due to unforeseen issues stemming from the initial damage. Owners must be prepared for potentially greater financial outlays for repairs and maintenance, which should be factored into the overall cost of ownership. Transparency is also key: failure to disclose a vehicle’s branded title status when selling it can lead to legal and financial repercussions for the seller.

Strategic Financial Decisions for Buying or Selling a “Blue Title” Vehicle

Whether you’re considering buying or selling a vehicle with a “blue title” in Texas, a strategic financial approach is essential to protect your assets and avoid unexpected costs.

Due Diligence for Buyers: Pre-Purchase Inspections and History Reports

For prospective buyers, thorough due diligence is non-negotiable. This means:

- Vehicle History Report: Always obtain a comprehensive vehicle history report (e.g., CarFax, AutoCheck) using the VIN. This report will reveal the official branded title status (salvage, rebuilt, flood, etc.), accident history, odometer discrepancies, and previous ownership. This is your primary tool for financial risk assessment.

- Independent Pre-Purchase Inspection (PPI): Even if a vehicle has a rebuilt title and has passed state inspection, hire an independent, certified mechanic to perform a thorough pre-purchase inspection. This inspection should specifically focus on identifying any lingering issues related to the previous damage, structural integrity, and the quality of repairs. This small upfront investment can save you thousands in future repair costs.

- Negotiate Price Aggressively: Armed with the vehicle’s history and inspection results, be prepared to negotiate the price significantly downward to reflect its branded title status and any identified defects.

Failing to conduct these steps can lead to severe financial consequences, as you might overpay for a vehicle with hidden problems.

Transparent Disclosure for Sellers: Ethical and Legal Obligations

Sellers of “blue title” vehicles have an ethical and, in many cases, a legal obligation to disclose the vehicle’s full title history to potential buyers. In Texas, while not always explicitly requiring disclosure of specific title brands for private sales, misrepresentation can lead to legal action for fraud or breach of contract. Best practices for sellers include:

- Provide History Reports: Be proactive and provide potential buyers with a vehicle history report.

- Clearly State Title Status: Explicitly state the vehicle’s “rebuilt” or “blue title” status in advertisements and during discussions.

- Document Everything: Keep records of repairs, inspections, and all communications regarding the vehicle’s history.

Transparency protects the seller from future legal and financial disputes and builds trust, potentially facilitating a smoother sale, albeit at a lower price point.

Maximizing Resale Value and Market Appeal

While a “blue title” inherently reduces a vehicle’s value, sellers can take steps to maximize their return:

- High-Quality Repairs: Ensure any repairs performed were done by reputable shops using quality parts. Documenting these repairs with receipts and photos can add credibility.

- Excellent Maintenance Records: Consistent maintenance and repair records demonstrate ongoing care for the vehicle.

- Competitive Pricing: Research the market for similar branded title vehicles to price yours competitively. Overpricing will deter buyers, while a fair price reflecting its condition and title status can attract a quicker sale.

- Focus on Value Proposition: Highlight any recent upgrades, new tires, or excellent mechanical condition to offset the title brand.

From a financial perspective, a seller’s goal is to mitigate the depreciation caused by the “blue title” by showcasing the vehicle’s current reliability and condition.

Conclusion

The term “blue title Texas,” while not an official state designation, serves as a crucial informal marker that often indicates a vehicle with a branded history, most commonly a rebuilt salvage title. Understanding what this designation entails is indispensable for anyone involved in vehicle transactions in Texas. From reduced market value and challenging financing options to complex insurance considerations and potential liability, the financial implications of a “blue title” vehicle are extensive.

Both buyers and sellers must approach these transactions with meticulous due diligence, transparency, and a clear understanding of the financial risks and opportunities involved. By thoroughly researching vehicle history, obtaining independent inspections, and making informed decisions, individuals can navigate the complexities of “blue title” vehicles in Texas, safeguarding their financial well-being and making economically sound choices in the vibrant Texas automotive market. Always consult official TxDMV resources and, when in doubt, seek advice from financial or legal professionals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.