Purchasing a car is a significant financial decision for most individuals and families. Beyond the excitement of choosing a model and color, the practical reality of how to pay for it often looms large. Understanding how car payments are calculated is not just about crunching numbers; it’s about empowering yourself to make informed decisions, avoid unnecessary debt, and ensure the vehicle fits comfortably within your financial landscape. This comprehensive guide will demystify the process, breaking down the core components, presenting the fundamental formulas, and offering strategies to help you navigate the complexities of car financing with confidence. By the end of this article, you’ll have a clear roadmap to understanding, calculating, and ultimately budgeting for your next vehicle purchase.

Understanding the Core Components of a Car Payment

A car payment isn’t just a random figure; it’s the result of several interconnected variables. Grasping each component is the first step toward accurately calculating your monthly obligation and understanding its impact on your long-term financial health.

The Principal Loan Amount: Price, Down Payment, and Trade-in Value

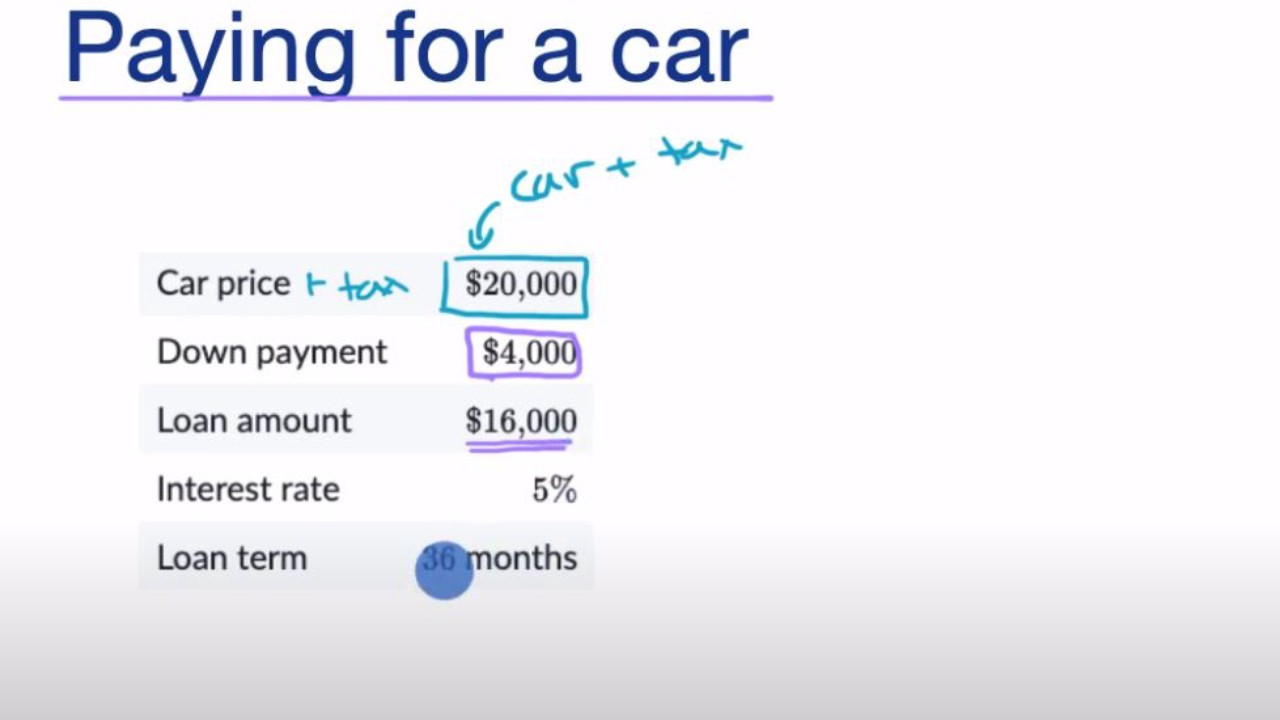

The principal loan amount is the actual sum of money you borrow to purchase the car. This isn’t necessarily the sticker price; it’s the agreed-upon sale price of the vehicle, minus any down payment you make and the value of any trade-in vehicle.

- Sale Price: This is the negotiated price of the car itself. Always aim to negotiate the price before discussing financing or trade-ins, as it forms the baseline for everything else.

- Down Payment: A down payment is the initial amount of money you pay upfront. A larger down payment directly reduces the principal loan amount, meaning you borrow less, which in turn leads to lower monthly payments and less interest paid over the life of the loan. Financial experts often recommend a down payment of at least 20% for new cars and 10% for used cars to mitigate depreciation and reduce your loan-to-value ratio.

- Trade-in Value: If you have an existing vehicle, trading it in can act like an additional down payment. The agreed-upon trade-in value is deducted from the sale price, further reducing the amount you need to finance. It’s often wise to research your car’s trade-in value independently (e.g., via Kelley Blue Book or Edmunds) before heading to the dealership.

For example, if a car’s sale price is $30,000, and you put down $5,000 and trade in a car worth $3,000, your principal loan amount would be $30,000 – $5,000 – $3,000 = $22,000.

Interest Rate (APR)

The interest rate, often expressed as Annual Percentage Rate (APR), is the cost of borrowing money. It’s a percentage charged by the lender on the principal loan amount. A higher APR means you’ll pay more in interest over the life of the loan, significantly increasing your total cost of ownership.

Several factors influence the APR you qualify for:

- Credit Score: This is the most critical factor. Borrowers with excellent credit scores (generally 720+) qualify for the lowest rates, as they are deemed lower risk. Poor credit scores will result in much higher APRs, sometimes into double digits.

- Loan Term: Shorter loan terms often come with slightly lower interest rates, as the lender’s risk is contained over a shorter period.

- Lender: Different lenders (banks, credit unions, dealership finance departments) offer varying rates, making it crucial to shop around.

- Market Conditions: Broader economic factors and the prime lending rate can also influence car loan interest rates.

Even a difference of one or two percentage points in APR can translate into hundreds or thousands of dollars over a multi-year loan. Understanding your credit score and improving it before applying for a car loan can save you a substantial amount of money.

Loan Term (Duration)

The loan term is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or 84 months). The loan term has a direct and inverse relationship with your monthly payment and a direct relationship with the total interest paid.

- Longer Terms: A longer loan term (e.g., 72 or 84 months) results in lower monthly payments, making the car seem more affordable in the short term. However, you’ll pay significantly more in total interest because the principal takes longer to be paid down, and interest accrues over an extended period. Longer terms also increase the likelihood of being “upside down” on your loan (owing more than the car is worth), especially with rapid initial depreciation.

- Shorter Terms: A shorter loan term (e.g., 36 or 48 months) results in higher monthly payments. While these payments are larger, you pay substantially less in total interest over the life of the loan. This means you own the car outright faster and save money in the long run.

Choosing the right loan term involves balancing your monthly budget with your desire to minimize total interest paid. Financial advisors often recommend keeping car loan terms to 60 months or less whenever possible.

The Formula for Calculating Car Payments

While online calculators are convenient, understanding the underlying formula provides a deeper insight into how your payment is derived. The standard formula for calculating a fixed-rate loan payment, which car loans typically are, is as follows:

Demystifying the Payment Formula

The formula used to calculate a monthly car payment is:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1 ]

Let’s break down each variable:

- M = Your monthly loan payment. This is the value you are trying to find.

- P = The principal loan amount. As discussed, this is the amount you are borrowing after the down payment and trade-in.

- i = Your monthly interest rate. This is derived from your annual interest rate (APR) divided by 12 (for 12 months in a year). So, if your APR is 6%, then

i = 0.06 / 12 = 0.005. It’s crucial to convert the percentage to a decimal. - n = The total number of payments. This is your loan term in years multiplied by 12. For example, a 5-year loan would have

n = 5 * 12 = 60payments.

This formula essentially calculates the constant payment required to amortize a loan over a set period, given a specific principal and interest rate. The numerator determines how much interest is compounded and how much principal needs to be paid down monthly, while the denominator accounts for the total number of payments over the loan’s life.

Practical Application: Step-by-Step Calculation Example

Let’s put the formula into action with a hypothetical scenario:

- Principal (P): $25,000

- Annual Interest Rate (APR): 5%

- Loan Term: 60 months (5 years)

Step 1: Calculate the monthly interest rate (i)

- APR = 5% = 0.05

i = 0.05 / 12 = 0.00416667

Step 2: Determine the total number of payments (n)

- Loan term = 60 months

n = 60

Step 3: Plug the values into the formula:

M = 25000 [ 0.00416667 * (1 + 0.00416667)^60 ] / [ (1 + 0.00416667)^60 – 1 ]

Let’s calculate the parts:

(1 + i) = 1.00416667(1 + i)^n = (1.00416667)^60 ≈ 1.283359

Now substitute back into the formula:

M = 25000 [ 0.00416667 * 1.283359 ] / [ 1.283359 – 1 ]M = 25000 [ 0.0053473 ] / [ 0.283359 ]M = 133.6825 / 0.283359M ≈ 471.86

So, your estimated monthly payment would be approximately $471.86.

This calculation shows that for a $25,000 loan at 5% over 60 months, you would pay $471.86 per month. Over the 60 months, you would pay a total of $471.86 * 60 = $28,311.60. The total interest paid would be $28,311.60 – $25,000 = $3,311.60.

Beyond the Basic Calculation: Hidden Costs and Considerations

While the core loan payment is a major factor, it’s crucial to remember that the total cost of owning a car extends far beyond this single number. Ignoring these additional expenses can lead to budget shortfalls and financial stress.

Sales Tax, Fees, and Registration

These are often overlooked but significant upfront or rolled-into-the-loan costs.

- Sales Tax: Most states levy a sales tax on vehicle purchases. This can be a few percentage points of the car’s price. Depending on your state, this tax might be added to your loan principal, increasing your monthly payment and the total interest you pay, or it may need to be paid out-of-pocket at the time of purchase.

- Documentation Fees (Doc Fees): Dealerships charge these fees for processing paperwork. They can vary widely by state and dealership, ranging from under $100 to several hundred dollars. While they are usually non-negotiable, it’s good to be aware of them.

- Registration and Licensing Fees: You’ll need to pay to register your vehicle with the state and obtain license plates. These fees vary by state, vehicle type, and sometimes even vehicle weight or value. These are typically annual costs but must be factored into the initial purchase.

Always ask for an “out-the-door” price that includes all taxes, fees, and charges before signing any agreements to get a complete picture of the total vehicle cost.

Car Insurance Costs

Car insurance is a legal requirement in almost every state and a significant ongoing expense that must be factored into your monthly budget. The cost of insurance can vary dramatically based on numerous factors:

- Vehicle Type: More expensive, high-performance, or frequently stolen cars typically cost more to insure.

- Your Driving Record: A clean driving history with no accidents or violations will result in lower premiums.

- Your Location: Urban areas with higher traffic density and theft rates often have higher insurance costs.

- Your Age and Gender: Younger, less experienced drivers generally pay more.

- Coverage Levels: Opting for comprehensive and collision coverage (often required by lenders) will increase your premiums compared to basic liability.

- Credit Score: In many states, your credit score can influence your insurance rates.

It’s highly recommended to get insurance quotes for specific vehicles you’re considering before committing to a purchase. A seemingly affordable car payment can become prohibitive when combined with high insurance premiums.

Maintenance and Fuel Expenses

Beyond the initial purchase and mandatory insurance, cars require ongoing operational costs that can significantly impact your budget.

- Fuel: The type of car you buy (e.g., fuel-efficient compact vs. large SUV) directly impacts your weekly or monthly fuel budget. Consider your typical commute and annual mileage.

- Scheduled Maintenance: Cars require regular oil changes, tire rotations, fluid checks, and other service appointments based on mileage or time. Neglecting these can lead to more expensive repairs down the line. New cars often come with a warranty, but regular maintenance is still required and often not covered.

- Repairs: Even new cars can occasionally require repairs, and older cars are more prone to them. Setting aside an emergency fund for unexpected repairs is a wise financial practice.

- Tires: Tires wear out and need to be replaced every few years, which can be a significant expense, especially for larger vehicles.

These ongoing costs might not seem as impactful as a monthly car payment, but they accumulate and can easily add another $100-$300+ to your monthly vehicle expenses, depending on the car and your driving habits.

Tools and Strategies for Smarter Car Financing

Navigating car financing can be complex, but several tools and strategies can simplify the process, help you make more informed decisions, and potentially save you money.

Online Car Payment Calculators

These ubiquitous tools are invaluable for quickly estimating payments and comparing different scenarios. Most reputable financial websites, bank lending pages, and even dealership sites offer them.

- Ease of Use: Simply input the principal loan amount, interest rate (APR), and loan term, and the calculator instantly provides an estimated monthly payment.

- Scenario Planning: They allow you to easily adjust variables. Want to see how a larger down payment impacts your monthly cost? Or how extending the loan term affects your total interest paid? Online calculators make this comparison effortless, helping you identify the sweet spot between affordability and total cost.

- Budgeting Aid: By trying different combinations, you can quickly determine what fits within your monthly budget constraints without committing to anything.

Always use a few different calculators from trusted sources, as slight variations in rounding or formula implementation might exist, though results should be very similar.

Pre-Approval vs. Dealership Financing

Securing loan pre-approval from a bank or credit union before you visit a dealership is one of the most powerful strategies for car buyers.

- Know Your Rate: Pre-approval gives you a concrete interest rate and maximum loan amount before you even start negotiating. This provides a clear benchmark.

- Negotiating Leverage: With pre-approval in hand, you’re buying the car with cash in the dealership’s eyes. This separates the car price negotiation from the financing negotiation, allowing you to focus on getting the best vehicle price.

- Competitive Offers: Dealerships will often try to beat your pre-approved rate to earn the financing business. This creates healthy competition, potentially leading to an even better deal for you.

- Avoid Pressure: You won’t feel pressured to accept the dealership’s first financing offer if you already have a better one.

While dealerships can sometimes offer competitive rates, especially through manufacturer incentives, having your own financing ready gives you control and confidence.

The 20/4/10 Rule

While not a rigid law, the “20/4/10 Rule” is a widely recommended guideline for responsible car buying:

- 20% Down Payment: Aim to put down at least 20% of the car’s purchase price. This reduces the amount you finance, minimizes interest paid, and helps avoid being “upside down” on your loan as the car depreciates.

- 4-Year (48-month) Loan Term: Try to keep your loan term to four years or less. This significantly reduces the total interest you pay and ensures you build equity faster. While longer terms offer lower monthly payments, the increased interest cost often outweighs the perceived monthly savings.

- 10% of Gross Income: All your car-related expenses (monthly payment, insurance, fuel, maintenance) should ideally not exceed 10% of your gross (pre-tax) monthly income. This ensures your car doesn’t become a disproportionate drain on your overall budget, leaving room for other financial goals and emergencies.

Adhering to rules like 20/4/10 helps promote long-term financial stability and prevents you from overextending yourself for a vehicle.

Making an Informed Decision: Budgeting for Your Car

Ultimately, the goal of understanding car payments is to make a financial decision that serves your needs without compromising your financial well-being. This requires a holistic view of your budget and future goals.

Assessing Your Financial Capacity

Before you even start looking at cars, take a hard look at your personal finances.

- Current Budget: Analyze your current income, fixed expenses (rent/mortgage, utilities, existing loan payments), and variable expenses (groceries, entertainment).

- Disposable Income: Determine how much disposable income you genuinely have each month. Be realistic and avoid “payment stretching” – choosing a longer loan term just to fit a more expensive car into a tight budget.

- Savings Goals: Consider how a new car payment will impact your ability to save for other important goals, such as retirement, a down payment on a home, or your emergency fund.

- Credit Health: Check your credit score and report. This will give you an idea of the interest rates you can expect and highlight any errors that need correcting.

A car should enhance your life, not become a financial burden. Be honest with yourself about what you can truly afford.

The Total Cost of Ownership (TCO)

While car payment calculations focus on the financing aspect, remember to consider the Total Cost of Ownership (TCO) when making your purchase decision. TCO encompasses not just the loan payments, but also:

- Depreciation: The loss in value of your car over time. This is often the largest “cost” of owning a new car.

- Insurance: As discussed, a significant ongoing expense.

- Fuel: Your regular commuting and travel costs.

- Maintenance & Repairs: Routine servicing and unexpected fixes.

- Taxes and Fees: Annual registration, property taxes (in some states), etc.

Understanding the TCO allows you to compare different vehicles comprehensively, not just by their sticker price or monthly payment. A cheaper car might have higher maintenance costs, or a more expensive car might offer superior fuel efficiency and lower depreciation, making its TCO surprisingly competitive.

By taking a holistic approach and considering all these factors, you ensure that your new car is a smart investment, not a financial trap.

Calculating car payments involves understanding the interplay of principal, interest, and loan term, but responsible car ownership extends far beyond these numbers. By familiarizing yourself with the formula, utilizing online tools, securing pre-approval, and adhering to sound financial guidelines like the 20/4/10 rule, you can confidently navigate the car buying process. Always remember to factor in additional costs like taxes, insurance, fuel, and maintenance to arrive at a true total cost of ownership. Armed with this knowledge, you are well-equipped to make a financially savvy decision that secures the vehicle you need without jeopardizing your broader financial health.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.