Indiana state income tax is a crucial aspect of personal finance for residents and individuals who earn income within the Hoosier State. Understanding its intricacies, from how it’s calculated to how it impacts your overall financial picture, is essential for effective financial planning and compliance. This article will delve into the core components of Indiana’s income tax system, providing clarity and actionable insights for taxpayers.

Understanding the Basics of Indiana State Income Tax

Indiana’s approach to income tax has evolved over time, and grasping the fundamental principles is the first step toward mastering your tax obligations. This section will cover the essential elements of what constitutes Indiana state income tax and who is subject to it.

What is Indiana Adjusted Gross Income (AGI)?

At the heart of Indiana state income tax lies the concept of Adjusted Gross Income (AGI). Similar to the federal system, Indiana uses AGI as the starting point for calculating your tax liability. It’s essentially your gross income from all sources, minus specific allowable deductions. Understanding what counts as income and what deductions are permitted is vital.

Sources of Income Subject to Indiana Tax

Indiana taxes a broad range of income sources. This includes, but is not limited to:

- Wages and Salaries: Income earned from employment is a primary source of taxable income.

- Self-Employment Income: Profits generated from operating a business or working as an independent contractor are subject to Indiana income tax.

- Interest and Dividends: Income received from investments like savings accounts, bonds, and stocks is generally taxable.

- Retirement Income: Pensions, annuities, and distributions from retirement accounts are typically considered taxable income. However, certain retirement benefits, like Social Security and military retirement pay, are exempt.

- Rental Income: Net income derived from real estate rentals is taxable.

- Capital Gains: Profits realized from the sale of assets such as stocks, bonds, or real estate are also subject to taxation.

It’s important to note that Indiana does not tax all forms of income. As mentioned, Social Security benefits and military retirement pay are exempt. Additionally, certain other benefits or income streams might have specific exemptions or exclusions defined by Indiana tax law.

Common Indiana Income Tax Deductions

While Indiana aims for a broad tax base, it does allow for certain deductions to reduce your taxable income. These deductions can significantly lower your overall tax burden. Common Indiana deductions include:

- Dependent Exemptions: For each qualifying dependent, taxpayers can claim a deduction. The amount of this exemption is set annually by the state legislature.

- Personal Exemption: A deduction is allowed for the taxpayer themselves and, if married, for their spouse.

- Military Spouse Residency Relief Act (MSRRA) Income: Income earned by a military spouse who is not a resident of Indiana but whose spouse is stationed in Indiana is exempt from Indiana income tax.

- Certain Retirement Income: While some retirement income is taxable, specific types like Social Security and military retirement pay are exempt.

- Contributions to College Savings Plans: Indiana offers tax benefits for contributions to state-sponsored college savings plans, such as Indiana’s 529 plan.

The specific deduction amounts and eligibility criteria are subject to change, so it’s crucial to consult the latest Indiana Department of Revenue (IDR) guidelines or a tax professional.

Who Must File an Indiana State Income Tax Return?

Generally, any individual who earns income in Indiana is required to file a state income tax return. This includes:

- Indiana Residents: If you live in Indiana and earn income, regardless of where that income is earned, you are subject to Indiana income tax.

- Non-Residents with Indiana Source Income: If you do not live in Indiana but earn income from sources within the state (e.g., working a job physically located in Indiana, owning rental property in Indiana), you may be required to file.

- Part-Year Residents: If you moved into or out of Indiana during the tax year, you will likely need to file a part-year resident return.

There are certain income thresholds below which you may not be required to file. However, even if you are not required to file, you might want to file to claim a refund if you had taxes withheld from your paycheck.

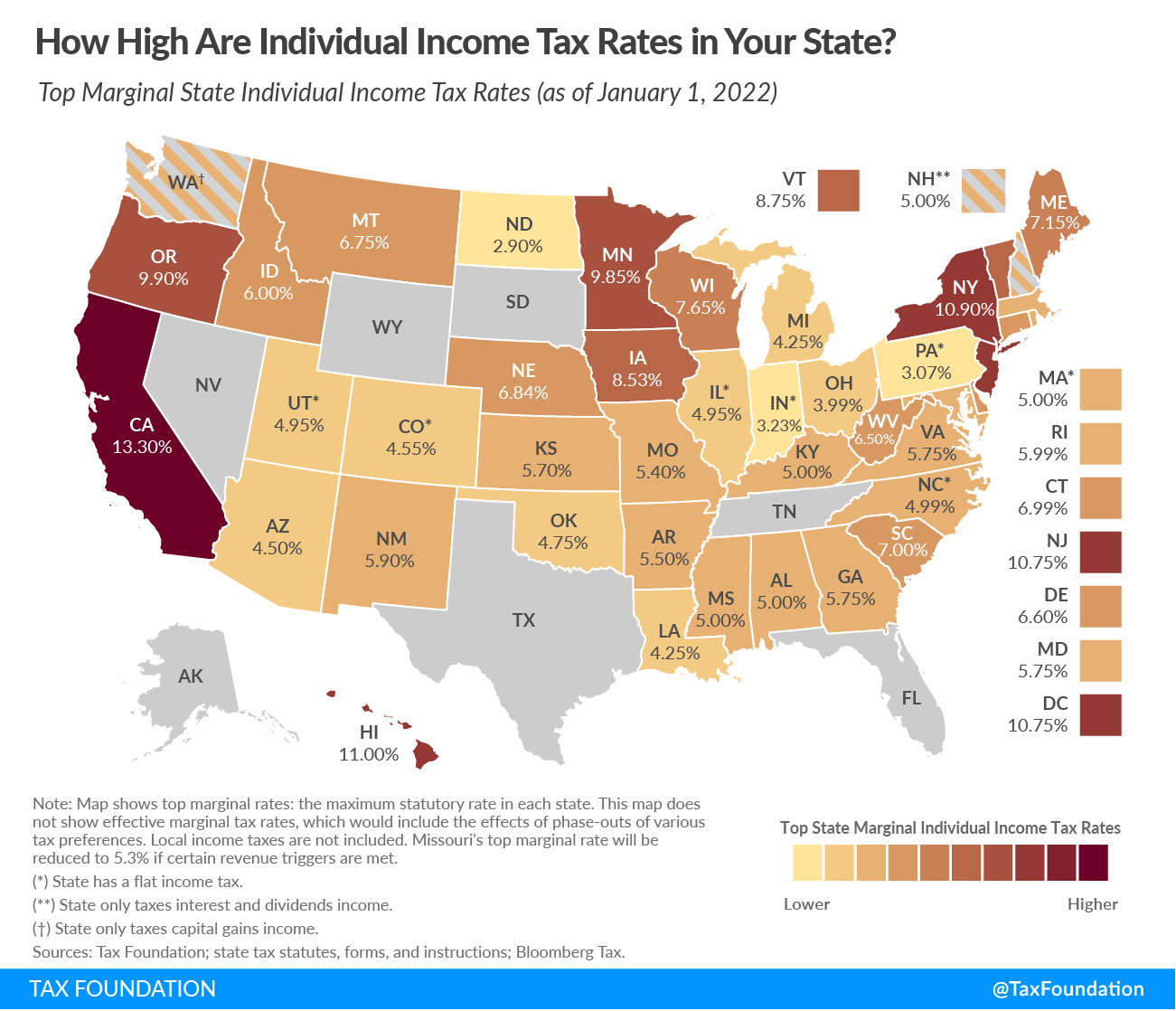

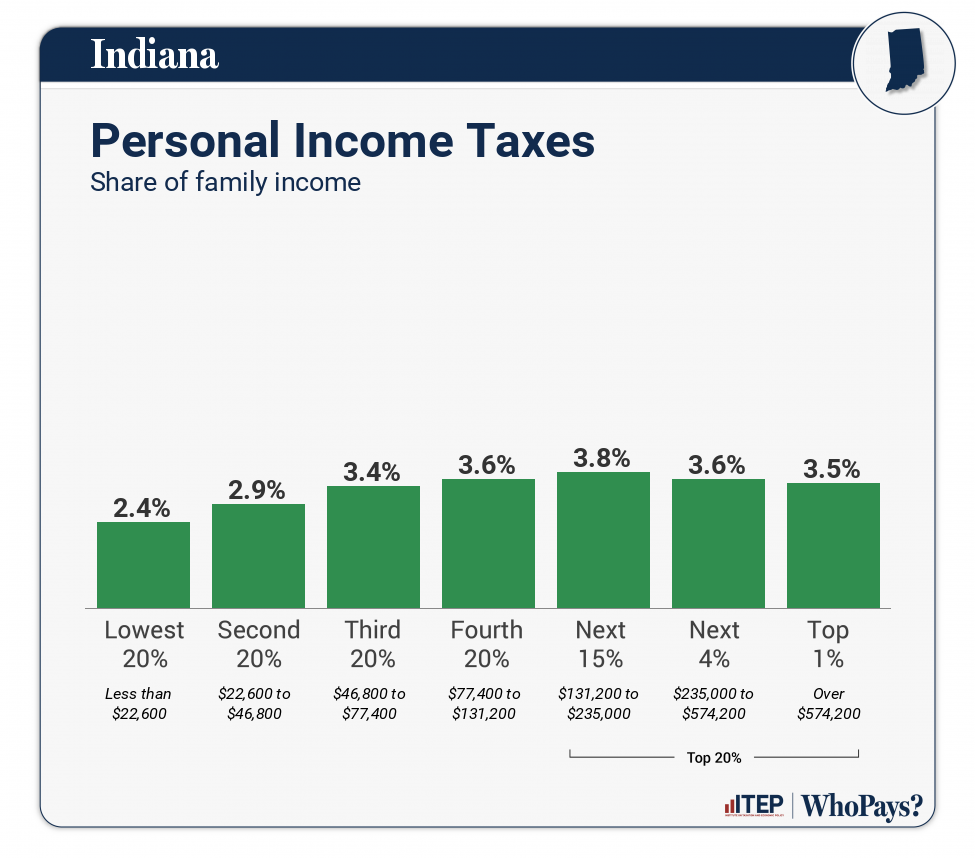

Indiana’s Income Tax Rate and Structure

Indiana’s income tax system is characterized by its flat tax rate, a feature that distinguishes it from states with progressive tax structures. This section will explore the current tax rate and the implications of a flat tax system.

The Indiana Flat Tax Rate

As of recent tax years, Indiana operates under a flat income tax rate. This means that all taxpayers, regardless of their income level, are taxed at the same percentage rate. This contrasts with progressive tax systems, where higher earners pay a larger percentage of their income in taxes.

The flat tax rate is a key policy decision that influences the distribution of the tax burden across the state’s population. Proponents often argue for its simplicity and fairness, suggesting it encourages economic activity by not penalizing higher earners. Opponents might argue that it disproportionately benefits higher-income individuals and places a heavier relative burden on lower-income taxpayers.

The specific flat tax rate has been subject to legislative adjustments over time. Staying informed about the current rate is crucial for accurate tax calculations. The IDR website is the official source for the most up-to-date tax rate information.

Implications of a Flat Tax System

The adoption of a flat tax has several implications for Indiana taxpayers:

- Simplicity: A flat tax simplifies tax calculations. There’s no need to determine which tax bracket your income falls into, making tax preparation potentially less complex.

- Predictability: For individuals and businesses, a flat tax rate offers a degree of predictability in tax planning.

- Distributional Effects: As noted, the flat tax tends to be more favorable to higher-income individuals, as they pay the same rate as lower-income individuals but on a much larger income base. This can lead to discussions about tax fairness and equity.

- Revenue Generation: The state’s revenue from income tax is directly tied to the chosen flat rate and the overall income earned within the state. Adjustments to the rate have a direct impact on state revenues.

Understanding these implications helps taxpayers contextualize their tax liability within the broader economic and social framework of Indiana.

Filing Your Indiana State Income Tax Return

The process of filing your Indiana state income tax return involves several steps, from gathering necessary documents to choosing your filing method. This section will guide you through the essential aspects of the filing process.

Key Documents and Information Needed

Before you begin filing, ensure you have gathered all the necessary documents and information. This typically includes:

- Social Security Numbers: For yourself, your spouse, and any dependents.

- Income Statements:

- W-2 Forms: From employers, detailing wages earned and taxes withheld.

- 1099 Forms: For various types of income, such as freelance work (1099-NEC), interest (1099-INT), dividends (1099-DIV), retirement distributions (1099-R), and unemployment compensation (1099-G).

- Records of Deductions and Credits: Any documentation supporting the deductions and credits you plan to claim, such as receipts for contributions, records of education expenses, or proof of business expenses.

- Previous Year’s Tax Return: This can be helpful for reference, especially when dealing with carryovers or consistent deductions.

- Bank Account Information: For direct deposit of refunds or direct debit of payments.

Having all these documents readily available will streamline the filing process and reduce the likelihood of errors.

Filing Methods: Online, Mail, and Professional Assistance

Indiana offers several convenient methods for filing your state income tax return:

- Online Filing (E-filing): This is the most popular and often the fastest method. You can e-file directly through the Indiana Department of Revenue (IDR) website using their free online portal for simple returns, or through various tax software providers (e.g., TurboTax, H&R Block, TaxAct) that support Indiana e-filing. E-filing generally results in faster refunds and provides immediate confirmation of submission.

- Filing by Mail: If you prefer to file by paper, you can download tax forms from the IDR website or obtain them from local tax offices. You’ll need to complete the forms accurately and mail them to the address specified by the IDR. This method typically takes longer for processing and refunds.

- Professional Tax Preparer: For those with complex tax situations or who prefer expert assistance, engaging a Certified Public Accountant (CPA) or an Enrolled Agent (EA) is a viable option. They can help ensure accuracy, identify all eligible deductions and credits, and file the return on your behalf.

Important Dates and Deadlines

The Indiana state income tax filing deadline generally aligns with the federal deadline, typically April 15th of each year. However, if April 15th falls on a weekend or a holiday, the deadline is extended to the next business day.

It is crucial to be aware of other important dates as well:

- Estimated Tax Payments: If you are self-employed or have income not subject to withholding, you may need to make quarterly estimated tax payments throughout the year. The deadlines for these payments are usually in April, June, September, and January.

- Extensions: If you cannot file by the deadline, you can request an extension. An extension to file is generally automatic if you obtain a federal extension. However, it’s important to remember that an extension to file is not an extension to pay. Any tax due must still be paid by the original deadline to avoid penalties and interest.

Missing deadlines can result in penalties and interest charges, so it’s vital to mark these dates on your calendar and plan accordingly.

Utilizing Credits and Incentives for Indiana Taxpayers

Beyond deductions, Indiana offers various tax credits and incentives designed to encourage specific economic activities, support families, and provide relief to certain taxpayer groups. Understanding and leveraging these can further reduce your tax liability.

Common Indiana Tax Credits

Tax credits are often more valuable than deductions because they directly reduce your tax liability dollar-for-dollar. Some commonly available Indiana tax credits include:

- Homestead Credit: This credit is designed to reduce property taxes for homeowners. While it’s a property tax credit, it’s administered through the state’s tax system, and understanding eligibility is important for homeowners.

- Property Tax Replacement Credit (PTRC): This credit also aims to offset property taxes by reducing your state income tax liability.

- Earned Income Tax Credit (EITC): Indiana’s EITC is a refundable tax credit for low-to-moderate income working individuals and families. Its value is tied to the federal EITC.

- Child and Dependent Care Credit: Similar to the federal credit, this allows taxpayers to claim a credit for expenses paid for the care of qualifying dependents to allow them to work or look for work.

- Other Industry-Specific Credits: Indiana may offer credits for specific industries or activities, such as those related to research and development, job creation, or investment in certain businesses.

The availability and specific requirements for these credits can change based on legislative updates. Consulting the IDR’s publications or a tax professional is recommended to ensure you are claiming all eligible credits.

Understanding Incentives for Economic Development and Investment

Indiana actively promotes economic growth through various incentives. While some are geared towards businesses, certain individual investments or actions might also qualify for state-level incentives that can impact your tax obligations.

- Indiana’s 529 College Savings Plan (Indiana CollegeChoice): Contributions to this plan may offer state tax advantages. Depending on the plan structure and legislative changes, you might be able to deduct contributions or benefit from tax-free growth and withdrawals for qualified education expenses.

- Investment Incentives: While less common for individual income tax, certain state-sponsored investment programs or initiatives might provide tax benefits for residents who invest in Indiana-based businesses or funds.

Staying informed about Indiana’s economic development initiatives and their potential tax implications can be beneficial for long-term financial planning.

Staying Current and Seeking Professional Guidance

The landscape of tax laws is constantly evolving. What was true last year might be different this year, making continuous learning and seeking expert advice crucial for accurate tax management.

The Importance of the Indiana Department of Revenue (IDR)

The Indiana Department of Revenue (IDR) is the primary source of official information regarding state income tax. Their website (in.gov/dor) provides:

- Tax Forms and Publications: Access to all necessary forms, instructions, and detailed publications explaining various aspects of Indiana tax law.

- Tax Rate Updates: Information on current income tax rates and any changes.

- Filing Deadlines and Requirements: Clear guidance on when and how to file.

- News and Alerts: Updates on legislative changes or important tax-related announcements.

Regularly visiting the IDR website, especially around tax season, is a fundamental step in staying compliant.

When to Consult a Tax Professional

While many taxpayers can manage their Indiana state income tax returns effectively on their own, certain situations warrant professional assistance:

- Complex Income Sources: If you have significant income from self-employment, rental properties, investments, or foreign sources, a tax professional can help navigate the complexities and ensure all income is reported correctly.

- Significant Life Changes: Major life events like marriage, divorce, the birth of a child, starting a business, or inheriting assets can significantly impact your tax situation and may require expert advice.

- Eligibility for Credits and Deductions: If you are unsure about your eligibility for various credits and deductions, a tax professional can identify opportunities to reduce your tax liability.

- Facing an Audit: If you are selected for an audit by the IDR, having a tax professional represent you can be invaluable.

- Desire for Tax Planning: Beyond filing, a tax professional can help with year-round tax planning to minimize your tax burden legally.

In conclusion, understanding Indiana state income tax is a vital component of personal finance. By familiarizing yourself with its structure, filing requirements, and available credits, you can effectively manage your tax obligations and contribute to your financial well-being. Always refer to official sources like the Indiana Department of Revenue and consider professional guidance when needed to ensure accuracy and optimize your financial outcomes.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.