Navigating the landscape of personal finance requires a delicate balance between wealth accumulation and risk mitigation. For most individuals, one of the most significant recurring expenses—and essential safety nets—is automobile insurance. Specifically, the question of “how much is full coverage car insurance” is not merely about a monthly premium; it is about understanding the cost of protecting one of your most valuable mobile assets.

While the term “full coverage” is widely used by consumers, it is technically a misnomer in the insurance industry. It typically refers to a combination of several policy types that, when bundled together, provide comprehensive financial protection against a wide array of risks. In this guide, we will break down the costs, the contributing factors, and the strategic financial decisions involved in securing full coverage.

Defining Full Coverage in the Context of Your Financial Plan

To understand the cost, one must first understand the components. From a financial management perspective, car insurance is a transfer of risk. By paying a premium, you transfer the potential for a catastrophic financial loss to an insurance company. “Full coverage” generally consists of three primary pillars.

Collision Coverage: Protecting Your Asset

Collision insurance covers the cost of repairing or replacing your vehicle if you are involved in an accident with another vehicle or an object, regardless of who is at fault. From a personal finance standpoint, this is essential if you do not have the liquid cash flow to replace your vehicle out of pocket. If you are financing or leasing a car, the lender will almost certainly require this coverage to protect their investment.

Comprehensive Coverage: Guarding Against the Unforeseen

While collision handles road accidents, comprehensive coverage handles “acts of God” and non-collision events. This includes theft, vandalism, fire, falling objects, and natural disasters like floods or hail. Without comprehensive coverage, a sudden storm or a stolen vehicle could result in a total loss of the capital you’ve invested in your car.

The Difference Between State Minimums and Full Protection

Most states require a bare minimum of liability insurance, which pays for the other person’s medical bills and property damage if you are at fault. However, liability insurance does nothing for your own financial recovery. Transitioning from state-minimum liability to full coverage represents a significant jump in premiums, often doubling the cost, but it provides the peace of mind that your personal net worth won’t be decimated by a single driving error or a theft.

Key Factors That Influence Your Insurance Premiums

Insurance companies use complex actuarial tables to determine risk. When you ask for a quote, the “how much” is determined by a myriad of data points that categorize you into a specific risk bracket.

Personal Demographics and Location

Age and gender are historically significant factors; younger drivers, particularly those under 25, are statistically more likely to be involved in accidents, leading to higher premiums. However, location is often the most overlooked variable. Your ZIP code dictates the frequency of accidents in your area, the rate of local vehicle theft, and even the likelihood of weather-related claims. Living in a densely populated urban center like New York City or Miami will inevitably lead to higher “full coverage” costs than living in a rural area.

Vehicle Value and Repair Costs

The type of car you drive is a direct multiplier of your premium. A luxury SUV with high-tech sensors and expensive bodywork costs more to insure because it costs the insurer more to repair. Conversely, a vehicle with high safety ratings and readily available parts may be cheaper to insure. Financial experts often suggest researching insurance costs before purchasing a vehicle, as the annual insurance premium can sometimes rival the cost of the car loan interest itself.

Credit Score and Financial History

In many states, insurance companies use a “credit-based insurance score.” This is a controversial but standard practice in the money niche. Actuarial data suggests a correlation between financial responsibility and driving safety. If you have a high credit score, insurers view you as a lower risk, potentially saving you hundreds of dollars annually on full coverage premiums. Improving your credit score is, therefore, a direct strategy for lowering your insurance overhead.

The Average Cost of Full Coverage: National Trends and Data

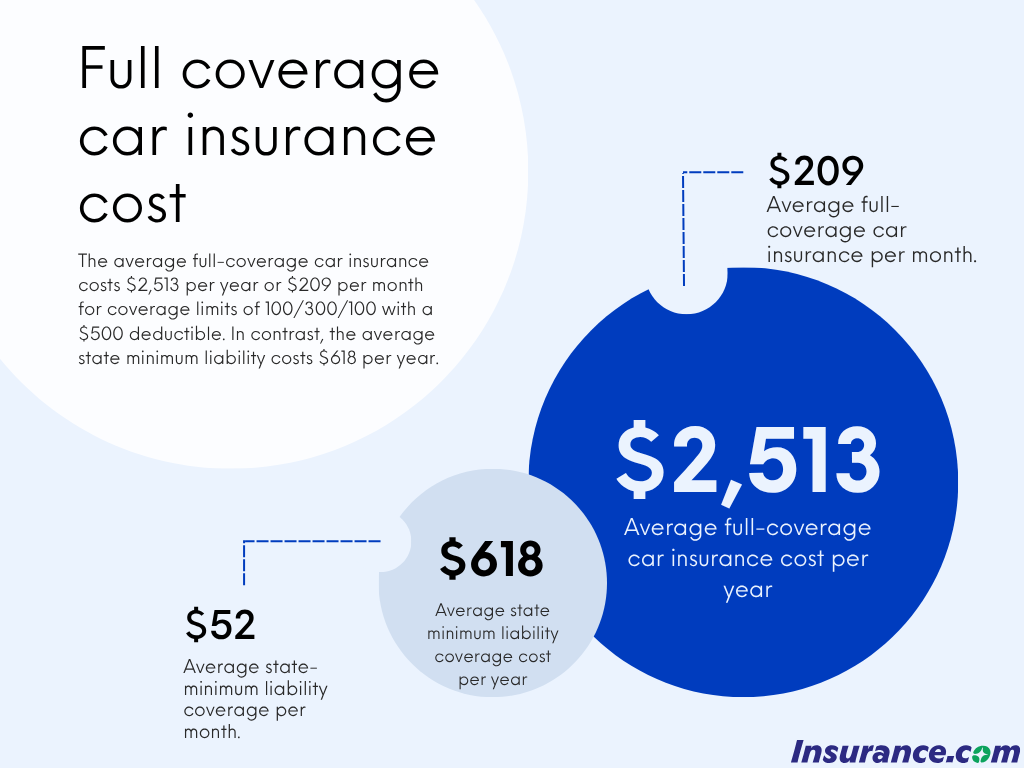

While individual rates vary, we can look at national averages to establish a baseline for your budget. As of current market trends, the average cost of full coverage car insurance in the United States hovers between $1,800 and $2,500 per year, or roughly $150 to $210 per month.

Breaking Down the Monthly and Annual Averages

When budgeting for car insurance, it is vital to look at the total “cost of ownership.” If your monthly car payment is $400 and your full coverage insurance is $200, your true monthly cost is $600. For many drivers, the jump from “liability only” (which may cost $600 a year) to “full coverage” (which may cost $2,100) is a $1,500 annual investment in risk management.

Why Rates Vary Significantly by State

Insurance is regulated at the state level, leading to massive price disparities. For instance, drivers in Michigan or Florida often face some of the highest rates in the country due to specific state laws regarding “no-fault” insurance or high rates of litigation and uninsured drivers. On the other hand, states like Maine or Idaho often see full coverage rates that are 30% to 50% lower than the national average. Understanding your local market is key to knowing if you are overpaying.

Strategies to Lower Your Premiums Without Sacrificing Protection

Achieving a lower premium doesn’t always mean you have to reduce your coverage levels. There are several financial maneuvers you can employ to optimize your insurance spend.

Leveraging Deductibles for Lower Monthly Costs

A deductible is the amount you pay out of pocket before your insurance kicks in. In the world of personal finance, choosing a higher deductible (moving from $500 to $1,000, for example) can significantly lower your monthly premium. This is a wise move if you have a healthy emergency fund. You are essentially “self-insuring” the first $1,000 of damage in exchange for a lower fixed monthly cost.

Utilizing Discounts and Bundling Options

The “bundling” of services is a cornerstone of corporate marketing and a benefit to the consumer’s wallet. Insuring your home and auto with the same provider often results in a 10% to 25% discount on both policies. Furthermore, look for discounts related to your profession, military service, or even “good student” discounts for young drivers on your policy.

The Role of Telematics in Modern Insurance Pricing

Many insurers now offer “usage-based insurance” or telematics. By installing a small device in your car or using a smartphone app, the insurer tracks your braking, speed, and mileage. If you are a safe, low-mileage driver, you can earn substantial discounts. This is particularly effective for people who work from home and do not have a daily commute, as they are statistically exposed to much less risk.

Is Full Coverage Worth the Investment? A Cost-Benefit Analysis

As a vehicle ages, the financial argument for maintaining full coverage changes. At a certain point, the cost of the insurance premium may outweigh the potential payout from the insurance company.

Assessing the Value of Your Vehicle

A common rule of thumb in the money niche is the “10% Rule.” If your annual premium for collision and comprehensive coverage exceeds 10% of your car’s total book value (e.g., paying $1,000 a year to insure a car worth $8,000), it might be time to reconsider. If your car is worth only $3,000 and your deductible is $1,000, the maximum you could ever “win” in a claim is $2,000. If you are paying $800 a year for that protection, it may be more financially sound to drop to liability-only and put that $800 into a dedicated car savings account.

Understanding Your Risk Tolerance and Liquidity

The decision to carry full coverage is ultimately about your personal liquidity. If your car is totaled tomorrow, do you have the cash to buy another one? If the answer is no, full coverage is a non-negotiable expense. It serves as a financial backstop that prevents a car accident from turning into a debt crisis.

In conclusion, “how much” full coverage costs is a variable figure that depends on your location, your car, and your habits. However, by understanding the mechanics of these policies and applying savvy financial strategies—like improving your credit score and optimizing deductibles—you can secure the protection you need at a price that fits within your broader financial goals. Insurance is not just a bill; it is a foundational component of a secure financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.