In the contemporary landscape of global commerce, the ability to move capital quickly, securely, and across borders is no longer a luxury—it is a financial necessity. As traditional banking systems grapple with the speed of the digital age, fintech giants have stepped in to bridge the gap. At the forefront of this revolution is PayPal, a platform that has evolved from a simple payment processor into a comprehensive financial ecosystem. Whether you are an individual looking to manage personal expenses, a freelancer seeking to collect international payments, or a budding entrepreneur, understanding how to effectively open and leverage a PayPal account is a critical step in modern financial management.

Understanding PayPal as a Core Pillar of Modern Personal Finance

Before diving into the mechanics of account creation, it is essential to understand where PayPal sits within the broader spectrum of personal finance. Unlike a traditional brick-and-mortar bank, PayPal operates as a digital wallet and a payment intermediary. It provides a layer of insulation between your primary bank account and the vast, sometimes unpredictable, world of online vendors.

The Evolution of Digital Wallets

The concept of a “digital wallet” has transformed significantly over the last decade. Initially, these tools were seen merely as conveniences for online shopping. Today, they serve as sophisticated hubs for capital management. PayPal allows users to hold balances in multiple currencies, earn interest through affiliated savings goals, and even explore cryptocurrency markets. By opening an account, you are essentially adopting a financial tool that prioritizes liquidity and accessibility, two of the most important factors in achieving financial flexibility.

Why PayPal Remains a Leading Financial Tool

Despite the emergence of numerous competitors, PayPal maintains its dominance due to its ubiquitous acceptance and its robust “Purchase Protection” programs. From a money-management perspective, this protection acts as a form of insurance for your liquid assets. When you pay through PayPal, you are not just transferring digits; you are engaging in a transaction backed by a dispute resolution framework that traditional wire transfers or debit card transactions often lack. This peace of mind is a cornerstone of sound personal finance.

Step-by-Step: Establishing Your Financial Gateway

Opening a PayPal account is a straightforward process, yet it requires a strategic approach to ensure the account is tailored to your specific financial goals. The first decision you make during the signup process will dictate your fee structure, your tax reporting requirements, and your access to professional financial tools.

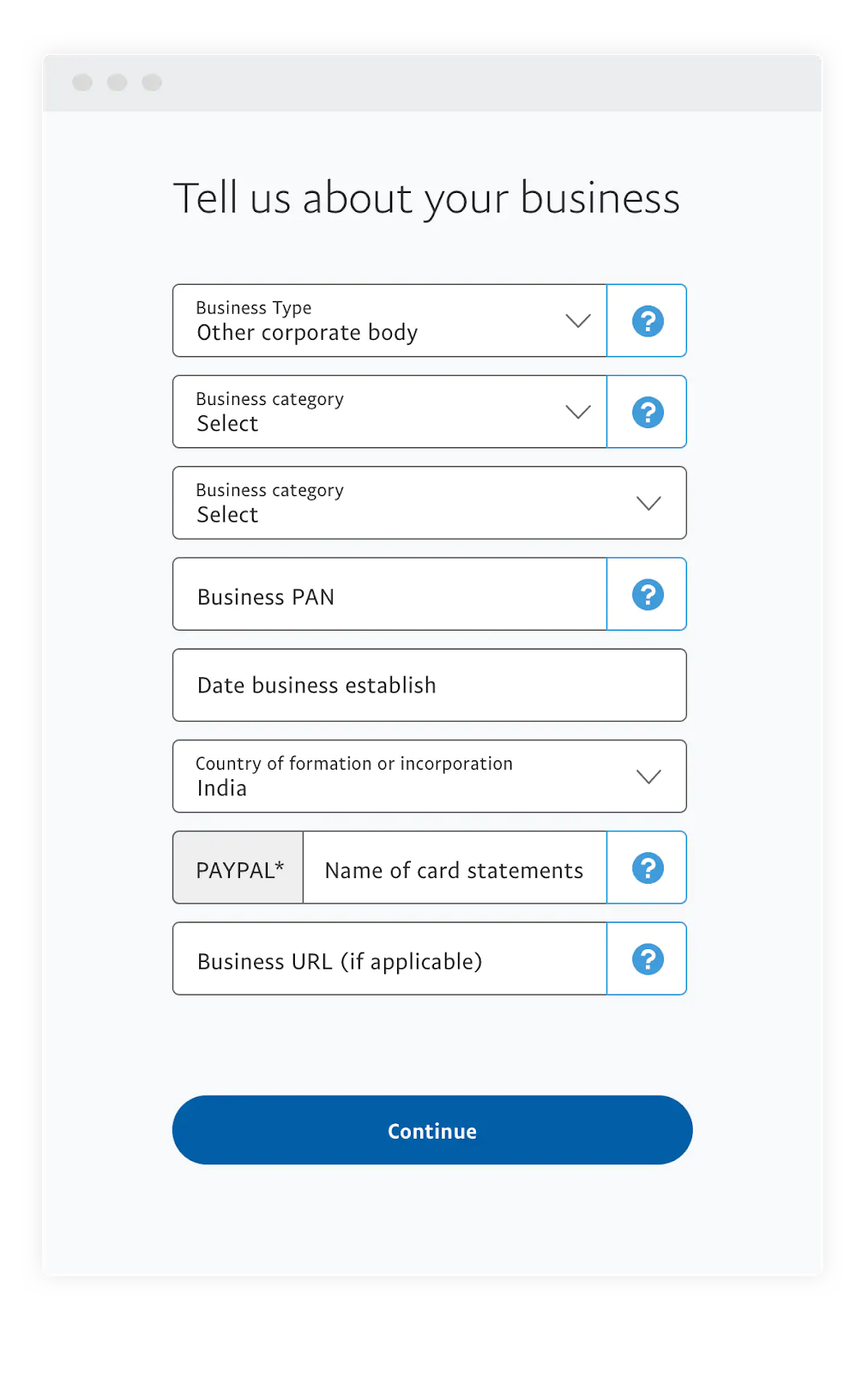

Choosing Between Personal and Business Accounts

PayPal offers two primary account types: Personal and Business. For the majority of users who wish to shop online or send money to friends and family, a Personal Account is the most efficient choice. It offers the lowest barrier to entry and minimal fees for standard domestic transactions.

However, if your goal is to generate online income—whether through a side hustle, e-commerce, or freelance consulting—a Business Account is indispensable. This account type allows you to operate under a company name, provides access to advanced invoicing tools, and allows for multi-user access for employees. From a financial organization standpoint, keeping your business income separate from your personal spending is the “Golden Rule” of accounting, and a PayPal Business account facilitates this separation effortlessly.

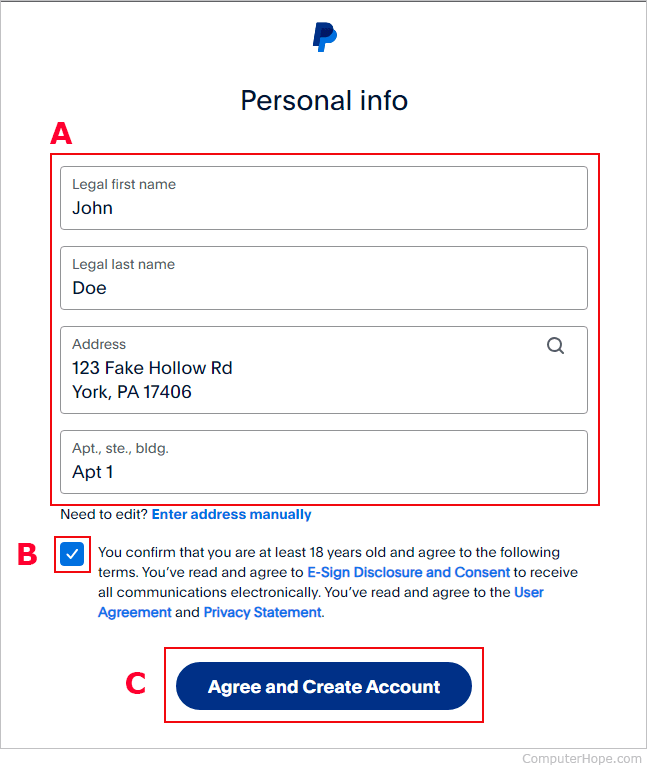

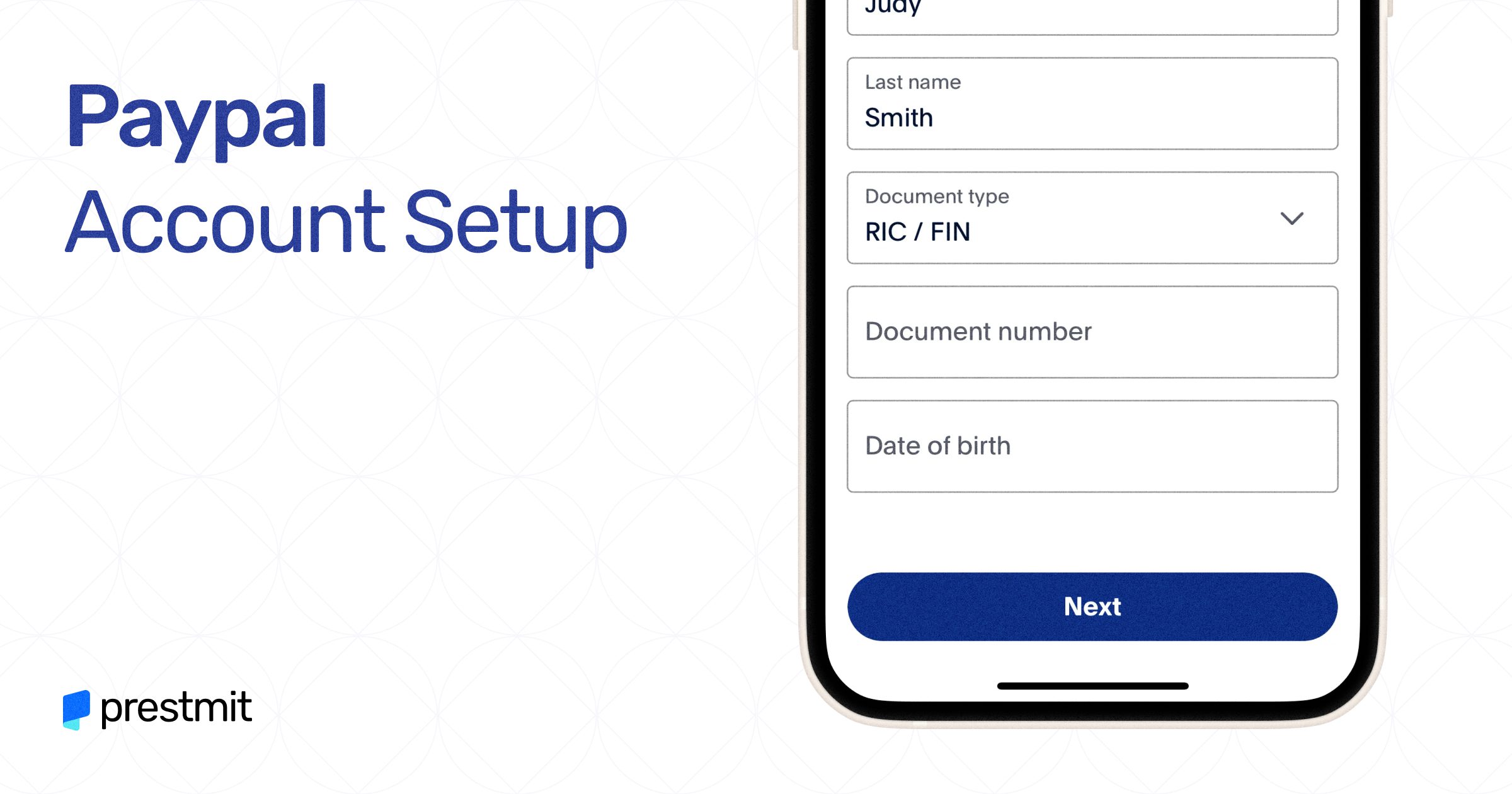

The Registration Process and Verification Requirements

To begin, you will need to provide a legal name, a valid email address, and a secure password. However, the process does not end there. To unlock the full potential of the account and remove initial transfer limits, PayPal requires identity verification. This is a standard “Know Your Customer” (KYC) protocol required by financial regulators to prevent money laundering. You will likely need to provide your Social Security Number (in the U.S.) or equivalent national tax identification elsewhere. Providing this information accurately is vital; any discrepancy between your PayPal data and your legal documents can lead to frozen funds—a situation every savvy financial manager wants to avoid.

Securing and Linking Your Financial Assets

An empty PayPal account is of little use. To make it functional, you must bridge it with your existing financial infrastructure. This involves linking your bank accounts, debit cards, and credit cards. Each of these connections serves a different strategic purpose in your overall money management plan.

Connecting Bank Accounts and Credit Cards

When you link a bank account, you enable the ability to “sweep” your PayPal balance into your primary savings or checking account. This is essential for maintaining liquidity. On the other hand, linking a credit card can be a strategic move for those who utilize “points” or “cashback” ecosystems. By paying through PayPal via a rewards-based credit card, you often retain your card’s benefits while gaining PayPal’s extra layer of security.

It is important to understand the hierarchy of funding sources. PayPal typically defaults to your PayPal balance first, followed by your linked bank account, and finally your cards. Mastering this hierarchy allows you to control exactly which “bucket” of money you are dipping into for specific purchases.

Best Practices for Financial Security and Fraud Prevention

In the realm of digital finance, security is the highest priority. Once your account is open, enabling Two-Factor Authentication (2FA) is non-negotiable. This adds a physical layer of security—usually a code sent to your mobile device—ensuring that even if your password is compromised, your funds remain safe.

Furthermore, users should be wary of “Phishing” scams. PayPal will never ask for your password via email. Developing a habit of checking the sender’s address and navigating directly to the PayPal website, rather than clicking links, is a fundamental skill in protecting your digital net worth.

Navigating the Economics of PayPal

A crucial aspect of financial literacy is understanding the cost of the tools you use. While PayPal is “free” to join, it operates on a sophisticated fee structure that can impact your bottom line if not managed carefully.

Understanding Fees and Currency Conversions

Sending money to friends and family within the same country is generally free if funded by a bank account or PayPal balance. However, the financial dynamics change when it comes to “Goods and Services” transactions. For sellers, PayPal charges a percentage of the transaction plus a fixed fee.

Currency conversion is another area where costs can accumulate. PayPal applies its own exchange rate, which typically includes a spread (a percentage above the mid-market rate). For those involved in international business, these spreads can add up. A sophisticated user will monitor these rates and determine whether it is more cost-effective to hold the foreign currency in their PayPal wallet or convert it during a period of favorable market fluctuations.

Managing Cash Flow and Instant Transfers

For many, the speed of access to funds is paramount. Standard transfers from PayPal to a bank account typically take 1–3 business days and are free. However, PayPal also offers “Instant Transfers” to eligible debit cards or bank accounts for a small fee. From a cash-flow management perspective, this is a valuable tool during emergencies. However, relying on instant transfers for every transaction can bleed a significant percentage of your income over time. Budgeting for the 3-day wait is almost always the more fiscally responsible choice.

Leveraging PayPal for Wealth Building and Online Income

Once the account is established and secured, it becomes a powerful engine for building wealth. PayPal is not just a place to spend money; it is one of the most accessible gateways to the global “gig economy.”

Receiving Payments for Side Hustles

For individuals looking to diversify their income streams, PayPal is often the default payment method for platforms like Upwork, eBay, and various affiliate marketing networks. The ability to generate professional invoices directly through the PayPal interface allows even the smallest “side hustle” to operate with the financial sophistication of a larger corporation. These invoices provide a clear paper trail, which is essential for tax season and for tracking the growth of your secondary income.

PayPal as a Tool for Disciplined Budgeting

Finally, PayPal can be used as a strategic budgeting tool. By allocating a specific amount of “discretionary spending” money to your PayPal balance each month, you can create a hard limit on your online shopping. Once the PayPal balance is zero, the “fun budget” is exhausted. This separation of funds helps prevent the “lifestyle creep” that often occurs when all spending is pulled from a single primary checking account.

In conclusion, opening a PayPal account is more than a technical task; it is a foundational move in establishing a modern financial identity. By choosing the right account type, securing your assets with 2FA, and understanding the underlying fee structures, you transform a simple app into a robust financial command center. In an era where digital agility defines financial success, mastering PayPal is an essential step toward achieving greater control over your economic future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.