The financial landscape is currently defined by a delicate balancing act between cooling inflation, resilient labor markets, and the shifting expectations of central bank policy. As investors and analysts peer into the week ahead, the primary objective is to separate signal from noise. In a market where a single data point can pivot multi-billion dollar portfolios, understanding the underlying currents of the “Money” niche—investing, business finance, and macroeconomic shifts—is essential for any market participant. This week, several key pillars will dictate market movement: the trajectory of interest rates, the robustness of corporate earnings, the volatility of the bond market, and the looming influence of geopolitical developments on commodities.

The Macroeconomic Pulse: Inflation Data and Central Bank Policy

The bedrock of current market valuation rests on the anticipated path of the Federal Reserve and its international counterparts. For the past two years, the narrative has been dominated by “higher for longer,” but as we enter this week’s trading sessions, the focus has shifted toward the timing and magnitude of potential easing.

Deciphering the Consumer Price Index (CPI) and Inflation Sticky Points

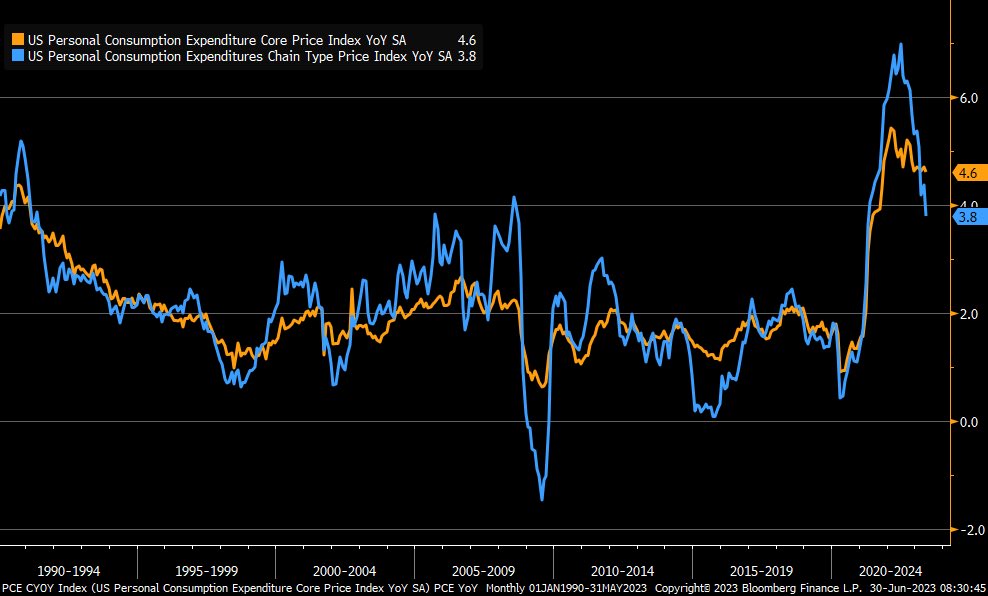

The most critical data point for the week is often the release of inflation metrics. Investors are looking for confirmation that the “last mile” of disinflation is being covered. While goods prices have largely normalized, service-sector inflation—driven by wages and housing costs—remains stubborn. This week, any deviation from the consensus CPI forecast will likely trigger immediate volatility in both equity and currency markets. A higher-than-expected print would force a repricing of rate-cut expectations, potentially strengthening the US Dollar while putting pressure on growth-oriented stocks.

Federal Reserve Rhetoric and Interest Rate Trajectories

Beyond the raw data, the “Fedspeak” scheduled for this week is paramount. Speeches from regional Fed presidents provide the nuanced context that formal statements often lack. Markets are currently looking for clues on the “neutral rate”—the interest rate that neither stimulates nor restrains the economy. If officials maintain a hawkish tilt, emphasizing that the job on inflation isn’t finished, we can expect a tightening of financial conditions. Conversely, any hint of concern regarding the cooling labor market could be interpreted as a precursor to more aggressive rate cuts, providing a tailwind for equities.

Corporate Earnings: The Reality Check for Valuations

While macroeconomic data sets the stage, corporate earnings provide the substance. We are currently in a period where “beats and misses” are scrutinized more for their forward-looking guidance than their past performance. This week’s earnings calendar is packed with bellwether companies that serve as proxies for the broader economy.

The Profitability of Growth and the AI Premium

A significant portion of recent market gains has been concentrated in a handful of mega-cap companies. This week, as several of these titans report, the market will demand justification for their high price-to-earnings (P/E) ratios. Investors are no longer satisfied with the promise of future technology; they are looking for tangible revenue growth derived from capital expenditures in infrastructure and software. If these companies show a margin squeeze or a slowdown in cloud spending, it could lead to a sector-wide rotation out of “growth” and into “value” or “defensive” sectors.

Consumer Discretionary and the Strength of the Household

The health of the consumer remains the ultimate arbiter of the US economy. This week, reports from major retailers and consumer-facing brands will offer a window into household spending power. High interest rates have historically dampened consumer appetite for big-ticket items, but the “excess savings” narrative has kept the economy afloat longer than many predicted. Analysts will be looking at credit card delinquency rates and inventory levels to determine if the consumer is finally beginning to buckle under the weight of sustained inflation.

The Fixed Income Frontier: Bond Yields and the Yield Curve

The bond market is often considered the “smart money” in finance, and its movements this week will be telling. The Treasury market acts as the benchmark for almost all other financial assets, influencing mortgage rates, corporate borrowing costs, and the discount rates used to value stocks.

Understanding the 10-Year Treasury Yield Fluctuations

The 10-year Treasury yield is perhaps the most important number in global finance. This week, as auctions take place and economic data is digested, the movement in the 10-year yield will signal the market’s long-term outlook on growth and inflation. A “bear steepening” of the yield curve—where long-term rates rise faster than short-term rates—would suggest that investors are bracing for a period of higher inflation or increased government debt issuance. On the other hand, a drop in yields might signal a “flight to safety,” indicating that investors are becoming more concerned about a potential recession.

Corporate Credit Spreads and Liquidity

In business finance, the “spread” between government bonds and corporate bonds is a vital measure of risk appetite. Currently, credit spreads are remarkably tight, suggesting that the market sees little risk of widespread corporate defaults. This week, we will look for any widening of these spreads. A widening spread indicates that lenders are becoming more cautious, which can lead to a “liquidity crunch” for smaller, highly leveraged firms that rely on constant refinancing.

Global Geopolitics and the Commodity Conundrum

Financial markets do not operate in a vacuum, and global events have a direct impact on domestic portfolios. Commodities, particularly energy and precious metals, are the primary vehicles through which geopolitical tension manifests in the financial markets.

Energy Markets: The Volatility of Oil and Natural Gas

Energy prices are a double-edged sword for the markets. While rising oil prices can benefit energy sector stocks, they act as a “tax” on the consumer and a driver of headline inflation. This week, supply-side constraints, driven by geopolitical instability in the Middle East and production decisions by OPEC+, will be at the forefront. Any escalation in regional conflicts could send Brent Crude prices higher, complicating the Federal Reserve’s mission and potentially dampening the outlook for transportation and manufacturing industries.

Gold as a Hedge and the Strength of the US Dollar

Gold has traditionally been the ultimate safe-haven asset. In recent weeks, we have seen gold prices reach near-record highs, driven by central bank purchasing and institutional hedging against currency devaluation. This week, the performance of gold in relation to the US Dollar Index (DXY) will be a key indicator of market anxiety. Typically, a strong dollar makes gold more expensive for foreign buyers, leading to a price drop. However, if both the dollar and gold rise simultaneously, it signals a profound lack of confidence in global stability, suggesting that investors are prioritizing capital preservation over growth.

Market Sentiment and Technical Positioning

Finally, successful navigation of the finance markets requires an understanding of investor psychology and technical levels. Fundamentals tell us where the market should go, but sentiment tells us where it will go in the short term.

The Fear Index (VIX) and Volatility Patterns

The CBOE Volatility Index, or VIX, measures the market’s expectation of 30-day volatility. Historically, a VIX below 15 indicates a “complacent” market, while a spike above 20 suggests growing fear. This week, we are looking for any sudden moves in the VIX that might indicate institutional investors are buying “put options” to protect their portfolios against a sudden downturn. High volatility often creates opportunities for active traders, but for the long-term investor, it serves as a warning to maintain a diversified stance.

Support and Resistance: The Technical Ceiling

From a technical perspective, major indices like the S&P 500 and the Nasdaq 100 are testing key psychological levels. This week, the focus will be on whether these indices can break through previous “resistance” levels or if they will bounce off “support” levels. A break below the 50-day moving average, for instance, could trigger algorithmic selling, accelerating a market pullback. Conversely, a strong close above historical highs would signal that the “bull market” has further room to run, fueled by “FOMO” (Fear Of Missing Out) among retail and institutional investors alike.

In conclusion, this week in the finance markets is characterized by a high degree of sensitivity to data and a complex interplay between different asset classes. By keeping a close watch on inflation metrics, corporate guidance, bond yield shifts, and geopolitical headlines, investors can better position themselves to manage risk and capitalize on the opportunities that volatility inevitably brings. Whether you are managing a personal portfolio or overseeing business finance, the key is to remain disciplined, analytical, and ready to adapt to an ever-changing economic environment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.