Navigating the landscape of federal taxation is a fundamental pillar of personal and business finance. For many, the realization that taxes are due brings a sense of urgency and, occasionally, confusion regarding the most efficient ways to settle a debt with the Internal Revenue Service (IRS). In the modern financial era, the methods available for tax remittance have evolved far beyond the traditional paper check. Today, taxpayers have access to a suite of digital tools, installment options, and third-party payment processors designed to streamline the process.

Understanding how to pay the IRS is not merely a matter of compliance; it is an essential skill in financial management. Choosing the right payment method can affect your cash flow, your eligibility for certain protections, and your overall peace of mind. This guide provides a deep dive into the various channels available for tax payments, the strategic implications of each, and how to manage your liabilities if you cannot pay in full.

The Digital Frontier: Electronic Payment Methods

The IRS has made significant strides in digitizing its collection processes. Electronic payments are generally preferred because they offer immediate confirmation, reduce the risk of mail theft, and minimize processing errors. For the financially savvy taxpayer, these digital tools are the first line of defense in maintaining a clean record with the treasury.

IRS Direct Pay: The Gold Standard for Individuals

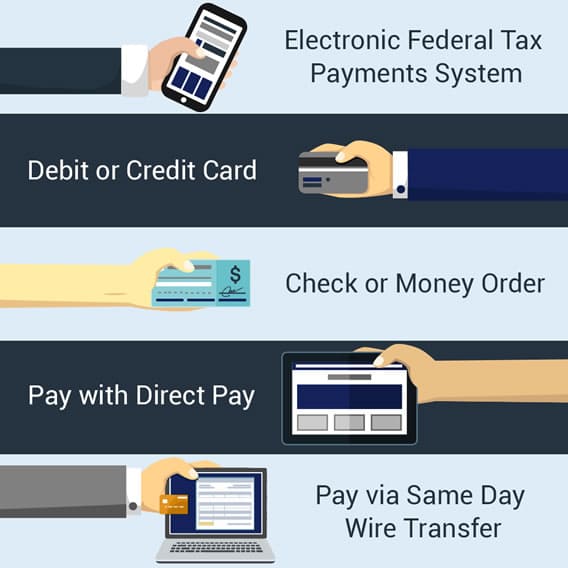

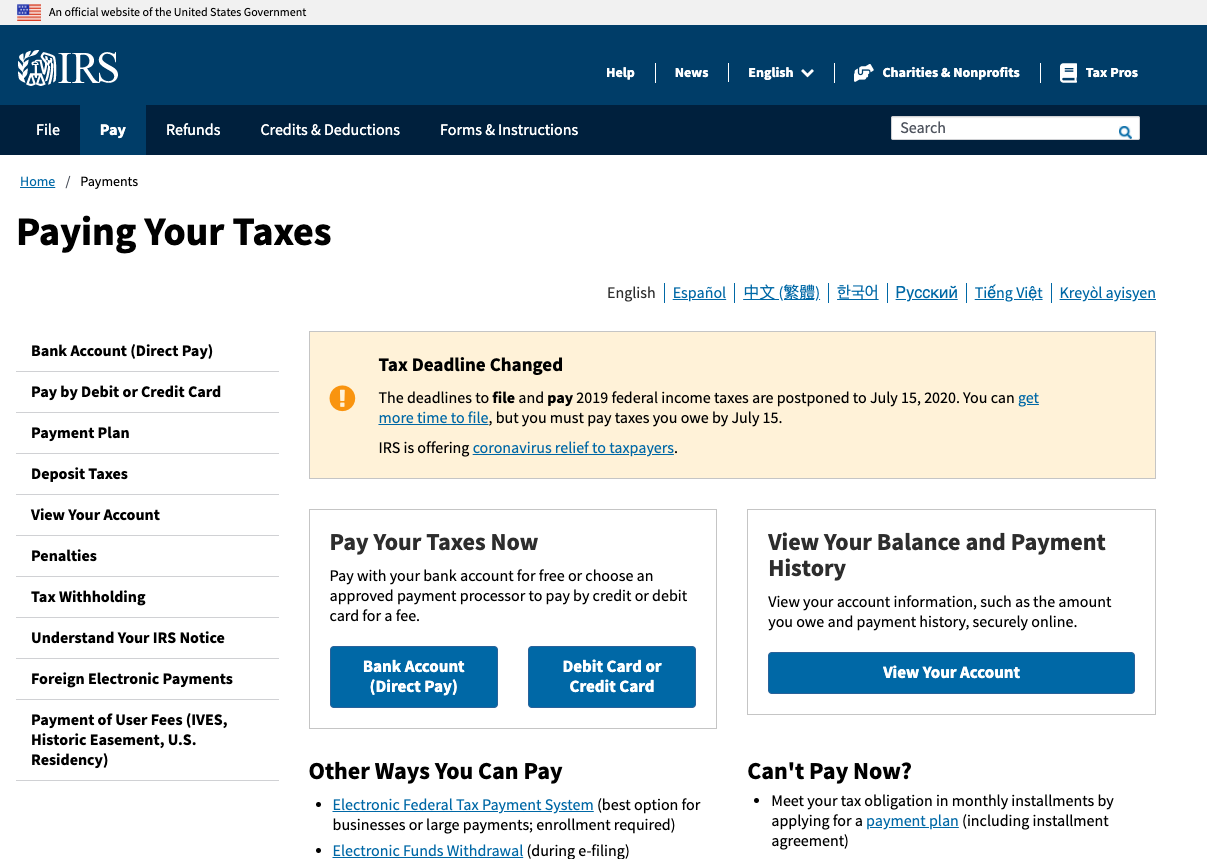

For individual taxpayers filing Form 1040, “Direct Pay” is often the most efficient route. This service allows you to pay your income tax directly from a checking or savings account without any additional fees. The interface is straightforward: you provide your tax year, your filing status, and your bank routing and account numbers.

The primary advantage of Direct Pay is the “instant” nature of the transaction. Once the payment is submitted, you receive a confirmation number that serves as an official receipt. This is particularly useful for those making estimated tax payments throughout the year—a common requirement for freelancers and small business owners who must manage their own withholding.

EFTPS: The Electronic Federal Tax Payment System

While Direct Pay is tailored for individuals, the Electronic Federal Tax Payment System (EFTPS) is the heavy-duty engine used by businesses and high-net-worth individuals. EFTPS requires a separate registration process, which includes receiving a PIN via mail for security purposes.

The power of EFTPS lies in its scheduling capabilities. Users can schedule payments up to 365 days in advance, making it an invaluable tool for corporate financial planning. For a business, missing a payroll tax deposit can result in significant penalties; using EFTPS ensures that these obligations are automated and tracked with professional precision.

Credit and Debit Card Payments

For those looking to leverage financial products, the IRS allows payments via third-party processors using credit or debit cards. While the IRS itself does not charge a fee for this service, the processors do. These fees usually range from 1.87% to 1.98% for credit cards, or a flat fee for debit cards.

From a strategic financial perspective, paying the IRS with a credit card can be a double-edged sword. It may allow a taxpayer to earn travel rewards or cash back, potentially offsetting the processing fee. However, if the balance is not paid off immediately, the high interest rates of credit cards can quickly eclipse any benefits. This method is best reserved for those who have the cash on hand but wish to maximize their loyalty program points.

Strategic Management of Tax Debt: Installment Agreements

Not every taxpayer has the liquidity to settle their entire balance by the April deadline. In the realm of personal finance, managing a tax gap requires a structured approach to avoid the draconian measures of levies or liens. The IRS offers several “payment plans” that act as a form of structured financing for your tax debt.

Short-Term and Long-Term Payment Plans

If you owe less than $100,000 in combined tax, penalties, and interest, you may qualify for a short-term payment plan, which gives you up to 180 days to pay the balance in full. This is often the best route for someone expecting a liquidity event, such as a bonus or the sale of an asset, in the near future.

For larger debts or longer timelines, the IRS offers Long-Term Installment Agreements (Direct Debit). These plans involve monthly payments over a period of up to 72 months. While interest and late-payment penalties still accrue, being on an approved plan stops the IRS from pursuing more aggressive collection actions. From a budgeting standpoint, an installment agreement transforms an overwhelming debt into a manageable monthly line item, allowing for more predictable financial forecasting.

The Offer in Compromise (OIC)

The “Offer in Compromise” is perhaps the most discussed yet least understood tool in tax management. It allows a taxpayer to settle their tax debt for less than the full amount they owe. However, the IRS only grants this if the taxpayer can prove that paying the full amount would create a “severe economic hardship” or if there is legitimate doubt as to the liability or collectability.

Applying for an OIC is a rigorous financial audit. The IRS examines your income, expenses, asset equity, and future earning potential. While it is a powerful tool for those in dire financial straits, it is not a “loophole” for the average taxpayer. It requires full transparency and a professional level of documentation.

Alternative Remittance: Cash, Checks, and Wire Transfers

Despite the digital shift, the IRS maintains several traditional and alternative payment channels to ensure accessibility for all segments of the economy. Whether you are unbanked or simply prefer traditional paper trails, these options remain viable components of the American tax system.

Retail Cash Payments

For individuals who prefer to deal in cash, the IRS has partnered with retail chains like 7-Eleven, CVS, and Walgreens through services like PayNearMe and VanillaDirect. Taxpayers can initiate a payment online, receive a code, and then take that code to a participating retail location to pay with cash.

There are limits to this method—usually around $1,000 per day—and it requires several days of lead time to process. From a financial inclusion perspective, this is a critical bridge for the unbanked population to remain compliant with federal law without needing a traditional line of credit or checking account.

The Traditional Paper Check or Money Order

Sending a check through the mail remains a popular option, though it is the most prone to error. When paying by check, the financial strategy is one of “verification.” You must ensure the check is made out to the “U.S. Treasury” (never the “IRS”), and includes your Name, Address, Social Security Number, Tax Year, and Tax Form on the memo line.

The risk with paper checks is the “lost in the mail” scenario. Professionals often recommend sending tax payments via Certified Mail with a Return Receipt Requested. This provides a legal paper trail that proves the payment was sent on time, which is vital if the IRS assesses a late-payment penalty due to a postal delay.

Same-Day Wire Transfers

For high-stakes situations where a payment must be received immediately to meet a legal deadline or stop a collection action, a same-day wire transfer is the ultimate tool. This involves a bank-to-bank transfer using the Federal Tax Collection Service (FTCS). While banks often charge a fee for outgoing wires (ranging from $25 to $50), the speed and finality of a wire transfer are unmatched for urgent financial compliance.

Security and Verification: Protecting Your Financial Identity

In the digital age, knowing how to pay the IRS also involves knowing how not to pay. Tax-related identity theft and payment scams are multi-billion-dollar industries. Protecting your financial health requires a vigilant approach to payment security.

Utilizing the IRS Online Account

The most secure way to manage your payments is through the official IRS Online Account portal. This dashboard provides a comprehensive view of your tax history, including amounts owed, payment history, and key records from your most recent tax return. By centralizing your interactions here, you reduce the risk of falling for phishing attempts.

A key rule of financial safety: The IRS will never initiate contact via text message or social media to request payment. Any communication demanding immediate payment via a gift card, prepaid debit card, or wire transfer without giving you the opportunity to question or appeal the amount is a hallmark of a scam.

Record Keeping and Post-Payment Auditing

Once a payment is made, the financial process is not over. Professional financial management requires robust record-keeping. You should maintain a digital or physical “Tax File” containing confirmation numbers, copies of checks, and bank statements showing the cleared funds.

The IRS typically has a three-year window to audit a return, but they can collect unpaid taxes for up to ten years. Keeping your payment receipts for this duration is not just a suggestion; it is a foundational practice for long-term financial security. If a discrepancy arises years later, your ability to produce a confirmation number from a 2024 Direct Pay transaction could save you thousands in potential reassessments and penalties.

Conclusion: Integration into Personal Finance

Paying the IRS should not be viewed as an isolated event, but as a recurring component of an integrated financial strategy. By mastering the tools of electronic remittance, understanding the structure of installment agreements, and maintaining rigorous security standards, you transform tax compliance from a source of stress into a routine administrative task. Whether you are an individual contributor, a freelancer, or a business owner, the ability to navigate the IRS payment systems with confidence is a hallmark of true financial literacy. In the end, proactive management of your tax liabilities ensures that more of your capital remains available for what truly matters: building wealth and securing your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.