Understanding the nature and treatment of period costs is fundamental to effective financial management and sound business decision-making. In the realm of business finance, costs are broadly categorized based on how they are recognized in financial statements. While some costs are directly tied to the production or sale of goods (known as product costs), others are expensed in the period they are incurred, regardless of sales volume. These latter costs are termed “period costs.” Grasping this distinction is crucial for accurately assessing profitability, managing cash flow, and making informed strategic choices.

The Fundamental Definition and Characteristics of Period Costs

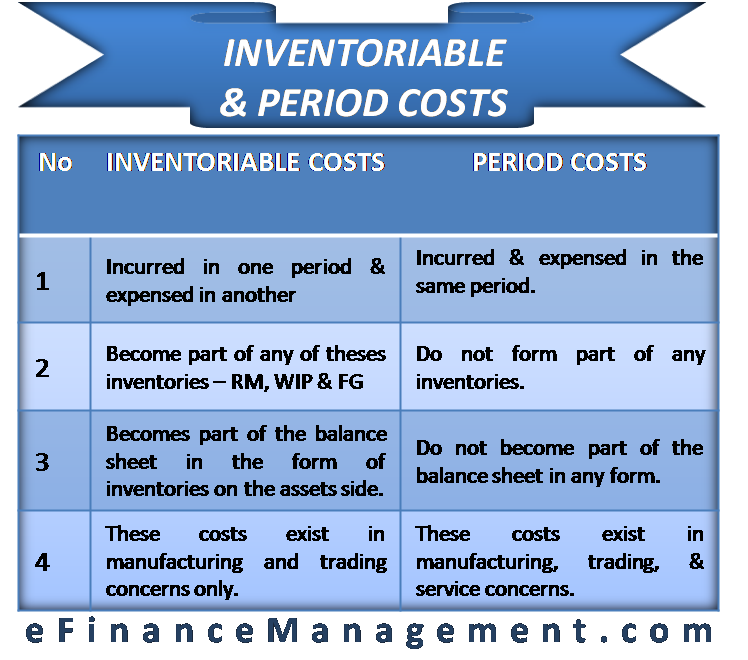

At its core, a period cost is an expense that is recognized on an income statement during the accounting period in which it is incurred, rather than being attached to the cost of inventory. This fundamental characteristic sets them apart from product costs, which are inventoried until the related goods are sold.

Distinguishing Period Costs from Product Costs

The primary differentiator between period costs and product costs lies in their relationship with the manufacturing or acquisition process of goods.

-

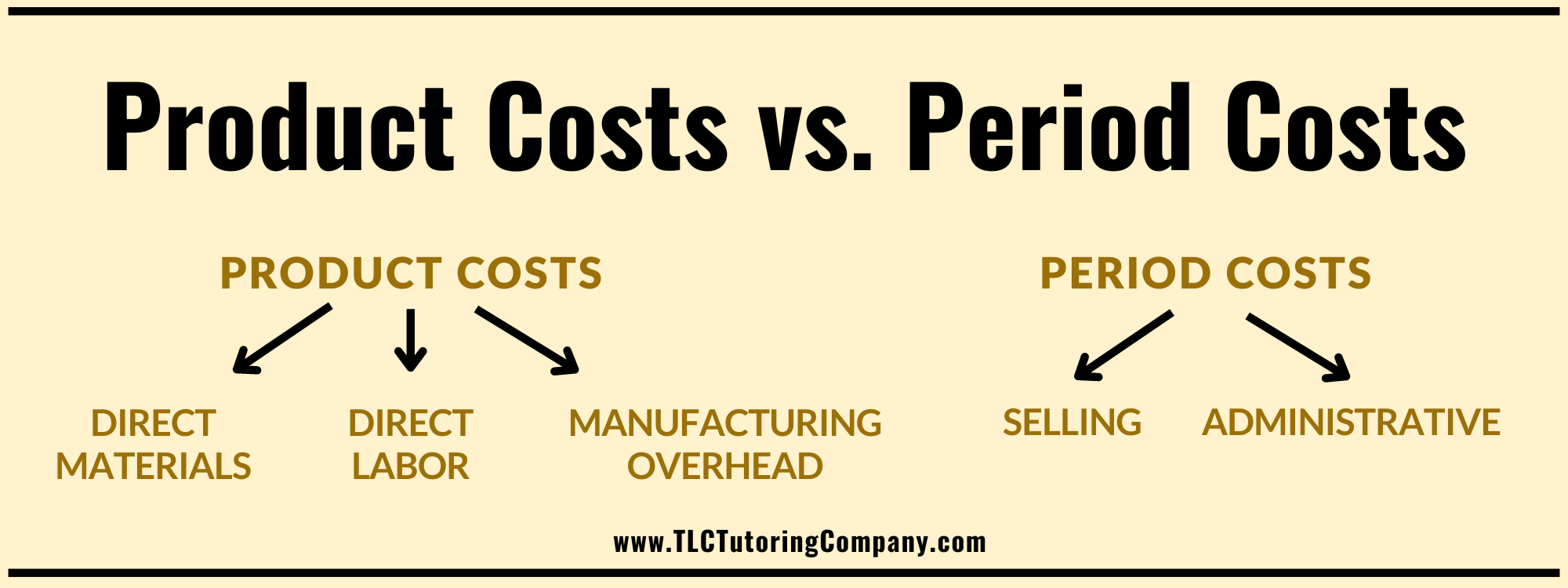

Product Costs: These costs are directly associated with bringing a product to a saleable condition. They include direct materials (the raw materials that become part of the finished product) and direct labor (the wages paid to workers directly involved in production). Additionally, manufacturing overhead, which encompasses indirect costs related to the production facility and process (e.g., factory rent, utilities for the factory, depreciation of manufacturing equipment), is also considered a product cost. Product costs are inventoried as part of the cost of goods sold (COGS) on the balance sheet until the product is sold. At that point, they are transferred to the income statement as an expense. This matching principle ensures that the cost of producing a good is recognized in the same period as the revenue generated from its sale.

-

Period Costs: In contrast, period costs are not directly related to the production process. They are incurred in the normal course of business operations but are considered to benefit the current period rather than being tied to the creation of specific inventory items. These costs are expensed as incurred on the income statement. For example, the rent for the company’s administrative offices is a period cost, as it pertains to the general operation of the business and not to the manufacturing of a specific product.

The Accounting Treatment: Expensing as Incurred

The accounting treatment of period costs is straightforward: they are charged directly to expense in the period they are incurred. This means that if a company incurs a period cost in January, that cost will appear on the January income statement, irrespective of whether any products produced in January have been sold. This “matching principle” dictates that expenses should be recognized in the same period as the revenues they help generate. However, for period costs, their benefit is often viewed as spread across the entire operating period rather than being tied to a specific revenue-generating event from a particular product.

Categorization within the Income Statement

Period costs are typically classified into two main categories on the income statement:

-

Selling Expenses: These are costs incurred to market, sell, and distribute a company’s products or services. Examples include advertising and promotion costs, sales commissions, salaries of sales staff, shipping and delivery expenses for finished goods, and depreciation of sales vehicles. These costs are essential for generating revenue but are not part of the cost of creating the product itself.

-

Administrative Expenses (General and Administrative Expenses – G&A): These are costs associated with the overall management and operation of the business, excluding selling and production costs. Examples include salaries of executives and administrative staff, rent for the corporate headquarters, office supplies, legal and accounting fees, and insurance for the general business. These expenses support the entire organization’s functioning.

Common Examples of Period Costs

To solidify understanding, examining specific examples across different business functions is invaluable. These examples illustrate how period costs manifest in the day-to-day operations of a company.

Selling Expenses in Detail

The effective marketing and distribution of goods and services are critical for any business’s success. The costs associated with these activities are categorized as selling expenses, a significant component of period costs.

-

Advertising and Marketing: Funds spent on creating and disseminating advertisements through various channels (TV, radio, online, print) are period costs. These campaigns aim to build brand awareness and drive sales, with their impact often felt broadly over time rather than being directly tied to a specific unit sold. Similarly, costs for market research, public relations activities, and promotional events fall under this umbrella.

-

Sales Salaries and Commissions: The compensation paid to the sales team, including base salaries and commissions earned on sales, are typically treated as period costs. While commissions are directly linked to sales, they are expensed in the period the sale is made, aligning with the revenue recognition for that sale. This contrasts with direct labor in manufacturing, which is inventoried.

-

Delivery and Shipping Costs: The expense incurred to deliver finished goods to customers is also a selling expense. These costs are necessary for completing the sale and satisfying the customer but are not part of the manufacturing cost of the product.

-

Depreciation of Sales-Related Assets: If a company owns vehicles used by its sales force or equipment used in its showrooms, the depreciation of these assets is considered a selling expense. This reflects the cost of using these assets to support sales activities over time.

Administrative Expenses in Detail

The operational backbone of any business relies on a robust administrative structure. The costs associated with managing and overseeing the entire enterprise are classified as administrative expenses, another key category of period costs.

-

Executive and Office Staff Salaries: The compensation for top management, administrative personnel, human resources, and accounting departments are period costs. These individuals manage the company’s overall strategy and operations, and their costs are expensed in the period their services are rendered.

-

Rent for Office Space: The cost of leasing or occupying office buildings for administrative functions is a period cost. Unlike factory rent (which is part of manufacturing overhead and thus a product cost), office rent supports general business operations.

-

Utilities for Offices: Electricity, water, and internet services for administrative offices are expensed as incurred. These are essential for maintaining an operational workspace but are not tied to product creation.

-

Legal and Accounting Fees: Professional services such as audits, tax preparation, and legal counsel are critical for compliance and governance. These fees are expensed in the period they are incurred.

- Office Supplies and Equipment Depreciation: Consumables like stationery and the depreciation of office furniture and computers used by administrative staff are also period costs.

The Significance of Period Costs in Financial Reporting and Analysis

The accurate identification and classification of period costs are not merely an accounting exercise; they have profound implications for a company’s financial health, decision-making capabilities, and overall valuation.

Impact on Profitability Measurement

The most direct impact of period costs is on the calculation of operating profit. Since period costs are expensed in the period they are incurred, they directly reduce operating income. A higher proportion of period costs, relative to revenue, will lead to lower operating profitability. Understanding this relationship allows businesses to analyze the efficiency of their selling and administrative functions. For instance, a sudden increase in advertising costs without a corresponding increase in sales could signal a need to re-evaluate marketing strategies.

Influence on Cash Flow Management

Period costs, by their nature, represent cash outflows that occur during the accounting period. Effective cash flow management requires anticipating and budgeting for these expenses. Businesses need to ensure they have sufficient liquidity to cover these ongoing operating costs. Fluctuations in period costs, such as unexpected increases in marketing expenditures or administrative overhead, can strain cash reserves if not properly planned for.

Role in Decision-Making and Strategic Planning

Accurate cost classification is essential for informed decision-making. When evaluating the profitability of a particular product line or sales initiative, management needs to distinguish between the direct costs of that initiative (which might include some period costs if directly attributable) and the overall period costs of the business. For example, when considering whether to launch a new marketing campaign, projecting the incremental selling expenses (period costs) against the anticipated increase in sales revenue is critical.

Furthermore, analyzing trends in period costs over time can provide valuable insights. A steady increase in administrative expenses, for example, might suggest inefficiencies in operations or the need for restructuring. Conversely, strategically increasing marketing expenditures might be a deliberate decision to drive future growth, and understanding this as a period cost allows for the proper accounting and expectation setting.

Implications for Investors and Stakeholders

Investors and other stakeholders rely on financial statements to assess a company’s performance and future prospects. The distinction between product and period costs significantly influences key financial metrics.

-

Gross Profit: This metric is calculated as Revenue minus Cost of Goods Sold (which includes product costs). Period costs are excluded from this calculation, meaning a company with high period costs can still have a healthy gross profit margin.

-

Operating Profit (EBIT): This is calculated by subtracting selling and administrative expenses (period costs) from gross profit. Therefore, period costs directly impact operating profit, a crucial indicator of a company’s core operational profitability.

-

Net Income: After all expenses, including interest and taxes, are deducted from operating profit, net income is determined. Period costs are a significant determinant of net income.

For investors, understanding the magnitude and trend of period costs helps them evaluate a company’s operational efficiency, its investment in growth (e.g., marketing), and its ability to manage overhead. A company that effectively controls its period costs while driving revenue is generally seen as more financially sound.

The Nuances and Considerations of Period Cost Accounting

While the definition of period costs seems straightforward, certain nuances and specific accounting rules require careful attention to ensure accurate financial reporting.

The Impact of Accrual Accounting

Period costs are accounted for under the accrual basis of accounting. This means that an expense is recognized when it is incurred, regardless of when the cash is actually paid. For example, if a company receives an invoice for advertising services in December but pays it in January, the advertising expense is recognized in December. This aligns the expense with the period in which the benefit (advertising) was received.

The Difference Between Period Costs and Deferred Expenses

It is crucial to distinguish period costs from deferred expenses, also known as prepaid expenses. While both represent costs incurred, their timing of expensing differs.

-

Deferred Expenses (Prepaid Expenses): These are costs that are paid in advance for benefits that will be received in future accounting periods. For instance, paying rent for six months in advance is a deferred expense. The portion of the rent that applies to future months is recorded as an asset (prepaid rent) on the balance sheet and is expensed over those future periods. The portion applicable to the current period is expensed as a period cost.

-

Period Costs: As discussed, these are expensed in the period they are incurred, not necessarily when they are paid. The benefit is considered to accrue within that period.

The distinction is vital because deferred expenses impact both the balance sheet (as an asset) and the income statement (as an expense over time), whereas period costs solely impact the income statement in the current period.

Industry-Specific Variations and Best Practices

While the core principles of period cost accounting are universal, specific industries may have unique considerations or reporting conventions. For instance, a software-as-a-service (SaaS) company might incur significant period costs in research and development, marketing, and customer support, all of which are crucial for its recurring revenue model. Understanding the specific cost structure and operational drivers of an industry is essential for appropriate classification and analysis.

Furthermore, companies often establish internal policies and procedures for classifying and tracking period costs. These policies should be consistent, well-documented, and aligned with generally accepted accounting principles (GAAP) or International Financial Reporting Standards (IFRS). Regular review of these policies ensures they remain relevant and effective as the business evolves.

In conclusion, period costs are an indispensable aspect of business finance. Their accurate identification, proper accounting treatment, and insightful analysis are fundamental to understanding a company’s financial performance, managing its cash flow, and making sound strategic decisions. By distinguishing them from product costs and understanding their impact on profitability and stakeholder perceptions, businesses can navigate the complexities of financial management more effectively.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.