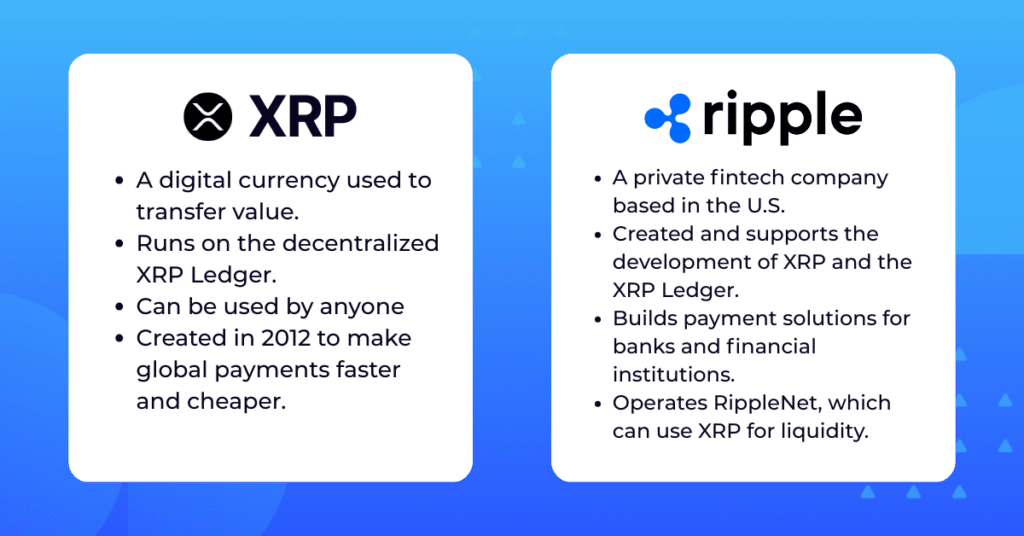

In the rapidly evolving landscape of digital assets, few cryptocurrencies have sparked as much debate, interest, and institutional scrutiny as XRP. Developed by Ripple Labs, XRP was designed from its inception to solve a specific, high-stakes problem: the inefficiency of the global financial system. While many cryptocurrencies were created to serve as alternative currencies or “digital gold,” XRP was built as a bridge.

Understanding what XRP is used for requires looking beyond the speculative nature of the crypto markets and focusing on its core utility as a financial tool. From revolutionizing cross-border payments to providing a foundation for central bank digital currencies (CBDCs), XRP serves as a linchpin in the transition from legacy banking to a real-time, internet-of-value economy. This article explores the primary use cases of XRP through the lens of personal finance, institutional investment, and global business operations.

Revolutionizing Cross-Border Payments and Liquidity

The primary and most significant use case for XRP is its role in cross-border settlements. In the traditional banking world, sending money across borders is a cumbersome, expensive, and time-consuming process. XRP was engineered to act as a “bridge currency,” allowing for the near-instantaneous transfer of value between different fiat currencies.

The Inefficiencies of the SWIFT Network

To understand why XRP is valuable, one must first understand the problem it solves. For decades, the global financial system has relied on the SWIFT (Society for Worldwide Interbank Financial Telecommunication) network. While SWIFT is reliable, it does not actually move money; it merely sends payment instructions. The actual settlement requires a complex web of intermediary banks and “Nostro/Vostro” accounts—pre-funded accounts held in foreign currencies. This system is slow (taking 3 to 5 days) and expensive, with high fees and significant capital tied up in dormant accounts.

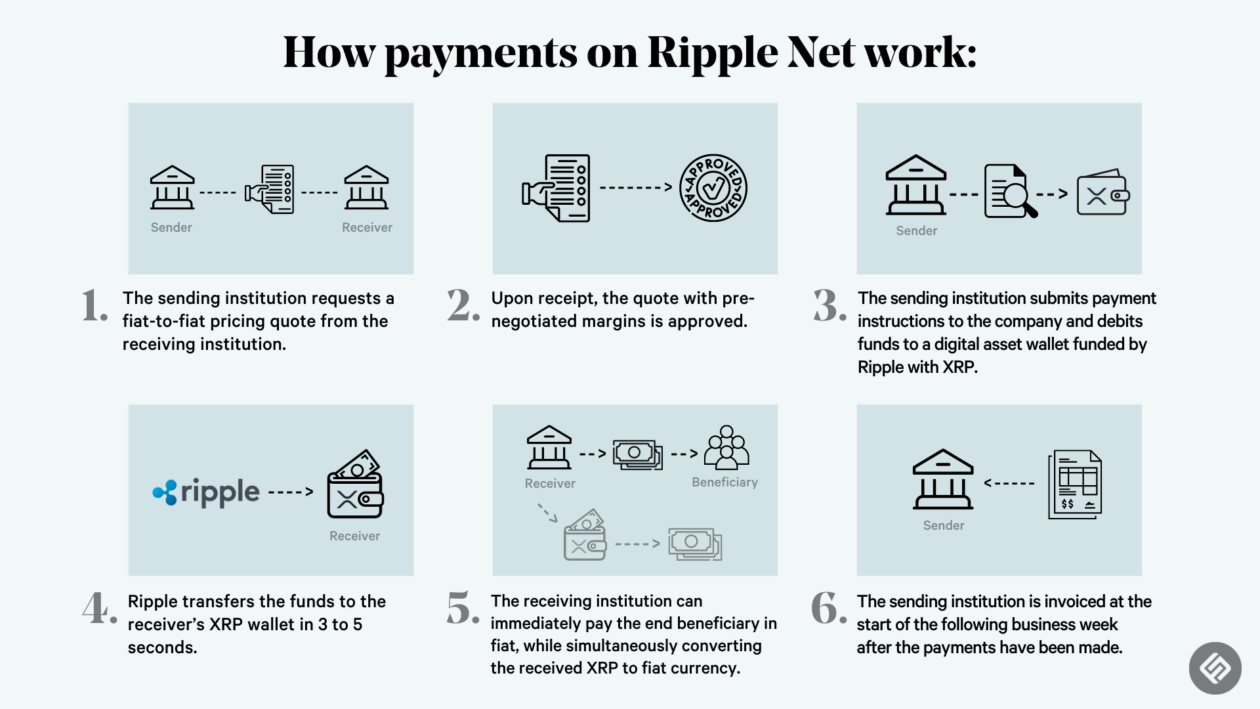

On-Demand Liquidity (ODL)

XRP’s most prominent application is within Ripple’s “On-Demand Liquidity” (ODL) service. Using XRP, financial institutions can settle transactions in real-time without the need to pre-fund accounts in destination markets.

In an ODL transaction, the sending bank converts its local fiat currency into XRP. That XRP is instantly sent across the XRP Ledger (XRPL) to the destination market, where it is converted back into the local fiat currency of the recipient. This entire process takes approximately three to five seconds. For businesses, this means freeing up trillions of dollars in stagnant capital that can be reinvested into growth, rather than sitting in foreign bank accounts.

Reducing Costs for Small and Medium Enterprises (SMEs)

While major banks are the primary target for ODL, the cost-saving benefits of XRP extend to Small and Medium Enterprises (SMEs). Traditional cross-border fees can be prohibitive for smaller companies trying to scale internationally. By utilizing XRP-powered payment corridors, SMEs can reduce transaction costs by up to 40-70%, allowing them to compete more effectively in a globalized marketplace.

XRP as an Institutional and Retail Investment Asset

Beyond its functional utility in payments, XRP is a major asset in the world of personal and institutional finance. As one of the top cryptocurrencies by market capitalization, it represents a significant portion of many diversified digital asset portfolios.

Liquidity and Market Accessibility

XRP is one of the most liquid digital assets in the world. It is traded on hundreds of exchanges globally, making it highly accessible to both retail investors and institutional hedge funds. This high liquidity is essential for its use as a bridge currency, but it also makes XRP a popular choice for traders looking for an asset with high volume and tight spreads. For the individual investor, XRP provides a gateway into the “fintech” sector of the crypto market, offering exposure to the growing adoption of blockchain technology by traditional financial institutions.

Portfolio Diversification and Risk Management

From a personal finance perspective, XRP is often viewed as a “utility play.” Unlike “meme coins” or purely speculative tokens, XRP’s value proposition is tied to its adoption by the banking sector. Investors often use XRP to diversify their portfolios, balancing the store-of-value characteristics of Bitcoin and the smart-contract utility of Ethereum with an asset focused on the global payments infrastructure. However, like all digital assets, XRP is subject to market volatility, and financial advisors typically recommend it as part of a high-risk/high-reward allocation within a broader investment strategy.

The Role of Regulatory Clarity

A major factor in XRP’s status as an investment asset has been its legal journey, particularly in the United States. The resolution of regulatory challenges has provided XRP with a level of legal clarity that few other digital assets possess. For institutional investors—such as pension funds or insurance companies—this clarity is a prerequisite for entry. As regulatory frameworks solidify, XRP is increasingly seen as a “compliant” asset, potentially opening the doors for its inclusion in Exchange Traded Products (ETPs) and institutional-grade financial instruments.

The Foundation for Central Bank Digital Currencies (CBDCs)

As nations around the world explore the digitization of their national currencies, the technology behind XRP has emerged as a leading contender for the infrastructure of Central Bank Digital Currencies (CBDCs).

Interoperability Between National Currencies

One of the greatest challenges in the shift to CBDCs is interoperability. If the United States develops a digital dollar and Brazil develops a digital real, they must be able to communicate and exchange value seamlessly. The XRP Ledger (XRPL) is designed to facilitate this interoperability. Because XRP can act as a neutral bridge asset, it allows different CBDCs to be exchanged without requiring a direct pair or a complex network of intermediary banks.

Financial Inclusion and Economic Efficiency

For many developing nations, CBDCs offer a way to increase financial inclusion by providing unbanked populations with access to digital financial services. The low transaction costs associated with XRP—fractions of a cent per transaction—make it an ideal backbone for microtransactions and government-to-citizen payments. By leveraging the XRPL, central banks can issue and manage digital versions of their currencies with greater transparency and lower administrative overhead than traditional physical currency systems.

Private Versions of the XRP Ledger

Ripple has also introduced a private version of the XRP Ledger specifically for central banks. This allows nations to maintain control over their monetary policy and privacy while benefiting from the speed and efficiency of the public XRPL technology. This dual-layer approach—where private ledgers can settle transactions using the public XRP asset as a bridge—positions XRP at the center of the future sovereign financial system.

Micropayments and the New Content Economy

The financial utility of XRP is not limited to large-scale banking. Its speed and low cost make it a premier tool for the burgeoning world of micropayments and the “creator economy.”

Monetizing Digital Content

Traditionally, it has been impossible to send a payment of $0.05 or $0.10 over the internet because the transaction fees (often $0.30 plus a percentage) would exceed the value of the payment. XRP solves this. Through platforms like Coil, creators can be paid in XRP in real-time as users consume their content. This allows for a “pay-as-you-go” model for journalism, music, and video, moving away from intrusive advertising and expensive monthly subscriptions.

Gaming and Virtual Economies

In the world of online gaming and the metaverse, XRP is used to facilitate the instant purchase and trade of virtual assets. Whether it is buying a “skin” in a game or a piece of virtual real estate, the ability to move small amounts of value instantly and cheaply is essential. XRP serves as a financial tool for developers who want to integrate frictionless economies into their software without the latency issues of older blockchain networks.

Peer-to-Peer (P2P) Remittances

For individuals sending money to family members in other countries, XRP provides a side-hustle and personal finance solution. Rather than paying 10% to 15% in fees to traditional remittance providers, users can utilize XRP-based wallets to send funds directly to their relatives. This ensures that more of the hard-earned money reaches its destination, directly impacting the financial well-being of families in remittance-dependent economies.

Conclusion: The Future of XRP in the Financial Sector

XRP is far more than a digital asset; it is a sophisticated financial tool designed to bridge the gap between the legacy banking world and the future of decentralized finance. Its primary use cases—cross-border liquidity, institutional investment, CBDC infrastructure, and micropayments—all point toward a single goal: making the movement of money as easy as the movement of information.

For the investor, XRP represents a stake in the modernization of the global financial plumbing. For the business owner, it offers a way to reclaim trapped capital and reduce operational costs. And for the global economy, it provides a scalable, sustainable, and efficient path toward a more inclusive financial future. As adoption continues to grow, the utility of XRP will likely expand, further cementing its role as a fundamental pillar of the digital age’s financial architecture.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.