Social Security is often viewed as the bedrock of the American retirement system, providing a predictable stream of income for millions of workers. However, for a specific segment of the population—including teachers, police officers, firefighters, and long-term federal employees—the math behind those monthly checks can be surprisingly complex. If you have spent a portion of your career in a job where you did not pay Social Security taxes but earned a pension, you are likely to encounter the Windfall Elimination Provision (WEP).

The Windfall Elimination Provision is a federal law that can significantly reduce the Social Security benefits of workers who receive a “non-covered” pension. Understanding the WEP is not just a matter of academic interest; it is a vital component of financial literacy for anyone planning their post-career lifestyle. Failure to account for this provision can lead to a shortfall in your retirement budget, potentially costing you hundreds of dollars every month.

Understanding the Mechanics of the Windfall Elimination Provision (WEP)

To understand why the WEP exists, one must first understand how the Social Security Administration (SSA) calculates benefits. Social Security is designed to be a progressive system. This means it is intended to replace a higher percentage of pre-retirement earnings for lower-wage workers than for higher-wage workers.

The Origins and Purpose of WEP

The WEP was enacted in 1983 as part of a larger overhaul to ensure the long-term solvency of the Social Security Trust Funds. Before the WEP, workers who spent the majority of their careers in “non-covered” employment (jobs where they paid into a separate pension system instead of Social Security) were treated the same as lifelong low-wage workers by the SSA formula.

Because these workers only had a few years of Social Security earnings or had very low “covered” earnings, the SSA formula viewed them as “needy” and applied the most generous replacement rates to their benefits. In reality, these individuals often had substantial pensions from their primary careers. The WEP was introduced to eliminate this “windfall”—essentially a double-dipping effect where a worker receives both a full pension and a Social Security benefit calculated as if they were a low-income earner.

How Social Security Calculates Your Benefits

Standard Social Security benefits are calculated based on your Average Indexed Monthly Earnings (AIME). The SSA applies a formula to your AIME to determine your Primary Insurance Amount (PIA). This formula uses “bend points.” For most workers, the first bend point replaces 90% of their average monthly earnings up to a certain dollar amount.

When the WEP is applied, that 90% multiplier is reduced—often down to 40%. This adjustment effectively lowers the “base” of your Social Security benefit, reflecting the fact that you are already receiving a pension from employment that was not subject to Social Security payroll taxes.

Who Is Impacted by the Windfall Elimination Provision?

The WEP does not apply to everyone. It specifically targets individuals who receive a pension from work where they did not pay Social Security taxes and who also qualify for Social Security benefits through other employment (either from a second job or a different phase of their career).

Public Sector Workers and Educators

The most common group affected by the WEP consists of state and local government employees. In several states—including California, Texas, Ohio, and Massachusetts—many public-sector employees, particularly teachers, do not participate in the Social Security system. Instead, they contribute to state-run retirement systems. If a teacher in one of these states worked a summer job for 20 years or had a private-sector career before entering the classroom, they may qualify for Social Security, but their benefit will be subject to the WEP reduction because of their teacher’s pension.

Federal Employees and the CSRS System

Federal employees hired before January 1, 1984, were typically enrolled in the Civil Service Retirement System (CSRS). Like the state systems mentioned above, CSRS employees did not pay Social Security taxes. While most newer federal employees are under the Federal Employees Retirement System (FERS), which does include Social Security, thousands of long-tenured civil servants still fall under the CSRS and are therefore subject to the WEP if they have earned enough Social Security credits elsewhere.

Individuals with International Pensions

In our globalized economy, many professionals spend portions of their careers working abroad. If you worked in a foreign country and earned a pension from a system that is not integrated with U.S. Social Security through a “Totalization Agreement,” the WEP may apply. The SSA views these foreign pensions similarly to non-covered domestic pensions, as the earnings were not subject to U.S. Social Security taxes.

How the WEP Calculation Changes Your Social Security Check

The most pressing question for those affected is: “How much will my benefit be reduced?” The reduction is not a flat percentage of your total benefit, but rather an adjustment to the formula used to calculate it.

The “Bend Point” Formula Explained

As of 2024, the standard Social Security formula takes 90% of the first $1,174 of your average indexed monthly earnings, adds 32% of earnings between $1,174 and $7,078, and adds 15% of earnings above that.

If you are subject to the full WEP reduction, that initial 90% factor is slashed to 40%. This results in a maximum monthly reduction that is capped each year. For 2024, the maximum WEP reduction is $587 per month. It is important to note that the WEP reduction cannot exceed one-half of the amount of your monthly non-covered pension. This “guarantee” protects those with very small pensions from having their Social Security benefit completely wiped out.

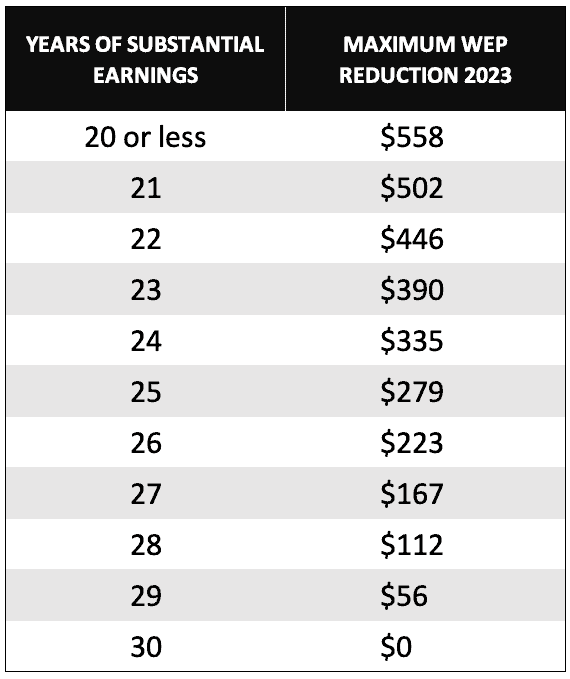

The Maximum Reduction Limit

While the $587 figure sounds daunting, it represents the worst-case scenario. The law includes a sliding scale based on “substantial earnings.” If you have 20 or fewer years of substantial earnings in the Social Security system, the 40% factor applies. However, if you have between 21 and 30 years of substantial earnings, the percentage gradually increases. For example, with 25 years of substantial earnings, the multiplier is 65%. Once you reach 30 years of substantial earnings, the WEP is eliminated entirely, and you receive your full Social Security benefit.

Strategies and Exemptions to Mitigate the Impact of WEP

For many workers, the discovery of the WEP comes as a shock late in their careers. However, there are strategic ways to navigate these rules and maximize your total retirement income.

The 30-Year Rule for Substantial Earnings

The most effective way to bypass the WEP is to ensure you have 30 years of “substantial earnings” under Social Security. The SSA defines “substantial earnings” differently each year (for 2024, the threshold is $31,275). If you are close to the 30-year mark—perhaps you have 27 or 28 years—it may be financially beneficial to work a few extra years in a Social Security-covered job. By reaching that 30-year threshold, you move back to the 90% multiplier, potentially adding thousands of dollars to your annual retirement income.

Coordinating with Spouse Benefits and GPO

It is also vital to distinguish between the WEP and the Government Pension Offset (GPO). While the WEP affects your own retirement or disability benefits, the GPO affects the Social Security benefits you might receive as a spouse or surviving spouse. If you are a government retiree, the GPO can reduce your spousal or survivor benefit by two-thirds of the amount of your government pension.

When planning with a spouse, it is crucial to run the numbers for both provisions. In some cases, it may make sense for the higher-earning spouse to delay Social Security to maximize the survivor benefit, even if the WEP or GPO will eventually apply.

Planning Your Retirement Strategy in the Shadow of WEP

Navigating the intersection of a non-covered pension and Social Security requires proactive financial planning. You cannot rely on the standard “Social Security Statement” you receive in the mail, as those estimates usually do not account for the WEP reduction until you actually apply for benefits.

Using the Social Security Online Tools

The Social Security Administration provides a “WEP Calculator” on its official website. To get an accurate picture of your future income, you should input your actual earnings history and the expected amount of your non-covered pension. This will provide a much more realistic estimate than the generic statements. Financial advisors specializing in public sector retirement are also invaluable resources, as they can help integrate your pension, Social Security, and personal savings (like a 403(b) or 457 plan) into a cohesive strategy.

Diversifying Retirement Income Streams

Because the WEP can take a “bite” out of your expected Social Security, diversification is key. Relying solely on a pension and Social Security may leave you vulnerable. Maximizing contributions to tax-advantaged accounts like IRAs or Roth IRAs can provide a buffer. Additionally, understanding that your Social Security check will be smaller should influence your decisions regarding when to claim benefits. While the WEP reduces the base amount, the standard rules for early or delayed retirement still apply. Delaying your claim from age 67 to 70 will still result in an 8% annual increase, though that increase will be applied to the WEP-reduced amount.

In conclusion, the Windfall Elimination Provision is a complex but essential factor in retirement planning for millions of dedicated public servants and international workers. While the reduction in benefits can be significant, it is not an insurmountable obstacle. By understanding the “substantial earnings” rules, utilizing accurate calculation tools, and diversifying your income streams, you can build a secure and prosperous retirement, ensuring that the WEP is merely a calculated variable in your financial success rather than a surprise setback.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.