In the landscape of personal finance, few tools are as powerful—yet frequently misunderstood—as the Individual Retirement Account, or IRA. While the term is often tossed around in conversations about retirement planning and tax season, many individuals view it as a complex bureaucratic hurdle rather than the wealth-building engine it truly is. At its core, an IRA is more than just a savings account; it is a tax-advantaged investment vehicle designed to help individuals secure their financial future independently of employer-sponsored plans.

Understanding the mechanics of an IRA is essential for anyone looking to achieve financial independence. Whether you are a young professional just starting your career, a freelancer navigating the gig economy, or a mid-career specialist looking to optimize your portfolio, the IRA offers a level of flexibility and control that is often missing from traditional corporate benefits. This guide explores the nuances of the IRA, the different types available, and how you can leverage them to maximize your long-term net worth.

Understanding the Fundamentals of an Individual Retirement Account (IRA)

To appreciate the value of an IRA, one must first understand its structural purpose. Unlike a standard savings account at a bank, where your money sits and earns a nominal interest rate (often failing to keep pace with inflation), an IRA is a “wrapper” that holds various investments. Inside an IRA, you can hold stocks, bonds, mutual funds, exchange-traded funds (ETFs), and even real estate in certain specialized accounts.

How an IRA Differs from a 401(k)

The most common point of confusion is the difference between an IRA and a 401(k). The primary distinction lies in “ownership” and “sponsorship.” A 401(k) is a retirement plan offered by an employer. The employer chooses the provider and the investment menu, and they may offer a “match” on your contributions.

An IRA, conversely, is “Individual.” You open it yourself through a brokerage, a bank, or an investment platform. This gives you total control over the investment selection. While you don’t get an employer match in an IRA, you gain access to a much wider array of investment options and lower fee structures, which can significantly impact your portfolio’s growth over several decades.

The Power of Compound Interest and Tax Deferral

The true magic of an IRA lies in its tax treatment. In a standard brokerage account, you pay taxes on dividends and realized capital gains every year. This “tax drag” slows down the growth of your money. Within an IRA, your investments grow either tax-deferred or tax-free.

Consider the “snowball effect” of compound interest. When your earnings are not being chipped away by the IRS every year, the full amount of your profit is reinvested to earn even more profit the following year. Over a 30-year horizon, the difference between a taxable account and a tax-advantaged IRA can amount to hundreds of thousands of dollars in additional wealth, even if the underlying investments are identical.

Exploring the Core Types of IRAs

Not all IRAs are created equal. The IRS provides different “flavors” of these accounts to suit different income levels and tax strategies. Choosing the right one depends largely on your current tax bracket versus the tax bracket you expect to be in when you retire.

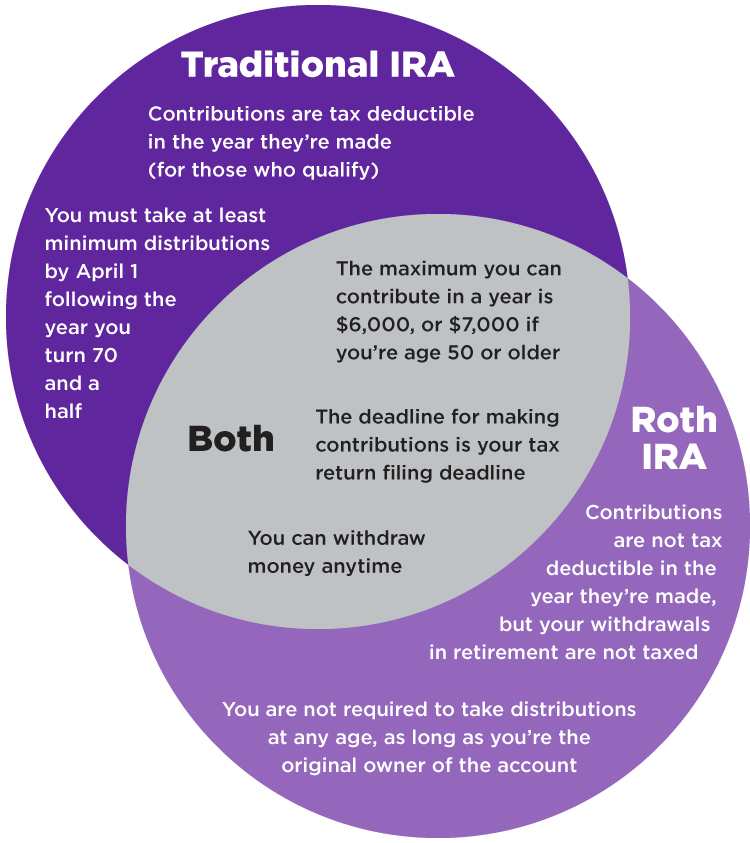

Traditional IRA: Tax-Deductible Contributions

The Traditional IRA is the original version of this account. Its primary appeal is the immediate tax break. Contributions to a Traditional IRA are often tax-deductible in the year you make them. For example, if you earn $70,000 a year and contribute $7,000 to a Traditional IRA, the IRS treats your taxable income as $63,000.

However, there is a trade-off. While you get a break today, you must pay income tax on the money when you withdraw it in retirement. This is an ideal strategy for those who are currently in a high tax bracket and expect to be in a lower tax bracket during their retirement years.

Roth IRA: Tax-Free Growth and Withdrawals

Established in 1997, the Roth IRA has become a favorite among financial planners and young investors. Unlike the Traditional IRA, contributions to a Roth are made with “after-tax” dollars—meaning you don’t get a tax deduction today.

The benefit, however, is monumental: all growth and all future withdrawals are 100% tax-free, provided you follow the distribution rules. If you invest $7,000 today and it grows to $100,000 over thirty years, you can withdraw that entire six-figure sum without giving a single penny to the IRS. This is particularly advantageous for younger investors who have decades for their money to compound.

Specialized Options: SEP and SIMPLE IRAs

For the self-employed, small business owners, and freelancers, the standard contribution limits of Traditional and Roth IRAs may feel restrictive. This is where SEP (Simplified Employee Pension) IRAs and SIMPLE (Savings Incentive Match Plan for Employees) IRAs come into play.

A SEP IRA allows business owners to contribute a significant portion of their income—up to 25% of net earnings in some cases—making it a powerful tool for high-earning consultants or entrepreneurs to shield their income from taxes while building a massive retirement nest egg.

Contribution Limits, Eligibility, and Rules

To prevent the wealthy from using IRAs as unlimited tax shelters, the IRS imposes strict rules regarding how much you can contribute and who is eligible to participate.

Annual Contribution Caps and Income Phase-outs

Every year, the IRS sets a maximum limit on how much you can put into an IRA. As of 2024, the limit is $7,000 for most individuals. It is important to note that this limit applies across all your IRAs; you cannot put $7,000 into a Traditional IRA and another $7,000 into a Roth IRA in the same year.

Furthermore, Roth IRAs have “income phase-outs.” If you earn above a certain threshold (which fluctuates based on your filing status), your ability to contribute directly to a Roth IRA is reduced or eliminated. For high earners, this often necessitates the use of a “Backdoor Roth” strategy, which involves contributing to a Traditional IRA and then converting it to a Roth.

The “Catch-Up” Contribution for Older Investors

The government recognizes that many individuals may not start saving seriously until later in life. To help these individuals “catch up,” those aged 50 and older are allowed to contribute an additional $1,000 per year (for a total of $8,000 in 2024). This “catch-up contribution” can be a vital component of a late-stage retirement strategy, allowing for a final surge in tax-advantaged savings before the transition to retirement.

Withdrawal Rules and Penalties

The “R” in IRA stands for Retirement, and the IRS takes that seriously. Generally, you cannot withdraw earnings from your IRA before the age of 59½ without facing a 10% early withdrawal penalty in addition to regular income taxes.

There are, however, specific exceptions. For instance, the Roth IRA allows you to withdraw your contributions (the original money you put in) at any time without penalty, as that money has already been taxed. Other exceptions for early withdrawal include first-time home purchases (up to $10,000), qualified educational expenses, or significant medical bills. Despite these exceptions, the primary goal should always be to leave the funds untouched to maximize growth.

Strategic Investment Approaches Within an IRA

Opening an account and contributing money is only the first step. The second, and arguably more important step, is deciding how that money is invested. Because an IRA is a long-term vehicle, your investment strategy should reflect your time horizon and risk tolerance.

Asset Allocation and Diversification

A successful IRA portfolio is built on the foundation of diversification. This means spreading your investments across various asset classes—such as large-cap stocks, international equities, government bonds, and perhaps real estate investment trusts (REITs).

Diversification protects you from “systemic risk.” If one sector of the economy (like technology or energy) takes a downturn, your other investments can help stabilize the portfolio. Within an IRA, you have the freedom to rebalance your portfolio—selling winners and buying underperformers to maintain your target allocation—without triggering capital gains taxes.

Target-Date Funds vs. Self-Directed Portfolios

For many investors, the easiest path is a Target-Date Fund (TDF). You choose a fund with a year closest to your expected retirement (e.g., “Target 2055”), and the fund manager automatically adjusts the risk profile over time. When you are young, the fund is aggressive (mostly stocks); as you approach retirement, it automatically shifts toward conservative assets (mostly bonds).

For those who are more hands-on, a self-directed approach using low-cost index funds or individual stocks allows for more granular control. This can lead to higher returns if managed correctly, but it requires more time, research, and emotional discipline during market volatility.

How to Open and Manage Your IRA

Starting an IRA is a remarkably simple process that can often be completed in less than fifteen minutes, yet it is one of the most significant financial moves you can make.

Choosing the Right Brokerage or Financial Institution

Most major financial institutions offer IRAs. When choosing a provider, you should look for three things: low fees (no maintenance or setup fees), a user-friendly digital interface, and a wide selection of no-commission ETFs or mutual funds. Popular choices include major discount brokerages and “robo-advisors,” which use algorithms to manage your portfolio for a small fee.

Rollovers: Consolidating Your Retirement Savings

One of the most effective ways to grow an IRA is through a “Rollover.” When you leave a job, you typically have the option to move your 401(k) balance into an IRA. This is often a wise move, as it allows you to consolidate multiple old retirement accounts into one place, giving you better visibility of your total net worth and access to a broader range of investment choices than your former employer likely provided.

Conclusion: The Path to Financial Freedom

The Individual Retirement Account is an indispensable tool in the pursuit of financial security. By providing a structure that incentivizes long-term thinking through tax advantages, the IRA empowers the individual to take charge of their own destiny. Whether you choose the immediate tax relief of a Traditional IRA or the long-term tax-free bounty of a Roth IRA, the most important factor is consistency. By starting early, contributing regularly, and investing wisely, the IRA transforms from a mere account into a foundational pillar of wealth that ensures dignity and comfort in your later years.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.