Securing a small business loan is often the most significant milestone in an entrepreneur’s journey. Whether you are looking to bridge a seasonal cash flow gap, invest in state-of-the-art equipment, or scale your operations to a new market, capital is the fuel that keeps the engine of innovation running. However, the lending landscape has evolved dramatically over the last decade. It is no longer just a matter of walking into a local bank with a handshake and a dream.

Navigating the complexities of business finance requires a strategic approach, a deep understanding of your financial standing, and an awareness of the diverse lending products available in today’s market. This guide provides a roadmap to help you understand the nuances of small business loans, prepare a winning application, and ultimately secure the funding necessary to achieve your corporate objectives.

Understanding the Landscape of Small Business Financing

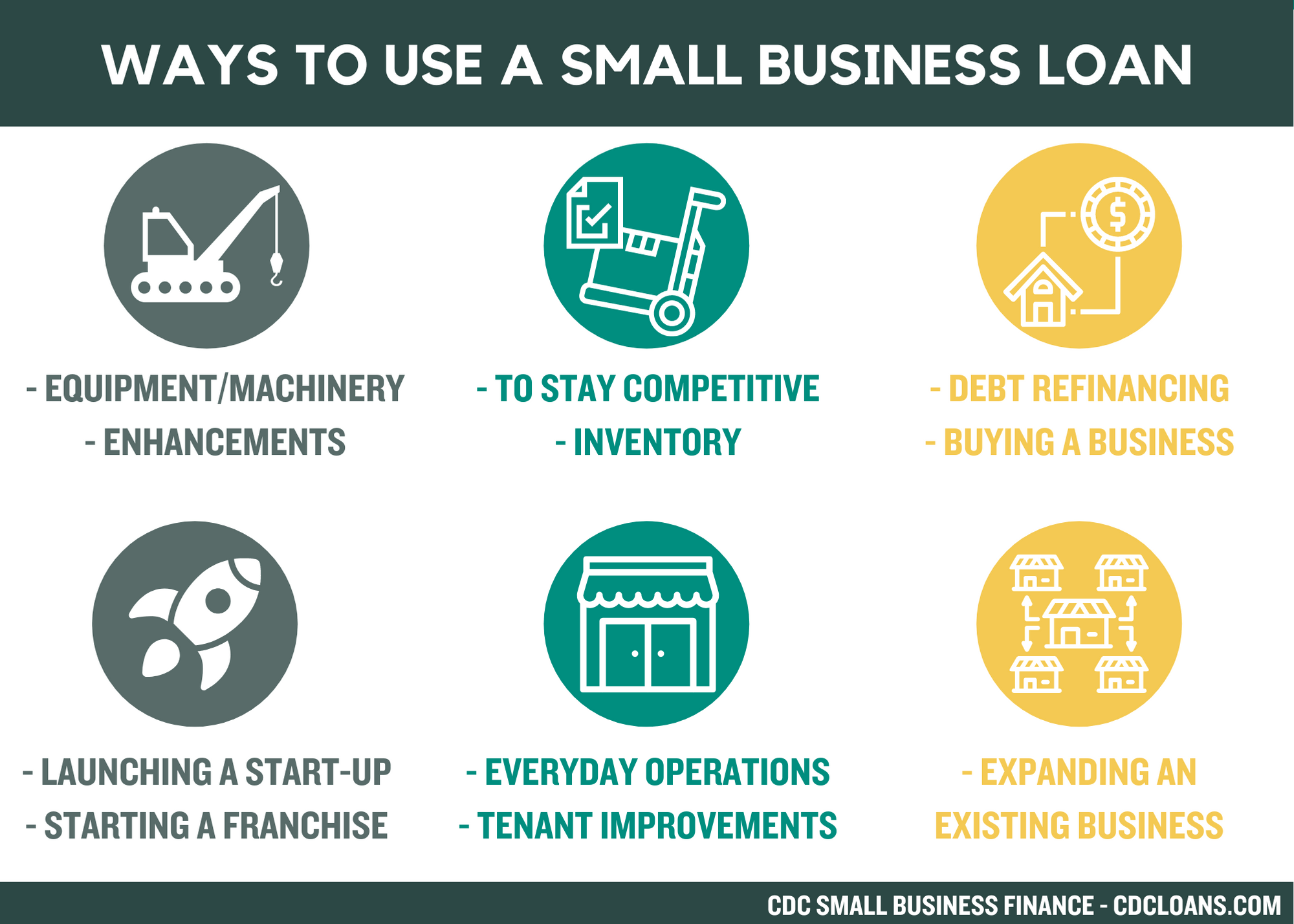

Before you submit a single application, you must identify which type of loan aligns with your specific business needs. Financing is not a one-size-fits-all solution; the wrong type of debt can stifle your growth just as easily as the right type can accelerate it.

Traditional Term Loans and Lines of Credit

Traditional term loans are what most people envision when they think of business borrowing. You receive a lump sum of capital and repay it over a set period with a fixed or variable interest rate. These are ideal for specific, one-time investments like purchasing real estate or acquiring another business.

Conversely, a business line of credit offers more flexibility. It works similarly to a credit card, where you are approved for a maximum amount and can draw from it as needed. You only pay interest on the amount you actually use. This is a premier tool for managing operational cash flow or preparing for unforeseen emergencies.

SBA Loans: The Gold Standard

The U.S. Small Business Administration (SBA) does not lend money directly to entrepreneurs. Instead, it guarantees a portion of the loan provided by participating lenders, reducing the risk for the bank. The SBA 7(a) program is the most popular, offering versatile funding for working capital or debt refinancing. Because of the government guarantee, these loans often feature the most competitive interest rates and longest repayment terms available, though the application process is notoriously rigorous and time-consuming.

Equipment and Invoice Financing

If your capital needs are tied to specific assets, specialized financing might be the most efficient route. Equipment financing uses the equipment itself as collateral, often allowing for easier approval even if your business credit is still developing. Invoice financing (or factoring) allows you to borrow against your outstanding accounts receivable. For B2B companies struggling with 30- or 60-day payment cycles, this provides immediate liquidity based on work already performed.

Evaluating Your Creditworthiness and Financial Health

Lenders are in the business of risk management. To get a “yes,” you must prove that your business is a safe bet. This involves a dual look at both your personal financial history and your business’s performance metrics.

The Importance of Personal and Business Credit Scores

For many small business owners, especially those in the early stages, personal credit is the primary barometer for the lender. A personal FICO score above 680 is generally required for traditional bank loans, while SBA loans may require even higher benchmarks.

Simultaneously, you must build your business credit profile through bureaus like Dun & Bradstreet or Experian Business. Lenders will look at your Paydex score to see how reliably you pay vendors. If your scores are currently low, it may be prudent to spend six months “cleaning up” your reports—paying down revolving debt and correcting errors—before applying for a major loan.

The Five C’s of Credit

Professional lenders evaluate applications based on the “Five C’s”:

- Character: Your personal and professional reputation.

- Capacity: Your ability to repay the loan based on cash flow.

- Capital: The amount of your own money you have invested in the business.

- Collateral: Assets you can pledge to secure the loan.

- Conditions: The external economic environment and the specific purpose of the loan.

Understanding these pillars helps you see your business through the eyes of an underwriter. If you are weak in “Collateral,” you must compensate with exceptional “Capacity” (strong, consistent revenue).

Analyzing Debt-to-Income and Debt-Service Coverage Ratios

Lenders will scrutinize your Debt-Service Coverage Ratio (DSCR). This formula—Net Operating Income divided by Total Debt Service—tells the lender if your business generates enough profit to cover its new loan payments comfortably. A ratio of 1.25 or higher is typically considered healthy. If your ratio is lower, it indicates that a new loan might overextend your finances, leading to a higher probability of rejection.

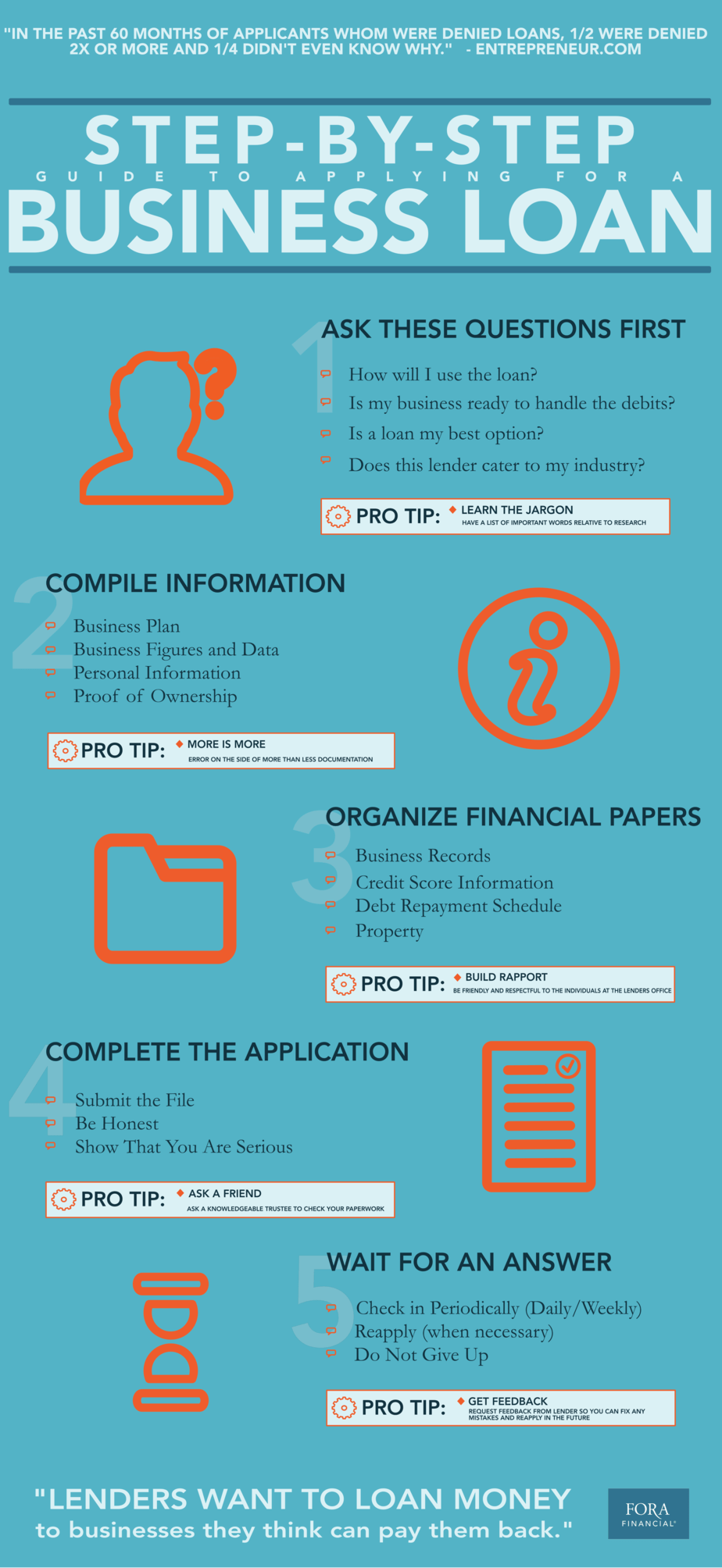

Navigating the Application Process: Documentation and Requirements

Preparation is the difference between a streamlined approval and a frustrating rejection. Small business lending requires an extensive paper trail that proves your business is legitimate, profitable, and well-managed.

Developing a Robust Business Plan

A business plan is not just for startups; it is a vital document for any loan application. It should clearly outline your mission, market analysis, management structure, and—most importantly—how the loan will be used to generate a return on investment. Lenders want to see that you have a strategic vision and that their capital will be used to create growth, not just to plug holes in a sinking ship.

Essential Financial Statements

You will need to provide at least two to three years of both personal and business tax returns. Additionally, you must produce current “internally prepared” financial statements, including:

- Profit and Loss (P&L) Statement: Showing your revenue and expenses over time.

- Balance Sheet: Highlighting your assets, liabilities, and equity.

- Cash Flow Forecast: A forward-looking document showing how you expect money to move through the business over the next 12 months.

Accuracy is paramount here. If your tax returns do not match your P&L statements, it creates a “red flag” regarding your financial transparency.

Legal and Ownership Documents

Lenders will also require proof of legal structure. This includes your Articles of Incorporation, business licenses, operating agreements, and any existing commercial leases. If you have multiple partners, anyone with a 20% stake or higher will likely need to provide personal guarantees and financial disclosures as well.

Comparing Lenders: Traditional Banks vs. FinTech Innovators

The source of your loan is just as important as the terms. Where you choose to apply will dictate the speed of funding, the cost of capital, and the level of personalized service you receive.

The Case for Traditional Banks and Credit Unions

Traditional institutions offer the lowest interest rates and the most stability. They value long-term relationships and may offer better terms if you already hold your business checking and savings accounts with them. However, banks are conservative. They often have higher hurdles for approval and can take several weeks—or even months—to move from application to funding.

The Rise of Online Lenders and FinTech

In the last decade, Financial Technology (FinTech) companies like OnDeck, Bluevine, and Funding Circle have revolutionized the industry. These lenders use sophisticated algorithms to evaluate your creditworthiness in minutes, often focusing on real-time cash flow rather than just credit scores.

The primary advantage of online lenders is speed; you can often receive funds within 24 to 48 hours. The trade-off is the cost. Interest rates (often expressed as factor rates) are significantly higher than those of traditional banks. These loans are best suited for short-term needs or for businesses that cannot qualify for bank financing.

Community Development Financial Institutions (CDFIs)

For minority-owned businesses or those in underserved communities, CDFIs are a powerful resource. These are non-profit lenders focused on economic development. They often offer more flexible underwriting and include mentorship or business coaching as part of the loan package. While they may have smaller loan limits, they are an excellent option for those who find the traditional banking system inaccessible.

Strategies to Increase Your Approval Odds

Securing a loan is a competitive process. To stand out, you must be proactive and demonstrate a high level of financial literacy.

Improving Your Financial Profile Before Applying

If you don’t need the money immediately, spend time optimizing your balance sheet. Reduce outstanding high-interest debt, ensure your accounts receivable are collected promptly to boost your cash balance, and avoid making any large, non-essential purchases that would temporarily lower your liquidity. A “clean” financial year prior to application significantly boosts your credibility.

The Power of the Pitch

When you meet with a loan officer, treat it like a pitch to an investor. Be prepared to explain exactly how the funds will be used. Instead of saying, “I need $100,000 for growth,” say, “I am requesting $100,000 to purchase two high-efficiency CNC machines which will increase our production capacity by 40% and allow us to fulfill a new contract with Company X.” Specificity builds confidence.

Considering Alternative Collateral

If your business lacks significant assets, consider what else you can bring to the table. Some owners use personal real estate as collateral or seek a co-signer with a stronger credit profile. While this increases your personal risk, it can be the “bridge” needed to secure financing that would otherwise be out of reach.

In conclusion, getting a small business loan is a rigorous exercise in financial preparation and strategic alignment. By understanding the various loan products, maintaining a pristine credit profile, and choosing the right lending partner, you can secure the capital necessary to take your business to the next level. Remember, a loan is not just a debt; it is a strategic tool designed to create a future that is more profitable than the present.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.