American Express occupies a unique position in the financial landscape. For many, carrying a “Centurion” or “Platinum” card is a mark of financial achievement and a gateway to premium travel perks. However, personal finance is not static. What served your lifestyle five years ago might now represent an unnecessary drain on your capital through high annual fees.

Deciding to cancel an American Express card is rarely as simple as making a phone call and cutting the plastic (or metal) in half. Because of the way Amex structures its rewards ecosystem and credit reporting, a hasty cancellation can result in the loss of thousands of dollars in rewards points or a sudden dip in your credit score. This guide provides a professional, strategic approach to closing your account while protecting your financial health.

1. The Pre-Cancellation Checklist: Protecting Your Assets

Before you initiate the cancellation process, you must treat your credit card account as a financial portfolio. You wouldn’t close a bank account without moving the cash; similarly, you should not close a premium credit line without securing your “currency”—your Membership Rewards (MR) points and your credit standing.

Managing Your Membership Rewards Points

The most critical step in canceling an American Express card is determining the fate of your points. If you have an Amex card that earns Membership Rewards, such as the Gold or Platinum card, those points are tied to your overall account profile. If you close your only MR-earning card, your entire balance of points could vanish instantly.

To protect your points, you have three primary options:

- Keep another MR card open: If you have more than one Amex card (e.g., a Blue Business Plus and a Platinum), your points are safe as long as at least one card remains active.

- Transfer points to partners: If this is your only card, transfer your balance to airline or hotel partners like Delta, British Airways, or Marriott Bonvoy before closing the account.

- Open a no-annual-fee “Lifeboat” card: Consider applying for the Amex EveryDay® Credit Card. It has no annual fee but earns Membership Rewards, allowing you to park your points there indefinitely for free.

Evaluating the Impact on Your FICO Score

In the world of personal finance, your “Credit Utilization Ratio” and “Length of Credit History” are paramount. Closing a card reduces your total available credit. If you carry balances on other cards, your utilization percentage will spike, which can lower your credit score.

Furthermore, while the “age” of the account will remain on your credit report for ten years (for accounts closed in good standing), the loss of the active credit line can affect the internal algorithms used by lenders. If this is your oldest credit card, think twice. The longevity of your relationship with a lender is a significant factor in your creditworthiness.

Clearing Outstanding Balances and Pending Charges

Ensure your balance is $0 before calling. While you can technically cancel a card with a balance, you will still be responsible for payments, and interest will continue to accrue. Additionally, audit your “pending” transactions. If a merchant hasn’t finalized a charge, the cancellation might be delayed or lead to a “zombie” balance that triggers late fees because you assumed the account was closed.

2. The Step-by-Step Guide to the Cancellation Process

American Express is known for its high-touch customer service. When you attempt to cancel, you will be routed to a “Retention Specialist” whose job is to keep you as a customer. Knowing this allows you to navigate the conversation efficiently.

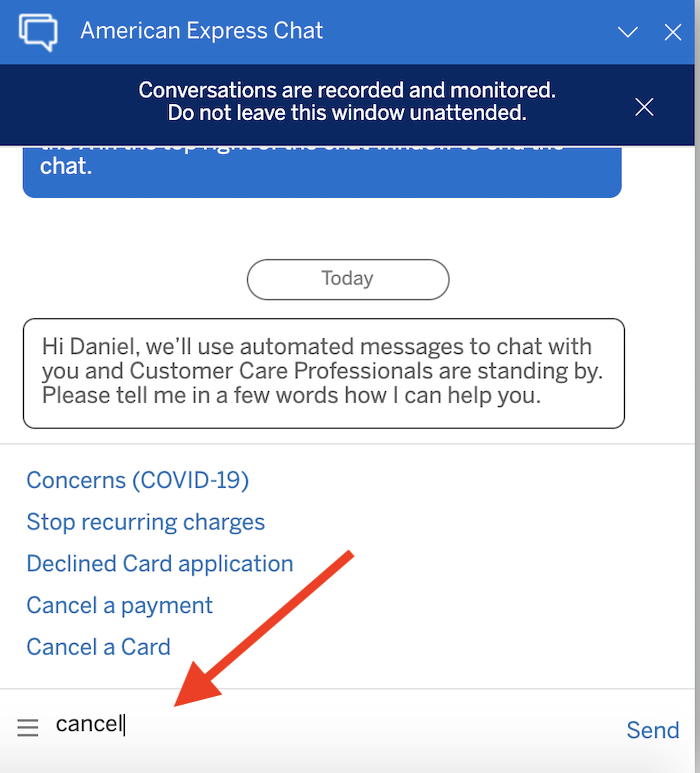

Method 1: Canceling via the Digital Chat Feature

One of the most efficient ways to cancel is through the American Express online portal or mobile app. The “Live Chat” feature connects you with a representative in real-time.

- Log in to your account.

- Navigate to the “Help” or “Contact Us” section and initiate a chat.

- State clearly: “I would like to close my account ending in [XXXX].”

- The representative will likely ask why. A simple “The annual fee no longer fits my budget” is usually sufficient.

- Important: Ask for a “Reference Number” for the cancellation request and save a transcript of the chat.

Method 2: Calling the Retention Line

If you prefer a verbal confirmation, call the number on the back of your card. You will eventually be transferred to the retention department. This is a more personal interaction where you may be asked detailed questions about your spending habits. If your mind is made up, remain firm but polite. Professionals recommend the “Broken Record” technique: regardless of the perks they offer, simply repeat, “I appreciate the offer, but I would like to close the account today.”

Confirming the Final Statement

Once the card is closed, you will lose access to the digital portal for that specific card eventually. Download your last 12 months of statements immediately. These are vital for tax purposes or in case of a future billing dispute. Your final statement should show a $0 balance and a “Closed at Customer Request” notation.

3. Strategic Alternatives: Retention Offers and Product Changes

Cancellation is a permanent solution to what might be a temporary financial misalignment. Before you sever the tie completely, consider if a different financial instrument within the Amex ecosystem would serve you better.

Requesting a Retention Offer

Before saying “close my account,” ask the representative: “Are there any retention offers available on my account that might justify me keeping the card for another year?”

Amex frequently offers “Statement Credits” or “Bonus Points” to high-value customers. For example, they might offer you 30,000 points if you spend $3,000 in the next three months. If the value of those points exceeds the annual fee, it is financially savvy to keep the card for one more year and re-evaluate later.

The “Downgrade” Strategy (Product Change)

If the annual fee is the primary pain point, ask about a “Product Change.” This allows you to swap your high-fee card for a lower-fee or no-fee version within the same “family” of cards.

- The Gold Card Family: You can often downgrade a Gold card to a Green card.

- The Cash Back Family: You can downgrade a Blue Cash Preferred to a Blue Cash Everyday.

The benefit of a downgrade is that your credit line remains open, your account age continues to grow, and you avoid a “hard pull” on your credit report that usually accompanies a new application.

The 30-Day Rule for Annual Fees

Timing is everything in business finance. If your annual fee has recently posted, American Express generally provides a 30-day window from the statement closing date to cancel the card and receive a full refund of that fee. If you miss this window, they may pro-rate the refund in some jurisdictions, but in many cases, the fee is non-refundable after 30 days. Always check your statement date before initiating the call.

4. Post-Cancellation Best Practices: Ensuring a Clean Break

The work isn’t finished just because the representative said the account is closed. You must perform a final audit to ensure your financial footprint is secure.

Redirecting Automated Payments

In our subscription-based economy, it is easy to forget which services are linked to which card. From Netflix and Amazon Prime to your gym membership and insurance premiums, audit your last three statements. Update these vendors with a new payment method immediately. A “failed payment” on a recurring bill can lead to service interruptions or, worse, a report to a collections agency if ignored.

Monitoring Your Credit Report

Thirty to sixty days after cancellation, check your credit report via a service like AnnualCreditReport.com or a banking app. Verify that the account status is listed as “Closed by Consumer.” If it says “Closed by Grantor,” it could imply the bank closed it due to poor management, which looks worse to future lenders. If there is an error, dispute it immediately with the credit bureaus.

Safe Disposal of Physical Assets

Modern American Express cards, particularly the Platinum and Gold versions, are made of stainless steel or metal alloys. These cannot be destroyed with standard household scissors.

- Request a Mailer: You can ask Amex to send you a prepaid envelope to return the metal card for secure recycling.

- Use Heavy-Duty Tools: If you choose to do it yourself, use tin snips.

- Protect Your Data: Ensure the EMV chip and the magnetic stripe are destroyed. Even though the account is closed, the physical card contains sensitive data that should not fall into the wrong hands.

Conclusion

Canceling an American Express card is a significant financial decision that should be executed with precision. By auditing your Membership Rewards, considering the impact on your credit score, and exploring retention or downgrade options, you ensure that your exit from the Amex ecosystem is as profitable as your entry was.

In the landscape of personal finance, your tools should always serve your goals. If a card’s costs outweigh its utility, closing it is not a failure—it is a strategic recalibration of your financial portfolio. Follow these steps to ensure that when you close that door, your credit reputation and your accumulated wealth remain firmly intact.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.