Pursuing a graduate or professional degree is a significant investment in your future. Whether you are aiming for a Master’s, a Ph.D., a law degree, or a medical qualification, the costs associated with higher education can be daunting. While scholarships, grants, and Federal Direct Unsubsidized Loans are the first lines of defense, they often fall short of covering the total cost of attendance. This is where the Grad PLUS loan comes into play.

A Grad PLUS loan—officially known as a Direct PLUS Loan for graduate or professional students—is a federal student loan offered by the U.S. Department of Education. It is designed specifically to bridge the gap between other financial aid and the total cost of your education. Understanding the nuances of this financial tool is essential for any prospective graduate student looking to manage their debt responsibly while securing the necessary funds for their academic journey.

Understanding Eligibility and the Application Process

Before diving into the financial specifics, it is crucial to understand who can access these funds and how the process begins. Unlike undergraduate federal loans, Grad PLUS loans involve a slightly more rigorous check on your financial background.

Basic Eligibility Requirements

To qualify for a Grad PLUS loan, you must be a graduate or professional student enrolled at least half-time at an eligible school in a program leading to a graduate or professional degree or certificate. You must also meet the general eligibility requirements for federal student aid, which include being a U.S. citizen or eligible non-citizen and maintaining satisfactory academic progress.

The Role of Credit History

One of the most significant differences between Grad PLUS loans and other federal student loans is the requirement of a credit check. While the government does not look for a specific “credit score” in the way a private bank might, they do look for “adverse credit history.” This includes recent bankruptcies, foreclosures, tax liens, or serious delinquencies on existing debt. If you do have adverse credit history, you may still be able to receive a loan if you find an “endorser” (similar to a cosigner) or if you can demonstrate extenuating circumstances.

How to Apply via the FAFSA

The journey toward securing a Grad PLUS loan always begins with the Free Application for Federal Student Aid (FAFSA). Even though the PLUS loan is a separate application on the Federal Student Aid website, your school will use your FAFSA data to determine your overall aid package. Once the FAFSA is processed and you have exhausted your Unsubsidized Loan limits, you can specifically apply for the Grad PLUS loan, which requires signing a Master Promissory Note (MPN).

Key Features, Interest Rates, and Borrowing Limits

Grad PLUS loans offer several unique features that distinguish them from both undergraduate federal loans and private student loans. Understanding these mechanics helps in calculating the long-term cost of your education.

Borrowing Limits: Closing the Gap

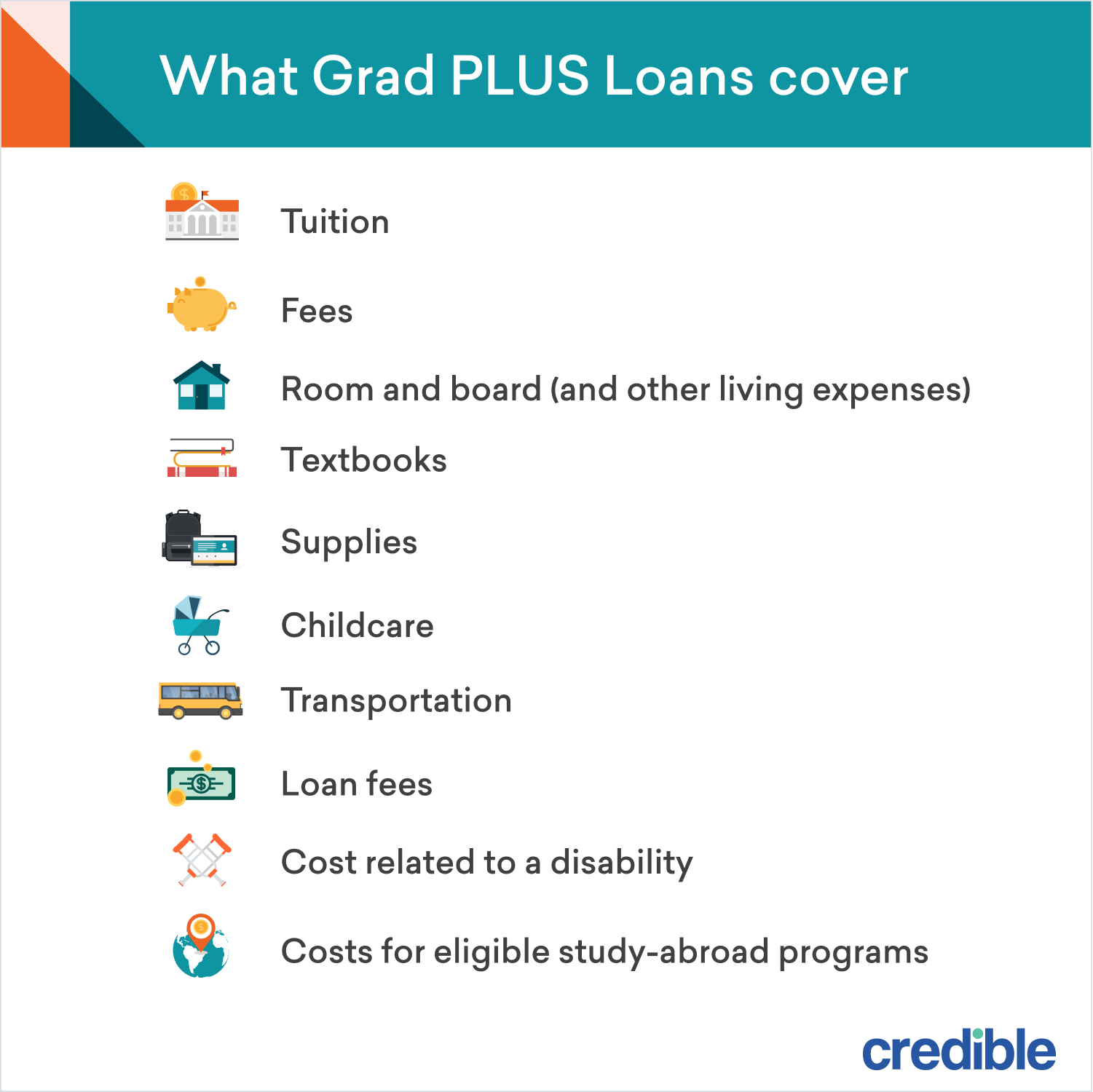

The most attractive feature of the Grad PLUS loan is its borrowing limit. Unlike Direct Unsubsidized Loans, which have annual and aggregate caps (currently $20,500 per year for most graduate students), the Grad PLUS loan allows you to borrow up to the full cost of attendance (COA) as determined by your school, minus any other financial aid you have received. This COA includes tuition, fees, room and board, books, supplies, and even transportation.

Interest Rates and Disbursement Fees

Because Grad PLUS loans are federal, they carry fixed interest rates, meaning the rate remains the same for the life of the loan. However, these rates are typically higher than those for undergraduate loans and Direct Unsubsidized graduate loans. In addition to interest, there is a loan disbursement fee—a percentage of the total loan amount that is deducted proportionately from each loan disbursement. This fee is relatively high (often around 4%), so it is vital to factor this “hidden cost” into your budget when deciding how much to borrow.

The Benefits of Federal Protection

Despite the higher interest rates compared to other federal options, Grad PLUS loans offer protections that private lenders rarely match. These include death and disability discharge, the ability to consolidate loans, and a variety of deferment and forbearance options if you encounter financial hardship after graduation.

Repayment Options and Debt Management Strategies

Managing the repayment of a Grad PLUS loan requires a proactive approach. Because these loans can accumulate to large sums, choosing the right repayment plan is a cornerstone of personal financial health.

Deferment and the Grace Period

Technically, repayment for a Grad PLUS loan begins as soon as the loan is fully disbursed. However, graduate students are entitled to an in-school deferment, meaning you do not have to make payments while you are enrolled at least half-time. Furthermore, you are typically granted a six-month “grace period” or post-enrollment deferment after you graduate, leave school, or drop below half-time enrollment. It is important to remember, however, that interest continues to accrue during these periods and will be capitalized (added to the principal balance) once repayment begins.

Income-Driven Repayment (IDR) Plans

For many advanced degree holders, especially those entering fields like social work, education, or academia, monthly payments based on standard 10-year plans can be overwhelming. Grad PLUS loans are eligible for Income-Driven Repayment (IDR) plans. These plans cap your monthly payments at a percentage of your discretionary income and can extend the repayment term to 20 or 25 years. Any remaining balance at the end of the term is forgiven, though that forgiven amount may currently be treated as taxable income.

Public Service Loan Forgiveness (PSLF)

If you plan to work for a government organization or a non-profit 501(c)(3), Grad PLUS loans are a powerful tool because they qualify for Public Service Loan Forgiveness. Under PSLF, if you make 120 qualifying monthly payments under an IDR plan while working full-time for a qualifying employer, the remaining balance of your federal loans is forgiven tax-free. This makes Grad PLUS loans significantly more attractive than private loans for public servants.

Comparing Grad PLUS Loans to Private Student Loans

When looking for additional funding, many students weigh the pros and cons of federal Grad PLUS loans against private student loans offered by banks or credit unions. The choice depends largely on your current financial standing and future career goals.

When Private Loans Might Be Better

If you have an exceptional credit score or a high-earning cosigner, you might find that a private lender offers a lower interest rate than the federal Grad PLUS loan. Additionally, private lenders do not always charge the high disbursement fees associated with federal loans. For a student certain of a high-paying career in the private sector (such as big-law or corporate medicine) who does not need federal protections, a private loan could save thousands of dollars in interest.

The Risks of Private Lending

The primary downside of private loans is the lack of flexibility. Private lenders rarely offer income-driven repayment or loan forgiveness programs. If the economy shifts or you lose your job, private lenders are generally less accommodating than the federal government. Furthermore, private loan interest rates can be variable, meaning they could rise significantly over the life of the loan, whereas Grad PLUS rates are locked in.

The Hybrid Approach

Some students choose to use Grad PLUS loans for the security and then, after graduation and securing a stable job, refinance those loans into a private loan with a lower interest rate. While this “best of both worlds” strategy can save money, it is a one-way street: once you refinance federal loans into private loans, you permanently lose access to federal benefits like PSLF and IDR plans.

Financial Responsibility and the Long-Term Impact

Borrowing for a graduate degree is not just a student aid decision; it is a major life decision. The debt-to-income ratio you carry after graduation will influence your ability to buy a home, start a family, or invest for retirement.

Calculating the True Cost

Before signing for a Grad PLUS loan, use a loan simulator to see what your monthly payments will look like. Remember that because interest accrues while you are in school, the amount you owe upon graduation will be higher than the amount you originally borrowed. If you have the means, paying off the interest as it accrues while you are still in school can prevent the balance from ballooning through capitalization.

Budgeting for the Essentials

Since Grad PLUS loans allow you to borrow up to the full cost of attendance, it can be tempting to borrow the maximum amount offered. However, every dollar borrowed is a dollar (plus interest) that must be paid back out of your future earnings. Experts recommend borrowing only what is strictly necessary for tuition and basic living expenses. Practicing a frugal lifestyle during your graduate years can result in significantly more financial freedom in your thirties and forties.

Strategic Planning for the Future

The Grad PLUS loan is a valuable financial instrument when used with a clear strategy. Whether that strategy involve aggressive repayment, utilizing PSLF, or eventual refinancing, the key is to remain informed. By understanding the terms, staying aware of interest rates, and planning for repayment before you even receive your first disbursement, you can ensure that your graduate degree remains a stepping stone to prosperity rather than a financial burden.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.