In the contemporary financial landscape, the shift from physical currency to digital liquidity has been seismic. Among the plethora of peer-to-peer (P2P) payment platforms, Venmo has emerged not merely as a convenience but as a fundamental financial tool for managing daily expenditures, splitting obligations, and even handling micro-business transactions. Understanding how to send Venmo money effectively requires more than just a passing knowledge of the interface; it demands an appreciation for digital security, fee structures, and the strategic management of one’s personal or business capital.

As we move closer to a truly cashless society, mastering these digital tools is essential for maintaining financial agility. This guide explores the nuances of the Venmo ecosystem, providing a detailed roadmap for navigating transactions with professional precision.

Mastering the Fundamentals of Digital Payments via Venmo

The process of sending money digitally is the cornerstone of modern personal finance. While the user interface is designed for simplicity, the underlying financial mechanisms require careful setup to ensure that funds move securely and efficiently from one ledger to another.

Setting Up Your Financial Foundation

Before the first dollar can be sent, a user must establish a secure link between their Venmo profile and their primary financial institutions. From a personal finance perspective, the choice of funding source is critical. Users can link a traditional checking account, a debit card, or a credit card.

It is important to note that using a credit card to send money on Venmo typically incurs a 3% transaction fee. For those focused on cost-saving and fiscal responsibility, linking a debit card or a direct bank account is the preferred method, as these transactions are generally free of processing fees. This initial setup phase is also the time to implement multi-factor authentication (MFA), a non-negotiable step for protecting one’s digital assets.

The Mechanics of a Transaction

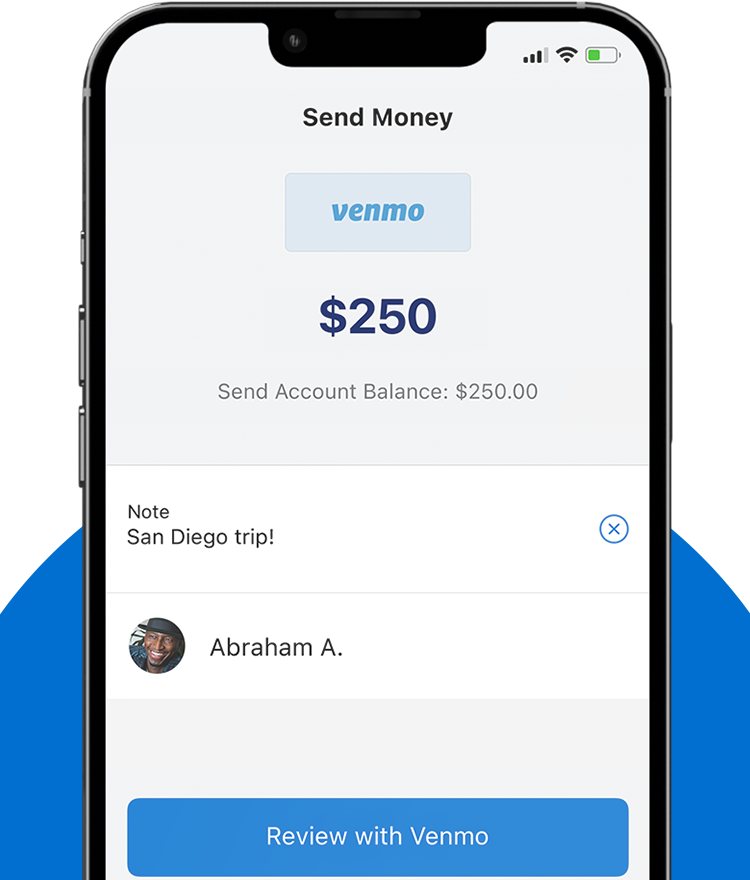

Sending money on Venmo is initiated through the “Pay or Request” function. To maintain professional financial records, it is advisable to use the search function to find recipients via their unique @username, phone number, or email. The “memo” or “note” field, while often used for social engagement via emojis, serves a practical purpose in personal accounting. Detailed notes help in tracking expenditures during tax season or when reconciling monthly budgets. Once the amount is entered and the funding source is confirmed, the transaction is near-instantaneous, reflecting immediately in the recipient’s Venmo balance.

Navigating the Financial Ecosystem: Fees, Limits, and Transfers

A sophisticated user of financial tools must understand the “cost of doing business.” Venmo operates on a freemium model where basic services are free, but specific conveniences and higher-tier functionalities come with associated costs that can impact one’s net liquidity.

Understanding the Cost of Convenience

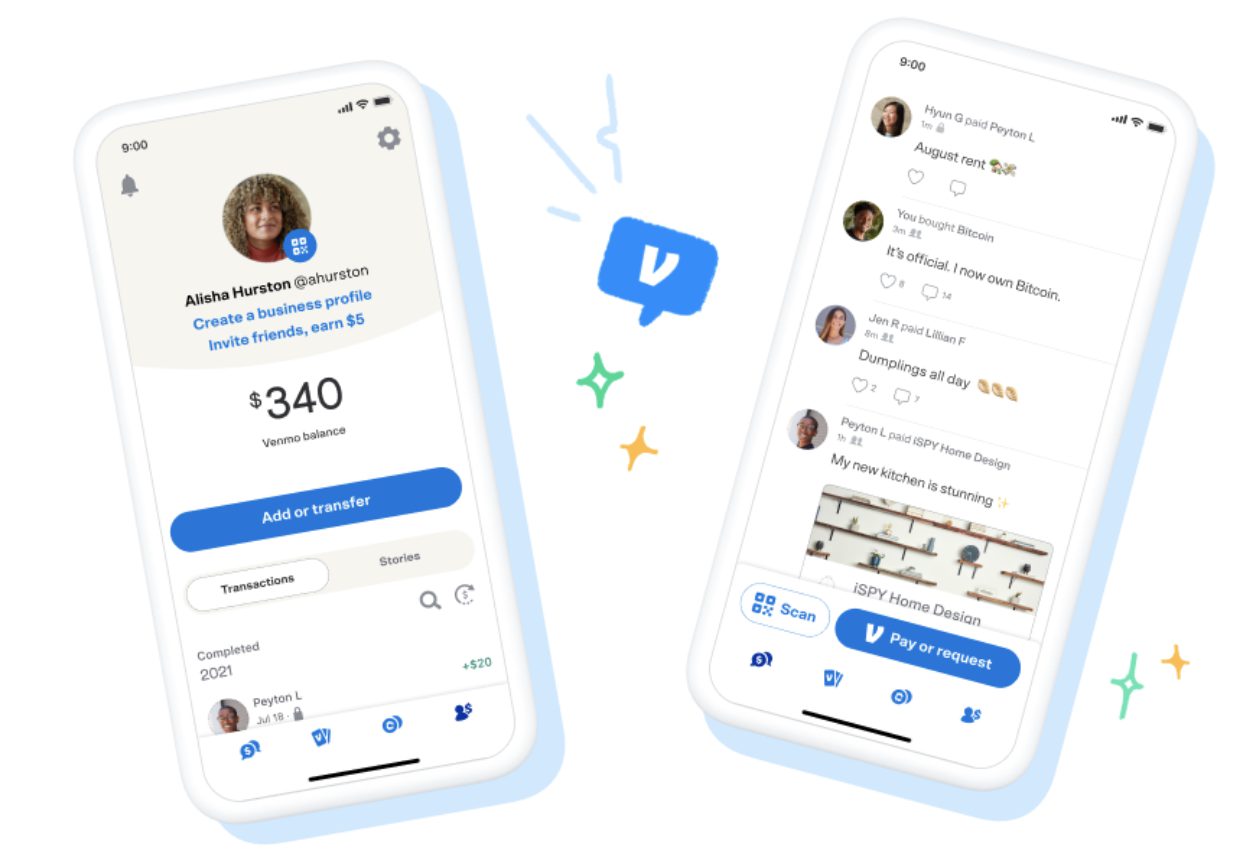

When money is received in a Venmo account, it stays in a “Venmo Balance” until the user decides to move it to a traditional bank. There are two primary methods for this:

- Standard Transfer: This is a free service that typically takes one to three business days. For individuals with a healthy cash flow who do not need immediate access to funds, this is the most fiscally sound option.

- Instant Transfer: For a fee (currently 1.75% of the transfer amount, with a minimum and maximum cap), users can move funds to an eligible debit card or bank account within minutes. While convenient, frequent use of instant transfers can result in a significant “convenience tax” over time, eroding personal savings.

Managing Transaction Limits and Verification

Venmo imposes specific limits on how much money can be sent and received. Unverified accounts face much lower ceilings, often limited to a few hundred dollars per week. To unlock the full potential of the platform—such as a weekly rolling limit that can exceed $19,000—users must undergo a formal identity verification process. This involves providing a Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). From a financial management standpoint, completing this verification is essential for anyone using the platform for significant household expenses, such as rent or mortgage shares.

Strategic Financial Management for Personal and Business Use

As Venmo has matured, it has evolved from a simple social payment app into a dual-purpose tool for personal budgeting and micro-enterprise management. Distinguishing between these two use cases is vital for tax compliance and financial clarity.

Venmo for Personal Budgeting and Group Expenses

For the modern consumer, Venmo serves as a powerful ledger for group-based financial obligations. Features like “Split” allow users to divide a single large expense—such as a utility bill or a shared dinner—among multiple parties with a few taps. This transparency reduces the friction of “who owes what” and ensures that personal budgets remain balanced. By reviewing transaction history, users can categorize their spending, identifying trends in discretionary versus non-discretionary outlays.

Transitioning to Venmo for Business: Tax Implications

The IRS has increasingly focused on digital payment platforms. Users receiving payments for goods and services must be aware of the 1099-K reporting requirements. If you use Venmo for a side hustle or a small business, it is imperative to set up a dedicated “Business Profile.”

Business profiles incur a small seller fee (typically 1.9% plus a fixed fee), but they offer several advantages:

- Tax Compliance: Venmo tracks these payments and provides the necessary documentation for tax filing if you meet the federal or state thresholds.

- Professionalism: It separates personal “splitting the bill” transactions from professional income, making it easier for accountants to audit your records.

- Purchase Protection: Transactions marked as “Goods and Services” may be eligible for Venmo’s Purchase Protection, providing a layer of security that personal payments lack.

Securing Your Digital Assets: Protection and Dispute Resolution

In the realm of digital finance, security is the paramount concern. Unlike traditional wire transfers or credit card payments, P2P transactions are often difficult to reverse, making the sender’s due diligence the first line of defense against financial loss.

Implementation of Multi-Layered Security Protocols

To protect the capital within your Venmo account, professional users should go beyond basic passwords. Enabling biometric locks (FaceID or Fingerprint) on the app ensures that even if a device is compromised, the funds remain inaccessible. Furthermore, adjusting privacy settings is a prudent move. While Venmo has a social component, setting your transactions to “Private” ensures that your financial habits and recipient lists are not visible to the public or your broader social network.

Navigating Payment Errors and Potential Scams

One of the most common financial pitfalls in the P2P space is the “accidental payment” or the “scam-back” maneuver. If money is sent to the wrong person, Venmo cannot simply “undo” the transaction due to the immediate nature of the funds transfer. The sender must request the money back and hope for the recipient’s honesty.

To mitigate risk:

- Verify Identifiers: Always double-check the recipient’s QR code or specific handle before hitting “Send.”

- Avoid Strangers: Never use the personal “Pay” feature to buy items from unverified sellers on marketplaces. Scammers often request payments via the “friends and family” style transfer because it offers no recourse for the buyer if the goods never arrive. Use the “Goods and Services” toggle to ensure your money is protected under Venmo’s corporate policies.

Conclusion: The Future of Mobile Finance

The ability to send money via Venmo has revolutionized how we interact with our finances. It has removed the barriers of physical distance and the delays of traditional banking, allowing for a more fluid and responsive economic life. However, with this speed comes a heightened responsibility for the user.

By treating Venmo as a serious financial tool—optimizing for low fees, ensuring tax compliance through business profiles, and maintaining rigorous security standards—users can leverage this technology to enhance their financial well-being. Whether you are settling a small debt with a friend or managing the cash flow of a burgeoning side business, the strategic use of Venmo is a hallmark of the modern, financially literate individual. As the platform continues to integrate with broader financial services like cryptocurrency and high-yield savings, staying informed on its evolving features will be key to navigating the future of money.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.