The term “stock market crash” often conjures images of frantic trading floors, ticker tapes spiraling downward, and headlines dominated by financial despair. While a crash is undeniably a significant economic event, understanding the mechanics, the consequences, and the opportunities it presents is essential for any serious investor. A crash is generally defined as a sudden, dramatic drop in stock prices across a major cross-section of a stock market, typically fueled by panic as much as by underlying economic factors.

When the market takes a dive—defined often as a decline of more than 20% in a very short period—it triggers a chain reaction that moves through the financial system and into the “real” economy. For the individual investor, the immediate aftermath is often characterized by a mixture of fear and uncertainty. However, for the prepared, a crash is not just an end; it is a profound transition period in the cycle of wealth creation.

The Economic Ripple Effect: From Wall Street to Main Street

A stock market crash is rarely a self-contained event within the digital screens of brokerage firms. Because the stock market serves as a barometer for economic health and a primary vehicle for corporate funding, a sharp decline has tangible consequences for the broader economy.

The Wealth Effect and Consumer Spending

One of the most immediate impacts of a market crash is the “negative wealth effect.” When stock prices plummet, household wealth evaporates—at least on paper. This leads to a psychological shift where consumers feel less wealthy and, consequently, reduce their discretionary spending. Since consumer spending accounts for a significant portion of the GDP in many developed nations, this contraction can lead to a slowing of economic growth or even a recession. When people stop buying cars, luxury goods, or even upgrading their homes, the companies producing these goods see their revenues drop, further fueling the downward cycle.

Corporate Liquidity and Capital Constraints

For businesses, the stock market is a vital tool for raising capital. When a market crashes, the cost of equity rises dramatically. Companies that intended to issue new shares to fund research and development, expansion, or debt repayment find themselves in a difficult position. Furthermore, a crash often coincides with a tightening of the credit markets. Banks and lenders become more risk-averse, making it harder for businesses to secure the loans necessary for daily operations. This “credit crunch” can lead to hiring freezes, layoffs, and a reduction in capital expenditures, which impacts the job market and long-term industrial productivity.

The Systemic Risk to Financial Institutions

Modern finance is deeply interconnected. A crash can trigger margin calls, where investors who borrowed money to buy stocks are forced to sell their holdings to cover their debts. This forced selling puts even more downward pressure on prices. If the decline is steep enough, it can threaten the solvency of brokerage firms and investment banks. While post-2008 regulations have increased the capital requirements for these institutions, a systemic shock can still create liquidity bottlenecks where the flow of money through the global economy slows to a crawl.

Personal Wealth: Navigating Portfolio Drawdowns and Psychological Stress

For the individual investor, a market crash is an emotional litmus test. It is one thing to see a “stress test” on a spreadsheet; it is quite another to watch your retirement account balance drop by 30% in a single month. Understanding the difference between realized and unrealized losses is the first step in surviving the turbulence.

Paper Losses vs. Realized Losses

The most critical lesson during a crash is that a decline in portfolio value is only a “paper loss” until the assets are actually sold. When stock prices drop, you still own the same number of shares in a company or an index fund. If the underlying companies remain profitable and resilient, the value of those shares has the potential to recover. The danger lies in “panic selling”—the act of selling assets at the bottom of the market due to fear. This crystallizes the loss, preventing the investor from participating in the eventual recovery. Successful long-term investing requires the emotional fortitude to stay the course when the headlines are most dire.

The Impact on Retirement and Fixed-Income Goals

For those nearing retirement, a market crash can be particularly daunting. This is known as “sequence of returns risk.” If a crash occurs just as an individual begins withdrawing funds for living expenses, they are forced to sell shares at depressed prices, which can significantly shorten the lifespan of their portfolio. This highlights the importance of asset allocation. Ideally, those close to retirement should hold a portion of their wealth in less volatile assets, such as high-quality bonds or cash equivalents, which act as a buffer and allow the equity portion of the portfolio time to recover without being liquidated at a loss.

Margin Calls and the Perils of Leverage

Investors using leverage—borrowed money—face the greatest risk during a crash. As the value of the collateral (the stocks) falls, brokers issue margin calls requiring the investor to deposit more cash or sell assets immediately. This often leads to a “death spiral” where the investor is forced to sell at the worst possible time. For the average personal investor, avoiding excessive leverage is the most effective way to ensure that a market crash remains a temporary setback rather than a total financial catastrophe.

Strategic Responses: Finding Opportunity in Volatility

While the initial phase of a crash is defined by loss, the subsequent phase is often defined by opportunity. History has shown that market crashes are often followed by periods of significant growth. For the disciplined investor, these periods offer a chance to acquire high-quality assets at “discount” prices.

The Power of Dollar-Cost Averaging

One of the most effective tools for navigating a crash is dollar-cost averaging (DCA). By consistently investing a fixed amount of money at regular intervals, regardless of the price, an investor automatically buys more shares when prices are low and fewer when prices are high. During a crash, DCA allows you to lower your average cost per share. Instead of trying to “time the bottom”—which is nearly impossible even for professionals—DCA ensures that you are continuously building your position as the market searches for a floor.

Portfolio Rebalancing as a Defensive Maneuver

A market crash often throws an investor’s target asset allocation out of alignment. If your goal was a 60/40 split between stocks and bonds, a crash might leave you with a 45/55 split because the value of your stocks fell while your bonds held steady. Rebalancing involves selling some of the “outperforming” assets (bonds) to buy more of the “underperforming” assets (stocks). This counter-intuitive move forces you to “buy low,” positioning the portfolio for maximum gain when the market eventually rebounds.

Identifying Value and “Safe Haven” Assets

Not all assets react to a crash in the same way. Defensive sectors, such as consumer staples, healthcare, and utilities, often hold their value better than cyclical sectors like technology or travel because people still need to buy groceries and medicine regardless of the economy. Additionally, “safe haven” assets like gold or short-term government Treasuries often see increased demand as investors flee equities. Understanding where to park capital during high volatility can help preserve the core of a wealth-building strategy.

The Path to Recovery: Historical Context and Policy Responses

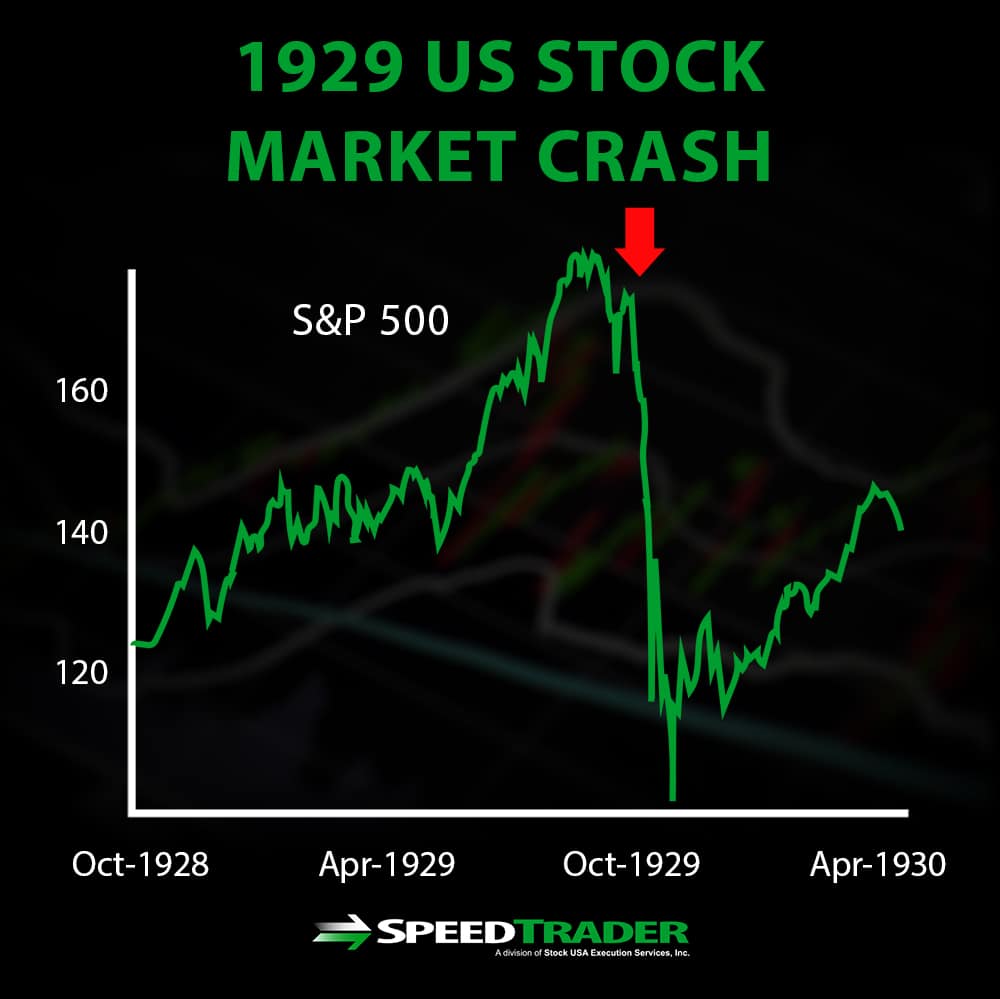

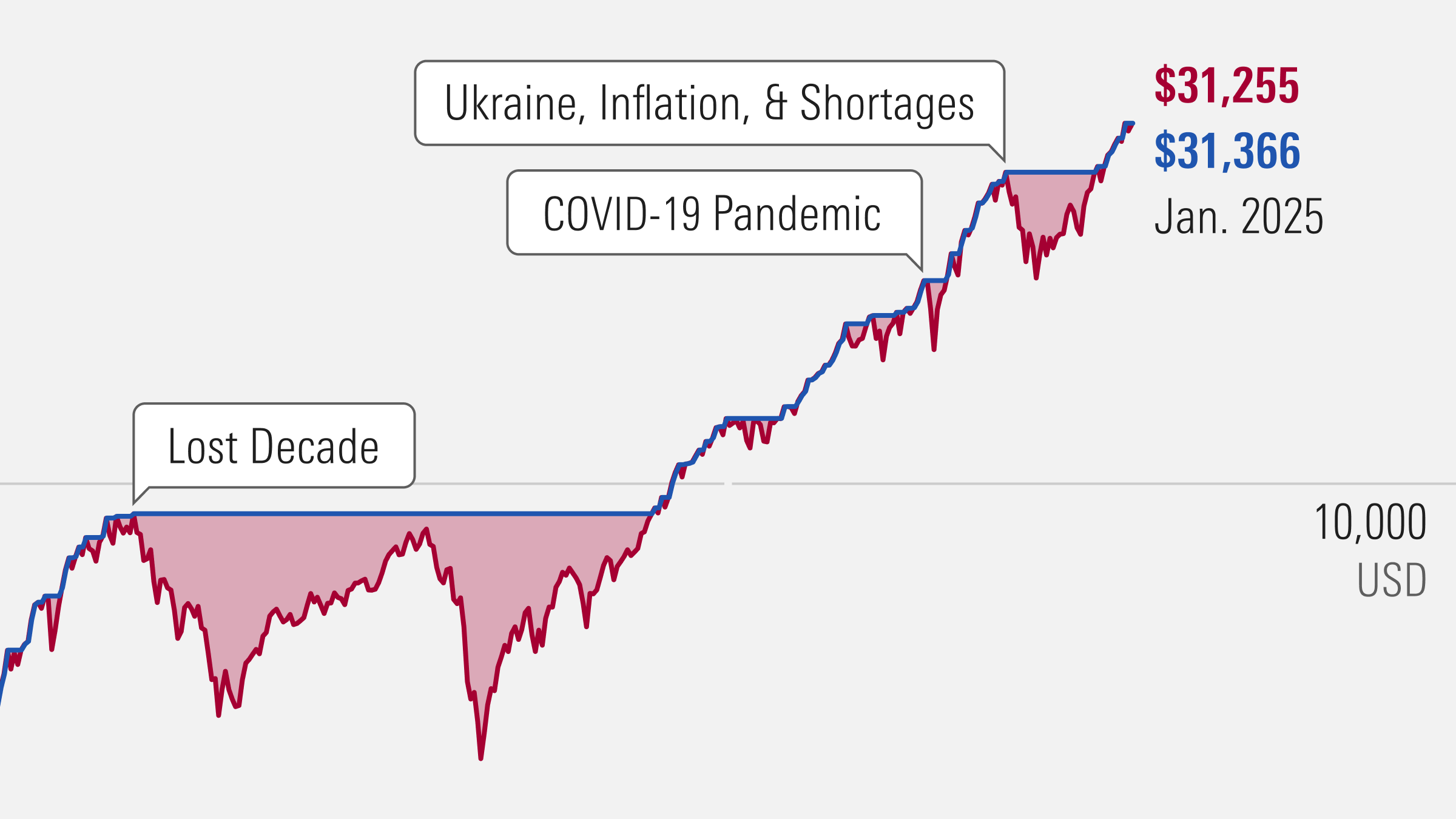

The most important takeaway from every market crash in history—from 1929 to the 2000 dot-com bubble and the 2020 pandemic crash—is that the market has always recovered and eventually reached new highs.

Short-Term Pain vs. Long-Term Resilience

Markets are inherently resilient because they are composed of companies that strive for profit, innovation, and efficiency. While a crash reflects a temporary breakdown in confidence or an adjustment to overvaluation, the long-term trajectory of the stock market is driven by corporate earnings and economic productivity. Investors who maintain a multi-decade horizon view crashes as mere blips on a much longer upward-sloping line. The time it takes for a market to recover varies—sometimes it is months, sometimes years—but the recovery has, to date, always occurred.

The Role of Central Banks and Government Intervention

In the modern era, a stock market crash usually triggers a swift response from central banks, such as the Federal Reserve. To stabilize the economy, they may lower interest rates or engage in quantitative easing (buying bonds to inject liquidity into the system). Governments may also pass fiscal stimulus packages to support struggling industries and citizens. While these interventions can lead to other long-term concerns like inflation or increased national debt, their primary goal is to prevent a market crash from turning into a multi-year economic depression.

Conclusion: Preparing for the Inevitable

The question for investors is not if the market will crash again, but when. Market cycles are a natural part of the capitalist system. By maintaining a diversified portfolio, avoiding excessive leverage, and keeping an emergency fund in cash, you can ensure that you are never a forced seller. A crash is a test of strategy and temperament. Those who view it with a professional, clinical eye—recognizing the difference between a drop in price and a drop in intrinsic value—are the ones who emerge from the volatility with their financial goals intact and their wealth potentially expanded.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.