Understanding the concept of a “starting credit score” is crucial for anyone venturing into the world of personal finance, especially for young adults or individuals who are new to credit. It’s the foundational score upon which future financial health is built. This score acts as a financial report card, influencing your ability to access loans, rent an apartment, secure a job, and even obtain insurance. While there isn’t a single, universal “starting” number that everyone receives, the journey to establishing credit and achieving a score begins with specific actions and timelines. This article will delve into what constitutes a starting credit score, how it’s formed, and the key factors that influence its initial development.

The Genesis of Your Credit Score: When Does it Begin?

For many, the concept of a credit score only becomes relevant when they need to borrow money or engage in financial transactions that require a credit check. However, the process of building a credit history, and consequently a credit score, can begin earlier than many realize. It’s not an abstract entity that magically appears; it’s a reflection of your financial behaviors over time.

The Age of Creditworthiness: When Can You Get a Credit Score?

Legally, individuals can begin to establish credit and thus have a credit score as soon as they are 18 years old. This is the age when you can legally enter into contracts, including those for credit cards, loans, and other financial products. Before the age of 18, it’s generally not possible to have a credit score because you lack the legal capacity to incur debt.

However, simply being 18 doesn’t automatically grant you a credit score. A credit score is derived from your credit history, which is a record of how you’ve managed borrowed money. If you haven’t taken out any loans or opened any credit accounts, you won’t have a credit history, and therefore, no credit score. This situation is often referred to as having a “thin file” or “no credit history.”

The “No Credit” Scenario: What is a Starting Point?

When individuals first become eligible to have a credit score, they often find themselves in a “no credit” situation. This means there is no data in their credit report for the credit bureaus to analyze. In such cases, the “starting credit score” isn’t a specific number, but rather the absence of one. Credit scoring models require a certain amount of information to generate a score. For example, the FICO score, one of the most widely used credit scoring systems, typically needs at least one account that has been open for six months or more and has been reported to the credit bureaus.

For individuals with no credit history, the initial score might be nonexistent or so low as to be functionally unscoreable. This can present a challenge when trying to access credit for the first time. Lenders are hesitant to extend credit to someone with no track record of responsible borrowing. This is why taking proactive steps to build credit is essential.

Building Your First Credit Score: The Foundational Steps

Establishing a credit score from scratch requires a deliberate and strategic approach. The goal is to create a positive credit history that demonstrates your ability to manage debt responsibly. This involves opening specific types of accounts and using them wisely.

The First Lines of Credit: Options for Newcomers

There are several pathways for individuals to begin building their credit history. Each has its own nuances and potential benefits.

Secured Credit Cards: A Low-Risk Entry Point

Secured credit cards are an excellent option for individuals with no credit history. These cards require a cash deposit upfront, which typically becomes the credit limit on the card. For instance, a $300 deposit might grant you a $300 credit limit. The deposit acts as collateral for the lender, significantly reducing their risk.

When you use a secured credit card, your payment activity is reported to the major credit bureaus (Equifax, Experian, and TransUnion). By making on-time payments and keeping your credit utilization low on the secured card, you begin to build a positive credit history. After a period of responsible use, many issuers will allow you to graduate to an unsecured credit card and may even refund your deposit.

Credit-Builder Loans: A Structured Approach

Credit-builder loans are specifically designed to help individuals establish or improve their credit. These loans are often offered by credit unions and community banks. The unique aspect of a credit-builder loan is that the borrowed amount is held in an account by the lender and released to you only after you have fully repaid the loan.

While you’re repaying the loan, your on-time payments are reported to the credit bureaus, effectively building your credit history. Once the loan is fully repaid, you receive the principal amount. This method provides a structured way to demonstrate your ability to make consistent payments.

Authorized User on an Existing Account: Leveraging Someone Else’s Credit

Becoming an authorized user on a credit card account belonging to someone with a strong credit history can also help you establish your own credit. The primary account holder adds you to their card, and you receive a card with your name on it. The activity on this card, including payment history and credit utilization, is then reported to your credit report.

However, this method comes with a significant caveat: the primary account holder’s financial behavior directly impacts your credit. If they make late payments or carry high balances, it can negatively affect your credit. It’s crucial to trust the primary account holder and ensure they manage their account responsibly.

Becoming an Authorized User Strategically

To leverage this option effectively, ensure the primary account holder has a long history of on-time payments, low credit utilization, and an account that has been open for a substantial period. This will provide the most beneficial data to your credit report. It’s also wise to have a clear understanding with the primary account holder about how the card will be used and who is responsible for payments.

The Crucial Factors Influencing Your Initial Credit Score

Once you begin to establish credit, your score will gradually develop. Several key factors play a significant role in shaping this initial score. Understanding these elements allows you to make informed decisions that foster positive credit growth.

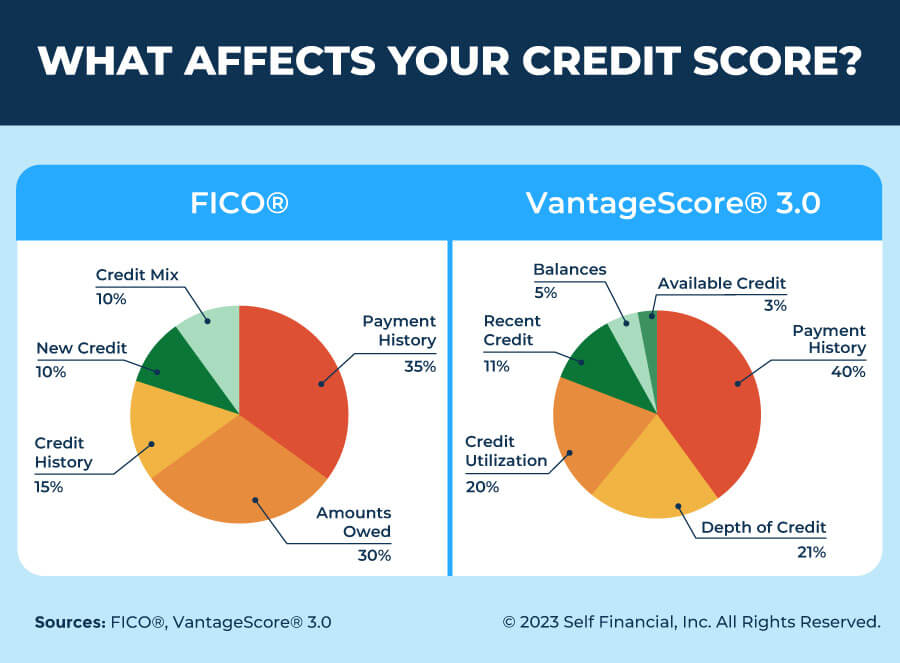

Payment History: The Most Important Pillar

Your payment history is the single most influential factor in determining your credit score, accounting for approximately 35% of a FICO score. This refers to whether you pay your bills on time. Even a single late payment, especially if it’s more than 30 days past due, can significantly damage your nascent credit score.

For individuals just starting out, demonstrating consistent on-time payments is paramount. This means paying your credit card bills, loan installments, and any other credit obligations by their due dates. Automating payments or setting up reminders can be invaluable tools in ensuring you never miss a payment.

The Impact of Delinquencies

Any instance of delinquency, whether it’s 30, 60, or 90 days late, will be reflected on your credit report and will negatively impact your score. The longer a payment is overdue, the more severe the damage. Establishing a habit of timely payments from the outset is the most effective way to build a strong foundation.

Credit Utilization: Keeping Balances Low

Credit utilization refers to the amount of credit you are using compared to your total available credit. This factor typically accounts for about 30% of your FICO score. It’s generally recommended to keep your credit utilization ratio below 30%, and ideally below 10%, for optimal credit health.

For someone with a limited credit history, a secured credit card with a low credit limit might mean that even small purchases can lead to a high utilization ratio. For example, if your secured card has a $300 limit and you spend $150 on it, your utilization is 50%. This can negatively impact your score, even if you make payments on time.

Strategies for Managing Utilization

To manage credit utilization effectively when starting out:

- Pay down balances frequently: Don’t wait until the end of the billing cycle to pay off your balance. Pay down your balance as you make purchases to keep the reported utilization low.

- Avoid maxing out cards: Even if you have the ability to spend up to your limit, resist the urge to do so.

- Request credit limit increases (strategically): Once you’ve demonstrated responsible usage, you might be eligible for a credit limit increase on your secured card. This can improve your utilization ratio without increasing your spending.

Length of Credit History: The Power of Time

The length of your credit history accounts for about 15% of your FICO score. This factor measures how long your credit accounts have been open and how long it’s been since you last used them. A longer credit history generally contributes to a higher score because it provides lenders with more data to assess your creditworthiness over time.

For individuals new to credit, this factor will initially be low. The key here is patience. As you keep your accounts open and in good standing, this factor will naturally improve. Avoid closing your oldest accounts, even if you have newer ones, as this can shorten your average credit history length.

Credit Mix and New Credit: Less Significant, but Still Relevant

The remaining portions of your credit score are influenced by your credit mix and new credit.

Credit Mix (10%): Variety of Credit Types

This factor looks at the different types of credit you have (e.g., credit cards, installment loans like auto loans or mortgages). Having a mix of credit types can be beneficial, as it shows you can manage different forms of debt. However, for someone just starting out, this is less of a concern. Focusing on managing one or two credit accounts responsibly is far more important than trying to diversify too early.

New Credit (10%): Recent Activity

This factor considers how many new credit accounts you’ve opened recently and how many hard inquiries (when a lender checks your credit for a loan or credit card application) are on your report. Opening too many new accounts in a short period can signal to lenders that you might be taking on too much debt.

When you first start building credit, you’ll likely have a few hard inquiries as you apply for secured cards or credit-builder loans. This is normal. However, avoid applying for multiple new credit products simultaneously. Space out your applications to minimize the impact on your score.

The Evolution of Your Starting Score: From Zero to Hero

The journey from having no credit score to achieving a good or excellent one is a marathon, not a sprint. It requires consistent good financial habits and a bit of patience. Your initial “starting credit score” is essentially a blank slate, and the numbers that begin to appear are a direct result of your actions.

Initial Scores: What to Expect

When you first open a credit account, it takes time for the information to be reported to the credit bureaus. This reporting typically happens once a month. Therefore, don’t expect an immediate score. It can take a few months of activity before a credit scoring model can generate a score.

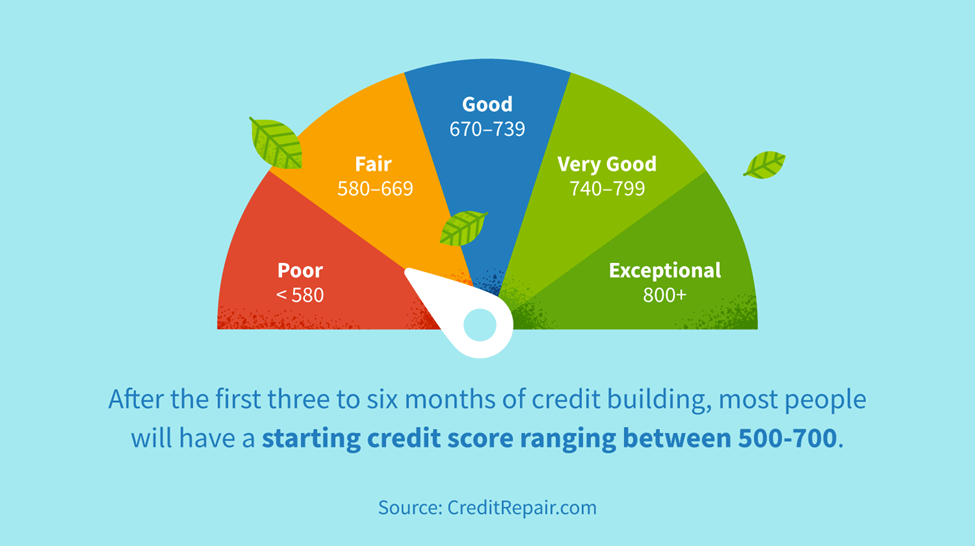

The very first scores you receive might be in the “fair” or “average” range. This is not necessarily a bad thing. It signifies that you have begun to establish a credit file. The goal then becomes to steadily improve this score.

Improving Your Score Over Time: Strategies for Growth

- Consistent On-Time Payments: As mentioned, this is the cornerstone of credit building.

- Maintain Low Credit Utilization: Keep your balances significantly lower than your credit limits.

- Avoid Opening Too Many Accounts at Once: Be strategic about when and how you apply for new credit.

- Monitor Your Credit Reports: Regularly check your credit reports for errors and to track your progress. You can obtain free copies of your credit reports annually from each of the three major credit bureaus at AnnualCreditReport.com.

- Patience: Credit scores don’t improve overnight. It takes time and consistent responsible behavior.

The “Starting Credit Score” as a Launchpad

Ultimately, the “starting credit score” isn’t a fixed point but rather the initial benchmark that reflects your early engagement with the credit system. Whether it’s a score derived from responsible use of a secured card, a credit-builder loan, or as an authorized user, it represents the first data points that lenders will use to assess your financial reliability. By understanding how this score is built and the factors that influence it, individuals can proactively cultivate a strong credit history, opening doors to a wider range of financial opportunities and a more secure financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.