In the realm of personal finance and real estate investing, few documents carry as much weight as the house deed. For many individuals, a home is the most significant financial asset they will ever own. Understanding the mechanics of how that asset is transferred, protected, and legally recognized is fundamental to sound financial planning. A deed is not merely a piece of paper; it is the physical embodiment of a legal transfer of interest, serving as the cornerstone of property rights in a modern economy.

Whether you are a first-time homebuyer, a seasoned real estate investor, or someone organizing an estate for future generations, understanding the nuances of a house deed is essential. This guide explores the legal definitions, the critical distinctions between titles and deeds, and the various types of deeds that impact your financial liability and asset security.

Understanding the House Deed: The Legal Foundation of Property Ownership

To understand the financial implications of a deed, one must first understand what it is. At its core, a deed is a written legal instrument that transfers the ownership of real property from one party (the grantor) to another (the grantee). In the context of “Money,” the deed represents the official transition of a high-value asset.

Deed vs. Title: Clearing the Confusion

One of the most common misconceptions in personal finance is using the terms “deed” and “title” interchangeably. While they are related, they represent two different concepts. A title is a legal concept representing a bundle of rights—the right to possess, use, and transfer a property. You do not “hold” a title in the physical sense; rather, you have a legal status.

The deed, conversely, is the physical, written document used to transfer those rights. If the title is the abstract concept of ownership, the deed is the vehicle that moves that ownership from person A to person B. Understanding this distinction is vital when performing due diligence during a real estate transaction, as a deed can exist without a “clear title” (one free of liens or disputes), but a title cannot be legally transferred without a valid deed.

Key Components of a Valid Deed

For a deed to be legally binding and recognized by financial institutions and local governments, it must meet several criteria:

- Identification of Parties: The document must clearly name the grantor (seller/giver) and the grantee (buyer/receiver).

- Legal Description: Unlike a simple mailing address, a deed requires a specific legal description of the property, often using “metes and bounds” or “lot and block” surveys.

- Granting Clause: This includes the specific language (such as “convey and warrant”) that indicates the intent to transfer the property.

- Consideration: In a financial context, the deed usually mentions the “consideration,” which is the value exchanged for the property (often the purchase price).

- Execution: The grantor must sign the deed, usually in the presence of a notary public, to ensure the signature is authentic.

Types of Deeds and Their Financial Implications for Investors

From an investment perspective, not all deeds are created equal. The type of deed used in a transaction dictates the level of protection the buyer receives and the level of liability the seller retains. Choosing the wrong deed can lead to significant financial loss if undisclosed claims on the property emerge later.

General Warranty Deeds: The Gold Standard

The general warranty deed offers the highest level of protection for the buyer. In this agreement, the grantor warrants that they own the property clearly and have the right to sell it. Most importantly, the grantor provides a guarantee against any title defects that may have arisen throughout the entire history of the property—even before the grantor owned it. For a homebuyer, this is the most financially secure option, as it legally binds the seller to defend the title against any future claims.

Special Warranty and Quitclaim Deeds: Navigating Risk

Investors often encounter Special Warranty Deeds, particularly in commercial real estate or when buying from a bank (foreclosures). This deed only warrants that the seller has not done anything to encumber the title during their specific period of ownership. It does not protect against issues that occurred before the seller acquired the property.

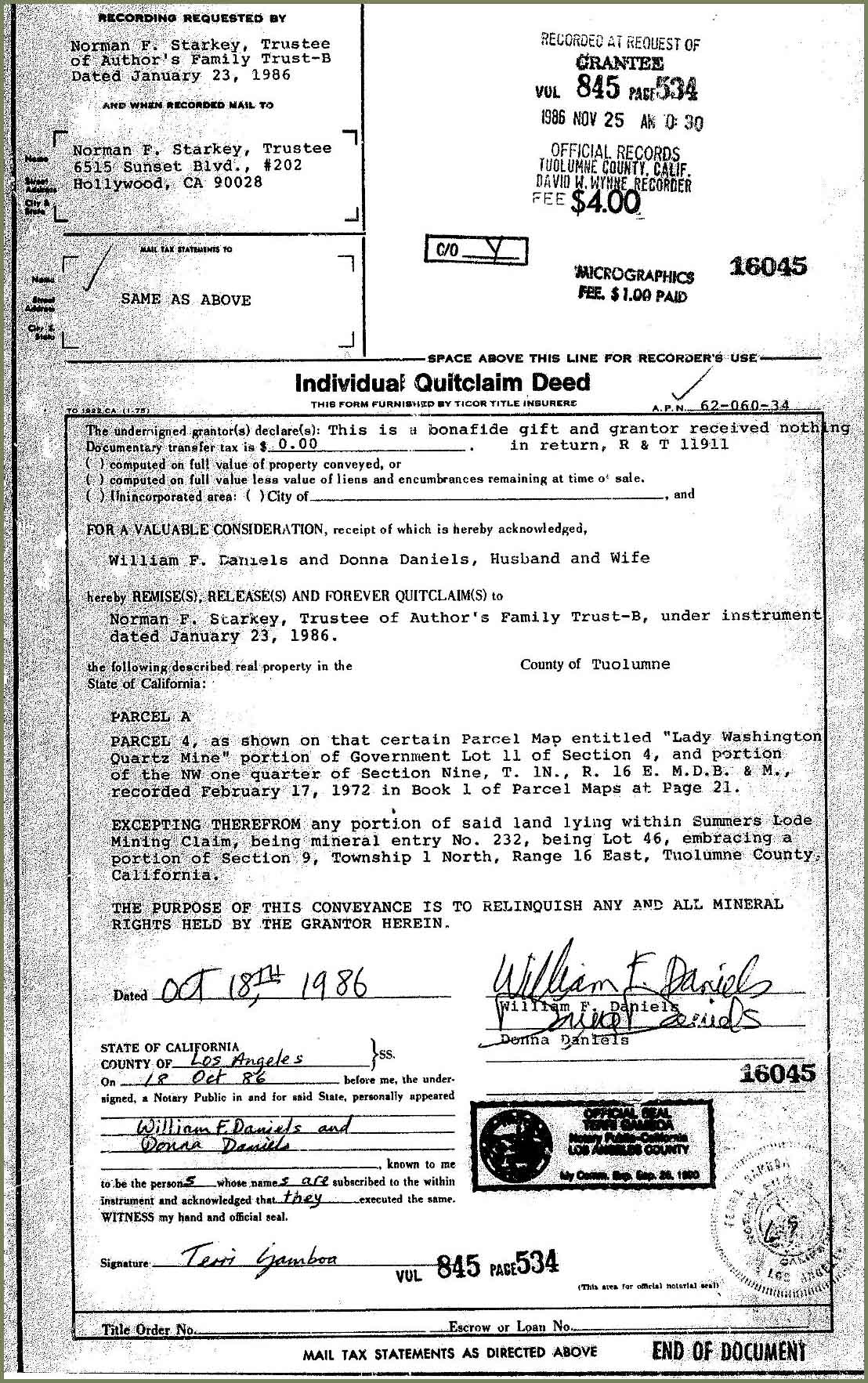

The Quitclaim Deed is the least protective and is rarely used in traditional home sales. It transfers whatever interest the grantor has in the property “as is,” without any promises that the title is clear or even that the grantor owns the property at all. In the world of personal finance, quitclaim deeds are most often used for internal transfers—such as moving a house into a living trust or transferring property between spouses during a divorce. Because they offer no protection, they are high-risk instruments for third-party investments.

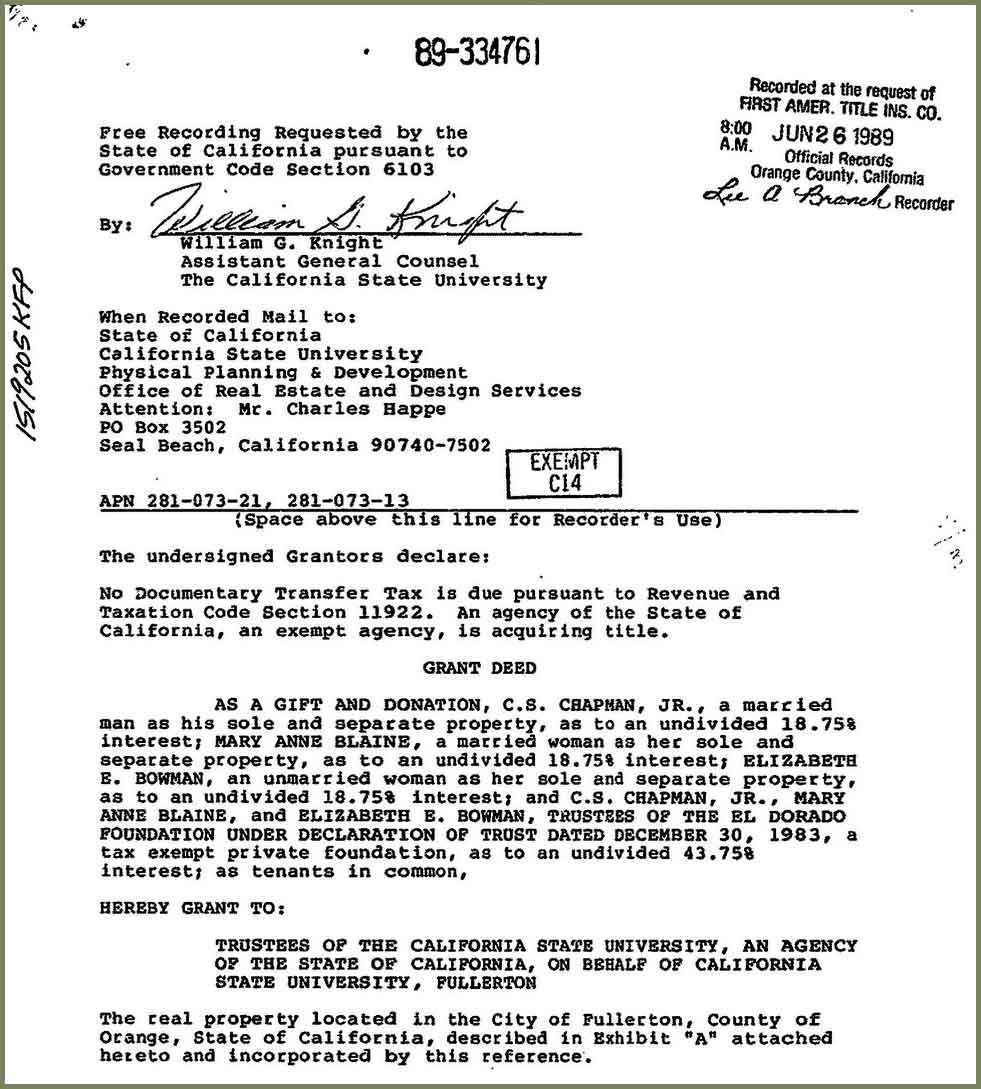

Grant Deeds and Bargain and Sale Deeds

Common in certain states like California, a Grant Deed implies that the grantor has not already sold the property to someone else and that there are no hidden encumbrances. It is a middle ground between a quitclaim and a warranty deed. A Bargain and Sale Deed is similar but usually offers no warranties against liens; it simply implies the grantor has the right to convey the property. These are frequently used in tax sales and foreclosures.

The Financial Process of Executing and Recording a Deed

The creation of a deed is only half of the journey. To ensure the asset is protected from a wealth-management perspective, the deed must be processed and recorded correctly. Failure to follow these steps can lead to “clouds on title,” which can prevent future sales or refinancing.

The Role of Notarization and Delivery

For a deed to be valid, it must be “delivered” and “accepted.” In a legal sense, the grantor must intend to pass the title to the grantee. From a digital security and financial integrity standpoint, notarization is the primary safeguard. The notary verifies the identity of the parties to prevent fraudulent transfers, a critical step in protecting one’s net worth from real estate fraud.

Why Public Recording Is Essential for Asset Protection

Once the deed is signed and notarized, it must be recorded at the local county recorder’s office or register of deeds. This is a crucial step for any property owner. Recording provides “constructive notice” to the world that you are the legal owner.

In the eyes of a lender or a future buyer, an unrecorded deed is a massive red flag. If a deed is not recorded, a dishonest grantor could technically attempt to sell the property to a second buyer. In many jurisdictions, the “race-notice” statute applies, meaning the first person to record the deed is often recognized as the legal owner, regardless of who signed the paperwork first. For an investor, recording the deed is the final act of securing the investment.

Strategic Financial Management: Managing Deeds in Estate Planning and Investment

Understanding deeds is a vital component of long-term financial strategy. How a deed is structured can determine how easily an asset passes to heirs and how much of its value is consumed by legal fees or taxes.

Transfer-on-Death Deeds (TODD)

As part of a modern financial plan, many individuals utilize a Transfer-on-Death Deed. This allows a property owner to name a beneficiary who will automatically receive the property upon the owner’s death, bypassing the lengthy and expensive probate process. For those looking to preserve wealth for the next generation, a TODD is a highly efficient financial tool that keeps the asset out of the courts while maintaining the owner’s control during their lifetime.

The Impact of Liens and Encumbrances on Property Value

A deed is often subject to “encumbrances”—financial claims or limitations on the property. These can include mortgages, tax liens, or mechanic’s liens. When you “take title” via a deed, you need to be certain of what financial burdens are attached to it.

Title insurance is the primary tool used by buyers to mitigate the risks associated with the deed. By paying a one-time premium, the buyer ensures that if a hidden lien or a previous owner’s heir emerges to challenge the deed, the insurance company will cover the legal costs and financial loss. In the context of a 15 or 30-year mortgage, title insurance is a non-negotiable expense for protecting one’s equity.

Conclusion: The Deed as a Pillar of Financial Stability

A deed to a house is far more than a formality of closing day; it is the legal instrument that secures your most significant financial investment. By understanding the differences between various types of deeds—from the robust protection of a General Warranty Deed to the specific utility of a Quitclaim Deed—you can make informed decisions that protect your capital and your family’s future.

In the complex landscape of personal finance, the clarity of your property deed determines the liquidity of your asset, the ease of its transfer, and the security of your ownership. Whether you are building a real estate portfolio or securing a home for your family, a deep understanding of the deed ensures that your wealth remains yours, documented and defended by the full weight of the law. Always consult with a real estate attorney or a financial advisor to ensure your deeds are correctly executed and recorded, cementing your status as a savvy manager of your financial legacy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.