For many Americans, Social Security serves as the bedrock of their retirement strategy. It is the one guaranteed source of inflation-adjusted income that continues for life. However, one of the most common questions financial advisors receive is: “How much is Social Security per month?” The answer is rarely a single, static figure. Instead, your monthly benefit is a variable outcome dictated by your earnings history, the age at which you choose to claim, and external economic factors like inflation.

Understanding the mechanics of Social Security is essential for effective personal finance management. Whether you are decades away from retirement or standing on the precipice of your golden years, knowing how to estimate and maximize your monthly check is a critical component of wealth preservation and income planning.

Understanding the Foundation: How the Social Security Benefit is Calculated

The Social Security Administration (SSA) uses a complex formula to determine your monthly payment, but it all begins with your work history. Unlike some pension plans that may only look at your final years of employment, Social Security considers your entire career.

The Role of Work Credits and Eligibility

Before you can receive a single dollar, you must earn enough “credits.” In 2024, you receive one credit for every $1,730 in earned income, up to a maximum of four credits per year. To qualify for retirement benefits, most people need 40 credits, which equates to roughly ten years of work. This ensures that the system is supported by those who have contributed through payroll taxes over a significant period.

AIME and PIA: The Mathematical Backbone

Once eligibility is established, the SSA looks at your 35 highest-earning years. These earnings are “indexed” to account for changes in average wages over time, ensuring that $20,000 earned in 1985 is compared fairly to $80,000 earned in 2023. These 35 years are averaged and divided by 12 to find your Average Indexed Monthly Earnings (AIME).

From there, a formula is applied to your AIME to determine your Primary Insurance Amount (PIA). The PIA is the base amount you would receive if you retired exactly at your Full Retirement Age (FRA). The formula is progressive, meaning it replaces a higher percentage of income for lower earners than it does for higher earners, though high earners still receive a larger absolute dollar amount.

The Impact of High-Earning Years

If you have fewer than 35 years of work history, the SSA fills in the remaining years with zeros. This can significantly drag down your monthly average. Conversely, if you have already worked 35 years but are currently in a high-earning phase of your career, every additional year you work replaces a lower-earning year from your youth. This is one of the most effective ways to “boost” your monthly benefit in the final stretch of your career.

The Critical Timing: Age of Filing and Your Monthly Payout

While your PIA is the baseline, the actual amount that hits your bank account each month depends heavily on when you decide to flip the switch. You can claim as early as age 62 or as late as age 70.

Full Retirement Age (FRA) Explained

Your Full Retirement Age is the point at which you receive 100% of your calculated PIA. For anyone born in 1960 or later, the FRA is 67. If you were born earlier, your FRA might be 66 and a few months. Filing at exactly this age ensures you get exactly what the formula calculated based on your earnings history.

The Cost of Early Filing at Age 62

Financial necessity or health concerns often drive individuals to file for Social Security as soon as they become eligible at age 62. However, this comes at a permanent cost. If your FRA is 67 and you file at 62, your monthly benefit is reduced by approximately 30%. This reduction is permanent and stays with you for the rest of your life. While you get more checks over your lifetime by starting early, each check is significantly smaller.

The Bonus of Delayed Retirement Credits (Age 70)

For those who can afford to wait, the reward is substantial. For every year you delay filing past your FRA, your benefit increases by 8% annually. This continues until you reach age 70. If your FRA is 67 and you wait until 70, you will receive 124% of your PIA. In the world of investing, a guaranteed 8% annual return is nearly impossible to find elsewhere, making “claiming at 70” a popular strategy for those looking to maximize their guaranteed monthly floor.

Factors That Can Alter Your Monthly Benefit Check

The amount you are “awarded” is not necessarily the amount you “keep.” Several factors can fluctuate your monthly take-home pay, ranging from federal policy to your own continued employment.

Cost-of-Living Adjustments (COLA)

One of the most valuable features of Social Security is the Cost-of-Living Adjustment. Every October, the SSA announces the COLA for the following year based on the Consumer Price Index (CPI-W). This ensures that your purchasing power does not erode as the price of goods and services rises. For example, in 2023, retirees saw a historic 8.7% increase due to high inflation. These adjustments are automatic and compounded, meaning your monthly check should theoretically keep pace with the economy over decades.

Taxation of Social Security Benefits

A common surprise for new retirees is that Social Security benefits can be taxable. Depending on your “combined income” (which includes your adjusted gross income, non-taxable interest, and half of your Social Security benefits), you may owe federal income tax on up to 50% or 85% of your benefits. If you have significant distributions from a traditional 401(k) or IRA, it is likely that a portion of your Social Security check will be redirected to the IRS.

The Earnings Test for Those Still Working

If you claim Social Security before reaching your FRA and continue to work, you may be subject to the Retirement Earnings Test. In 2024, if you earn more than $22,320, the SSA will withhold $1 in benefits for every $2 you earn above that limit. Once you reach your FRA, this limit disappears, and your benefit is recalculated upward to account for the months benefits were withheld. However, in the short term, this can significantly reduce your monthly cash flow.

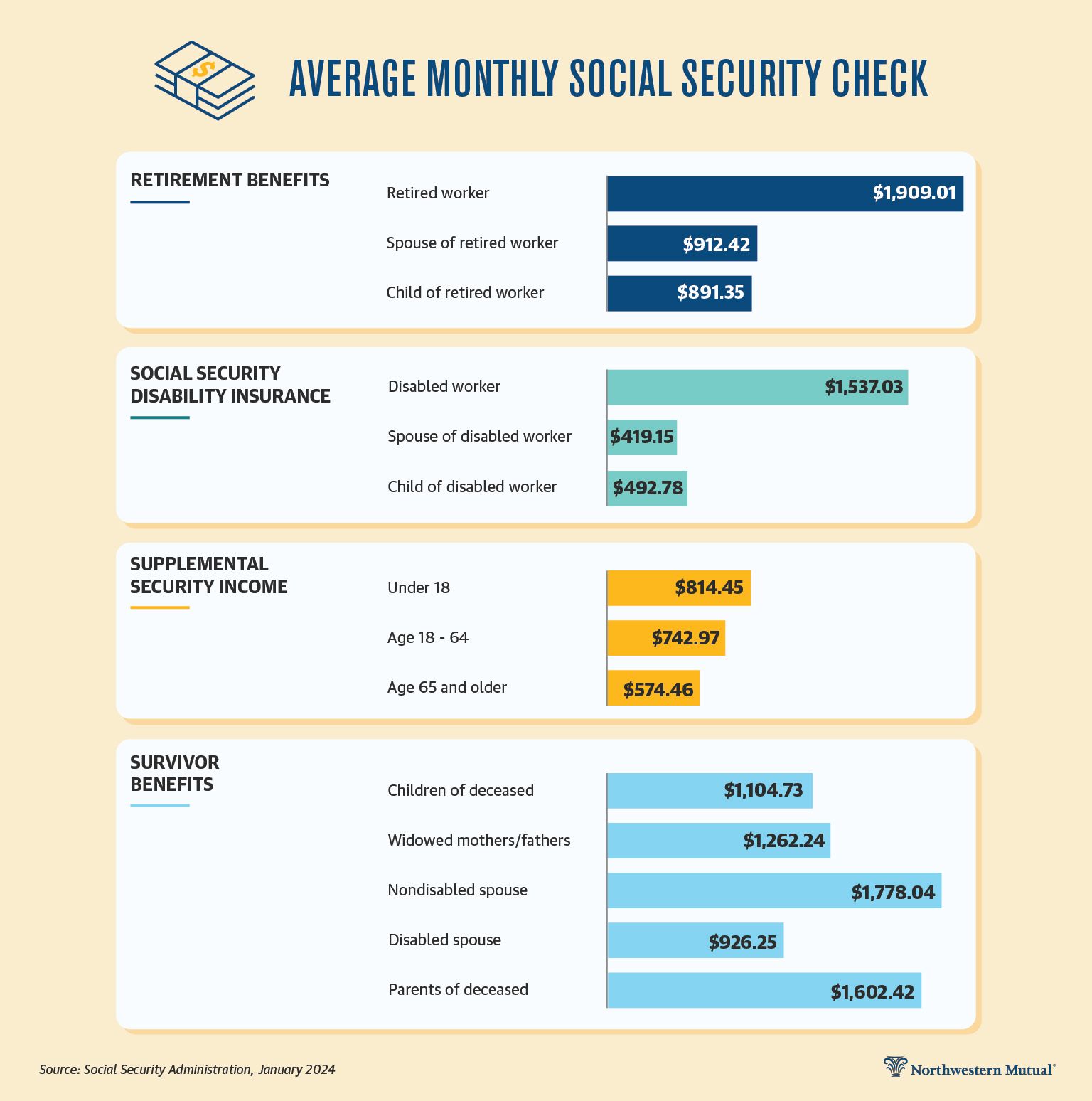

Specialized Benefits: Spousal, Survivor, and Disability Payments

Social Security is more than just a retirement program for the individual worker; it is a family insurance plan. Many people receive monthly amounts based on someone else’s work record.

Maximizing Spousal Benefits

A spouse who has not worked, or who earned significantly less, can claim a spousal benefit. This is equal to up to 50% of the higher-earning spouse’s PIA. This can be a vital source of income for households where one partner stayed home to raise children. Crucially, claiming a spousal benefit does not reduce the primary worker’s benefit.

Survivor Benefits for Families

In the event of a worker’s death, the surviving spouse may be eligible for survivor benefits. Typically, the survivor can receive 100% of the deceased spouse’s benefit if they have reached their own FRA. This is a critical component of life insurance and estate planning, ensuring that the household income does not plummet upon the death of the primary breadwinner.

SSDI: Social Security for Disability

Social Security Disability Insurance (SSDI) provides monthly payments to individuals who can no longer work due to a severe, long-term disability. The monthly amount for SSDI is calculated similarly to retirement benefits, but it allows individuals to access their “full” benefit amount earlier than their FRA because of their medical condition.

Strategic Planning for a Secure Financial Future

Knowing “how much” you will get is the first step toward determining “how much more” you need. Social Security was never intended to be a person’s sole source of retirement income; it was designed to replace about 40% of the average worker’s pre-retirement earnings.

Using the Social Security Administration (SSA) Estimator

The most accurate way to find your specific number is to create a “my Social Security” account on the official SSA website. This portal provides personalized estimates based on your actual earnings record. It allows you to toggle between different retirement ages to see exactly how your monthly check changes. Checking this annually is a fundamental task for any serious financial planner.

Integrating Social Security with 401(k)s and IRAs

Modern retirement planning involves “stacking” income sources. By knowing your projected Social Security amount, you can determine your “income gap”—the difference between your Social Security check and your required monthly expenses. This gap is what your 401(k), Roth IRA, or brokerage accounts must fill. If your Social Security is $2,500 and your expenses are $5,000, your portfolio must safely generate $2,500 per month.

Bridging the Gap: Side Hustles and Passive Income

For those whose Social Security estimates are lower than desired, the “Money” niche offers various solutions. Engaging in a side hustle or building passive income streams (like rental properties or dividend stocks) during your 50s and 60s can allow you to delay claiming Social Security until age 70. This “bridge” strategy maximizes your permanent monthly benefit while ensuring you don’t have to drain your retirement savings too early.

In conclusion, how much Social Security you receive per month is a figure largely within your control. Through strategic work history management, careful timing of your filing date, and a deep understanding of tax implications, you can optimize this vital pillar of your financial life. Social Security is not just a government check; it is a dynamic financial tool that, when used correctly, provides the security necessary to enjoy a long and prosperous retirement.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.