In an era of economic volatility and shifting market dynamics, the ability to manage personal finances with precision is no longer just a “good habit”—it is a critical survival skill. Budgeting is often misconstrued as a practice of deprivation, a digital ledger of all the things one cannot do. In reality, a well-structured budget is a strategic roadmap that provides the freedom to spend without guilt and the security to face the future without anxiety. To master your money, you must move beyond simple arithmetic and embrace a comprehensive framework of financial discipline, strategic saving, and psychological recalibration.

This guide explores the multidimensional approach to budgeting and saving, offering professional insights into how you can optimize your cash flow, eliminate waste, and build a resilient financial foundation.

1. Establishing a Robust Financial Foundation

Before you can determine where your money should go, you must have an unflinching understanding of where it currently resides. Most financial failures stem from a lack of clarity regarding cash flow—the literal movement of money in and out of your accounts.

Auditing Your Cash Flow

The first step in any sophisticated financial strategy is a comprehensive audit. This involves tracking every cent of income and every penny of expenditure over a 30-to-90-day period. Professional financial planners often categorize these into “Fixed Costs” (mortgage, insurance, utilities) and “Variable Costs” (dining out, entertainment, groceries). By analyzing these patterns, you can identify “leakage”—small, recurring expenses that do not provide significant value but collectively drain your wealth. This audit provides the empirical data necessary to make informed decisions rather than emotional ones.

Defining Your Financial Objectives

A budget without a goal is merely a list of restrictions. To remain motivated, you must align your budget with specific, measurable, achievable, relevant, and time-bound (SMART) objectives. Are you saving for a down payment on a property? Are you aiming for early retirement? Or are you simply looking to eliminate high-interest consumer debt? By attaching a “why” to every dollar you save, the act of budgeting transforms from a chore into a tactical move toward a desired lifestyle.

2. Mastering the Mechanics of Budgeting

Once the foundation is set, you must choose a budgeting methodology that aligns with your personality and financial complexity. There is no one-size-fits-all approach, but several professional frameworks have stood the test of time.

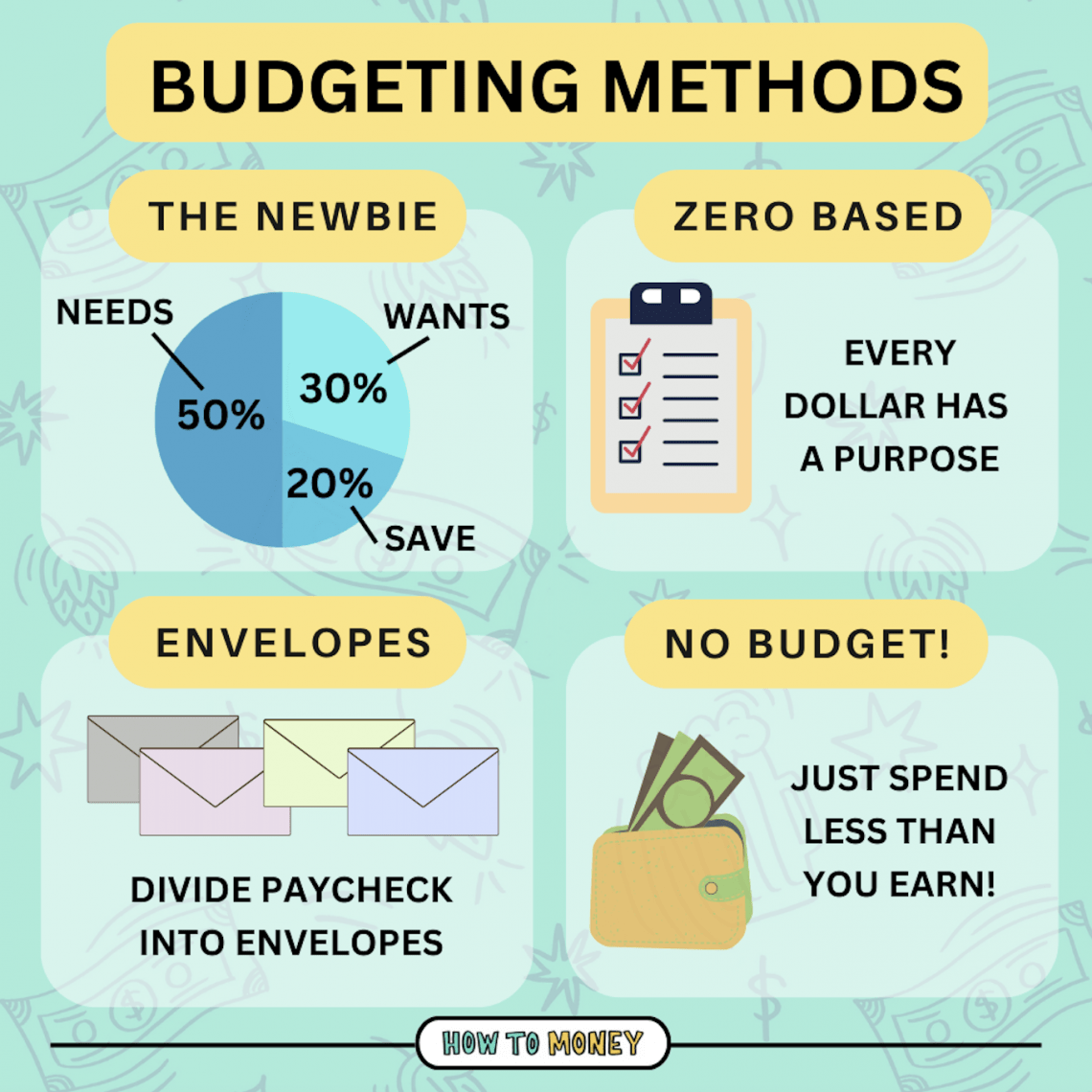

The 50/30/20 Rule

Popularized by financial experts as a baseline for stability, the 50/30/20 rule divides your after-tax income into three distinct buckets:

- 50% for Needs: This covers your essential obligations, such as housing, basic utilities, transportation, and minimum debt payments.

- 30% for Wants: This is your discretionary income. It covers lifestyle choices, such as travel, hobbies, and dining out.

- 20% for Savings and Debt Repayment: This is the “wealth-building” bucket. It includes contributions to retirement accounts, emergency funds, and extra principal payments on debt.

This framework is effective because it forces a balance between living for today and preparing for tomorrow.

Zero-Based Budgeting

For those who prefer granular control, zero-based budgeting is the gold standard. In this system, every single dollar of your income is assigned a specific job. If you earn $5,000 in a month, your expenses, savings, and debt payments must equal exactly $5,000 by the end of the month. This does not mean you have zero dollars in your bank account; it means your “budgeted” balance is zero. This method eliminates “lazy money” and ensures that surplus funds are directed toward productive assets rather than disappearing into mindless spending.

3. Strategic Cost Reduction and Behavioral Shifts

Saving money is not just about choosing the cheapest option; it is about optimizing value and addressing the psychological triggers that lead to overspending.

Optimizing Fixed and Recurring Expenses

While most people focus on cutting out small luxuries like coffee, the most significant impact often comes from optimizing large, recurring expenses. Periodically “shopping” your insurance policies, negotiating internet and cellular contracts, and refinancing high-interest debt can save thousands of dollars annually with minimal effort. Furthermore, the “subscription economy” has created a silent drain on many budgets. An aggressive audit of monthly digital subscriptions—many of which go unused—can instantly increase your monthly surplus.

The Psychology of Mindful Consumption

Saving money is as much a behavioral challenge as it is a mathematical one. We live in a world designed to encourage impulse purchases. To counter this, implement a “48-hour rule” for any non-essential purchase over a certain threshold. This cooling-off period allows the initial dopamine hit of shopping to subside, enabling a rational assessment of whether the item is a need or a fleeting want. By shifting your mindset from “consumerism” to “stewardship,” you begin to view your money as a tool for building freedom rather than a medium for acquiring status symbols.

4. Building a Resilient Savings Ecosystem

A budget tells your money where to go, but a savings ecosystem ensures that your money stays there and grows. This requires a tiered approach to liquidity and risk.

The Emergency Fund: Your Financial Firewall

The most critical component of any financial plan is the emergency fund. This is a dedicated pool of liquid cash intended solely for unforeseen crises, such as medical emergencies, major home repairs, or sudden job loss. Professional consensus suggests maintaining three to six months of essential living expenses in a high-yield savings account (HYSA). This fund acts as a buffer, preventing you from having to dip into long-term investments or take on high-interest debt when life becomes unpredictable.

Automating Wealth Accumulation

The greatest enemy of saving is human friction. If you have to manually transfer money to your savings account every month, you are far more likely to skip a month or spend the surplus. Automation removes the element of choice. By setting up automatic transfers that occur on the day you receive your paycheck, you adopt the “Pay Yourself First” mentality. When your savings and investment contributions are treated as non-negotiable bills, your lifestyle naturally adjusts to the remaining balance, making wealth accumulation effortless and consistent.

5. Leveraging Modern Financial Tools for Oversight

In the digital age, manual spreadsheets—while effective—can be augmented by sophisticated financial technology to provide real-time insights and forecasting.

Utilizing Budgeting and Tracking Applications

Modern financial apps can aggregate data from your bank accounts, credit cards, and investment portfolios to provide a holistic view of your net worth. These tools offer categorized spending reports, identifying trends that might otherwise go unnoticed. Whether it is a simple tracker or a complex AI-driven tool that predicts future cash flow based on historical spending, leveraging technology reduces the cognitive load of financial management. It allows you to spend less time “counting” money and more time “strategizing” with it.

Forecasting and Long-Term Modeling

Budgeting is typically viewed through a monthly lens, but true financial mastery requires a multi-year perspective. Professional budgeting involves “sinking funds”—saving small amounts monthly for large, infrequent expenses like annual taxes, car maintenance, or holiday spending. By forecasting these expenses, you prevent “budget busters” from derailing your progress. Additionally, understanding the power of compound interest allows you to see how a $500 monthly saving, when invested wisely, can transform into a significant retirement corpus over two decades.

Conclusion

Mastering the art of budgeting and saving is not a destination but a continuous process of refinement. It requires the professional discipline to audit your habits, the strategic foresight to plan for the long term, and the psychological resilience to choose delayed gratification over immediate impulses.

By implementing a structured framework like the 50/30/20 rule, automating your savings, and leveraging modern financial tools, you transition from a passive observer of your finances to an active architect of your wealth. Remember: every dollar saved is a seed planted for your future freedom. Start today by taking ownership of your data, defining your goals, and building the systems that will carry you toward permanent financial prosperity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.