In the world of finance, precision is not merely a preference; it is a requirement. Whether you are analyzing a corporate balance sheet, calculating the interest on a high-yield savings account, or determining your asset allocation in a diversified portfolio, the ability to convert fractions into decimals is a foundational skill. While the question “what is 3/5 as a decimal” may seem like a relic of elementary mathematics, its implications in personal finance, investment strategy, and business scaling are profound.

To answer the primary question: 3/5 as a decimal is 0.6.

While the numerical answer is simple, the application of this value—representing 60%—is a critical component of financial literacy. In this guide, we will explore the mathematical mechanics of this conversion and delve into how this specific ratio functions as a cornerstone for financial decision-making, budgeting, and wealth accumulation.

The Mathematical Foundation: Converting 3/5 to a Decimal

Before applying the number to a brokerage account or a business ledger, one must understand the absolute clarity that decimals provide over fractions. Fractions represent a part of a whole, but decimals allow for standardized comparison across various financial instruments.

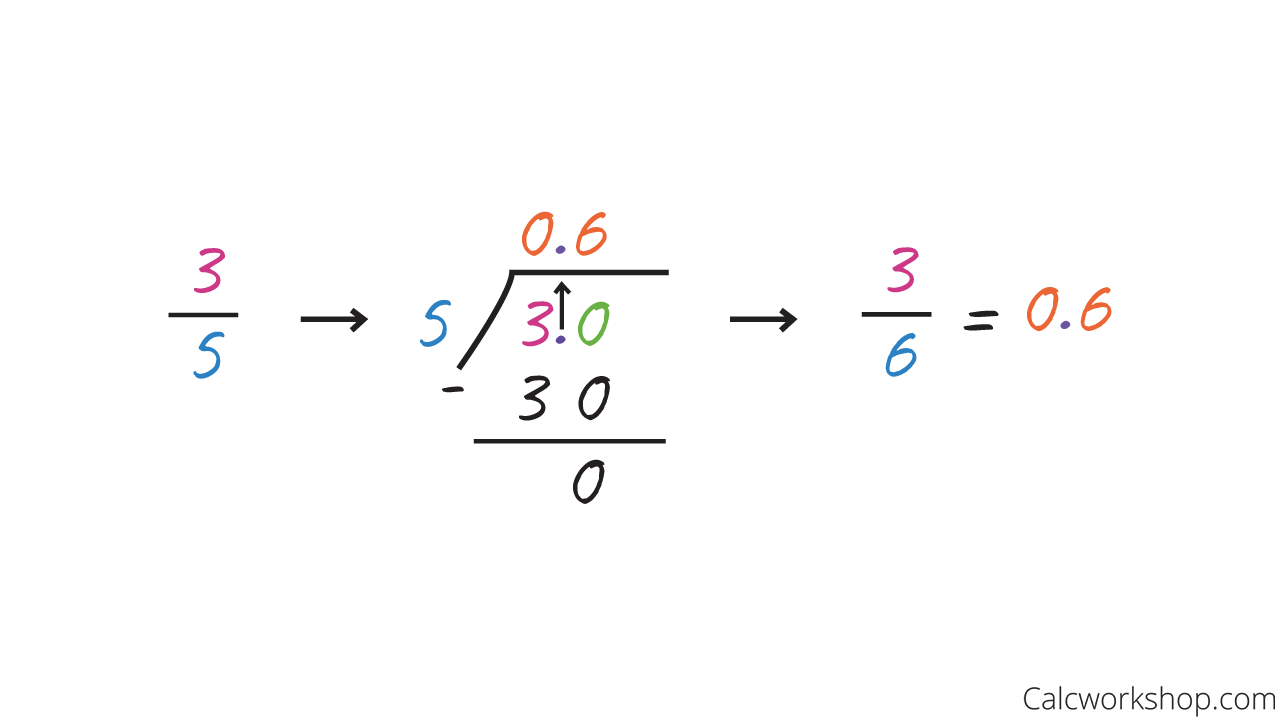

The Division Method

The most direct way to convert any fraction to a decimal is through the division of the numerator (the top number) by the denominator (the bottom number). In this case, we divide 3 by 5. Since 5 does not go into 3, we add a decimal point and a zero, making it 30. 5 goes into 30 exactly 6 times. Therefore, the result is 0.6. In a financial context, this represents a “factor” of 0.6, which is used to multiply principal amounts to determine a specific portion of capital.

The Equivalent Fraction Method (Base 10)

In finance, we often think in terms of “cents” or “percentages,” both of which are based on the number 100. To convert 3/5 into a base-100 decimal, we multiply both the numerator and the denominator by a factor that turns the denominator into 10 or 100. Multiplying 3/5 by 2/2 gives us 6/10, which is 0.6. Multiplying it by 20/20 gives us 60/100, which is 0.60. This 0.60 represents 60%, a figure that appears frequently in dividend payout ratios and tax brackets.

From Math to Money: Why Decimals Matter in Personal Finance

In the realm of personal finance, we rarely deal with fractions. You won’t find a credit card statement listing an interest rate as 1/8; it will be listed as 0.125 or 12.5%. Converting 3/5 to 0.6 is the first step in understanding the “sixty-percent rule” and other quantitative benchmarks.

Precision in Interest Rates and APY

When dealing with compound interest, the difference between a fraction and a decimal can mean the difference between accurate forecasting and a costly error. If an investment vehicle has a fee structure or an interest adjustment of 3/5 of a percentage point, knowing that this equals 0.6% is vital. Over a 30-year investment horizon, a 0.6% difference in fees can result in tens of thousands of dollars in lost gains due to the erosion of compounding returns. Professional investors use decimals to calculate the “expense ratio,” and a 0.6 decimal factor is a common benchmark for actively managed funds.

Calculating Investment Returns and Yields

If you hold a portfolio where 3 out of every 5 dollars are invested in equities, your decimal allocation is 0.6. This decimal allows you to quickly calculate your weighted average return. For example, if your equities return 10%, you multiply 0.10 by 0.6 to see that equities contributed 6% to your total portfolio growth. Decimals simplify the “weighting” process in modern portfolio theory, allowing for a more granular view of risk and reward than bulky fractions ever could.

The Power of 0.6: Applying the 3/5 Ratio to Budgeting and Allocation

The decimal 0.6 represents the majority. In many financial frameworks, 60% is a “tipping point” for stability and growth. Understanding how to manage 0.6 of your income or capital is essential for long-term solvency.

The 60% Rule for Fixed Expenses

Many financial advisors suggest a variation of the “Balanced Money Formula.” While the 50/30/20 rule is popular, a more conservative approach for high-cost-of-living areas is the 60% rule. This strategy dictates that 3/5 (0.6) of your gross income should cover all “committed expenses,” including housing, insurance, utilities, and taxes. By keeping these fixed costs at 0.6, an individual ensures that 40% of their capital remains liquid for debt repayment, aggressive investing, and discretionary spending.

Portfolio Diversification and Asset Allocation

In institutional investing, a 60/40 split (0.6 in stocks and 0.4 in bonds) has historically been the “Gold Standard” for a balanced portfolio. This 3/5 allocation to equities is designed to capture market growth while the remaining 2/5 provides a buffer against volatility. When a market rally pushes your stock allocation to 0.65 or 0.7, a disciplined investor will “rebalance” back to the 0.6 decimal. This process—selling high and buying low—is made possible by the constant monitoring of these decimal ratios.

Corporate Finance and Strategic Business Growth

Beyond personal wealth, the decimal 0.6 (3/5) plays a pivotal role in corporate strategy, specifically regarding ownership, margins, and debt capacity.

Profit Margins and Revenue Ratios

For a business to be considered “healthy” in many service-based industries, a gross profit margin of 0.6 is often the target. If a company spends $2 to produce a product and sells it for $5, the profit is $3. The margin is 3/5, or 0.6. This 60% margin provides the necessary cash flow to cover overhead, marketing, and research and development. Investors looking at “unit economics” prioritize businesses that can maintain a 0.6 decimal ratio because it indicates high scalability and pricing power.

Understanding Majority Stakes and Ownership

In the world of mergers and acquisitions (M&A), the 3/5 ratio is a powerful threshold. Owning 0.6 of a company’s shares represents a “supermajority” in many corporate bylaws. While 0.51 (51%) grants control, 0.6 (60%) often allows a shareholder to bypass certain minority protections, approve major structural changes, or force a sale. For entrepreneurs, maintaining an ownership decimal above 0.6 ensures that they retain the ultimate vision of the brand without being overruled by venture capital boards.

Debt-to-Equity and Leverage

Financial analysts use decimals to measure a company’s risk profile. A debt-to-equity ratio of 0.6 (where debt is 3/5 of equity) suggests a moderately leveraged company. In a low-interest-rate environment, using 0.6 leverage can amplify returns on equity. However, if the decimal creeps closer to 1.0 or higher, the business becomes “over-leveraged,” increasing the risk of insolvency during a market downturn. Professional money managers use these decimal calculations to determine the creditworthiness of a corporation before purchasing its bonds.

The Technological Edge: Quantitative Calculation in the Digital Age

As we move further into a tech-driven financial landscape, the conversion of 3/5 to 0.6 is handled by algorithms, but the human understanding of that value remains irreplaceable.

Algorithmic Trading and Decimalization

The stock market transitioned from fractions to decimals (decimalization) in the early 2000s. Before this, stocks were traded in 1/8ths or 1/16ths. The shift to decimals allowed for narrower “bid-ask spreads,” saving investors billions of dollars. Today, high-frequency trading (HFT) algorithms operate in decimals carried out to eight or ten places. To these machines, 0.6 is a precise data point used to execute trades in microseconds. Understanding the math behind the decimal allows investors to understand how these digital tools value assets in real-time.

The Psychology of 0.6 in Marketing and Pricing

In the psychology of money, 0.6 has a specific impact. Prices ending in .60 are less common than those ending in .99, often used by brands to signal “wholesale” or “calculated” value rather than a marketing gimmick. Furthermore, when a business offers a “3 for 5” deal, the consumer’s brain must quickly translate that to a 0.6 unit cost to determine if the deal provides actual value compared to a single unit. Being able to perform this decimal conversion mentally protects a consumer’s “money” from predatory pricing tactics.

Conclusion: The Value of Quantitative Literacy

What is 3/5 as a decimal? It is 0.6. But as we have explored, it is also a 60% profit margin, a 60/40 balanced investment portfolio, a supermajority in corporate governance, and a benchmark for personal budgeting.

In the pursuit of financial independence, the ability to see the world in decimals rather than just whole numbers is a superpower. It allows for the precise measurement of growth, the accurate assessment of risk, and the disciplined execution of a wealth-building strategy. By mastering these simple mathematical conversions, you equip yourself with the quantitative tools necessary to navigate the complexities of the modern financial world, ensuring that every cent—or every 0.01—is working toward your ultimate goal of financial freedom.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.